San Francisco’s funding landscape offers two distinct paths for business growth, yet many founders confuse private equity vs venture capital. These investment approaches differ fundamentally in how they operate, the companies they target, and the returns they pursue.

At Primum Law Group, we help business owners navigate these options with clarity. Understanding which path aligns with your company’s stage and goals is essential for making the right decision.

How Private Equity and Venture Capital Shape San Francisco’s Growth

Private Equity Targets Established Companies

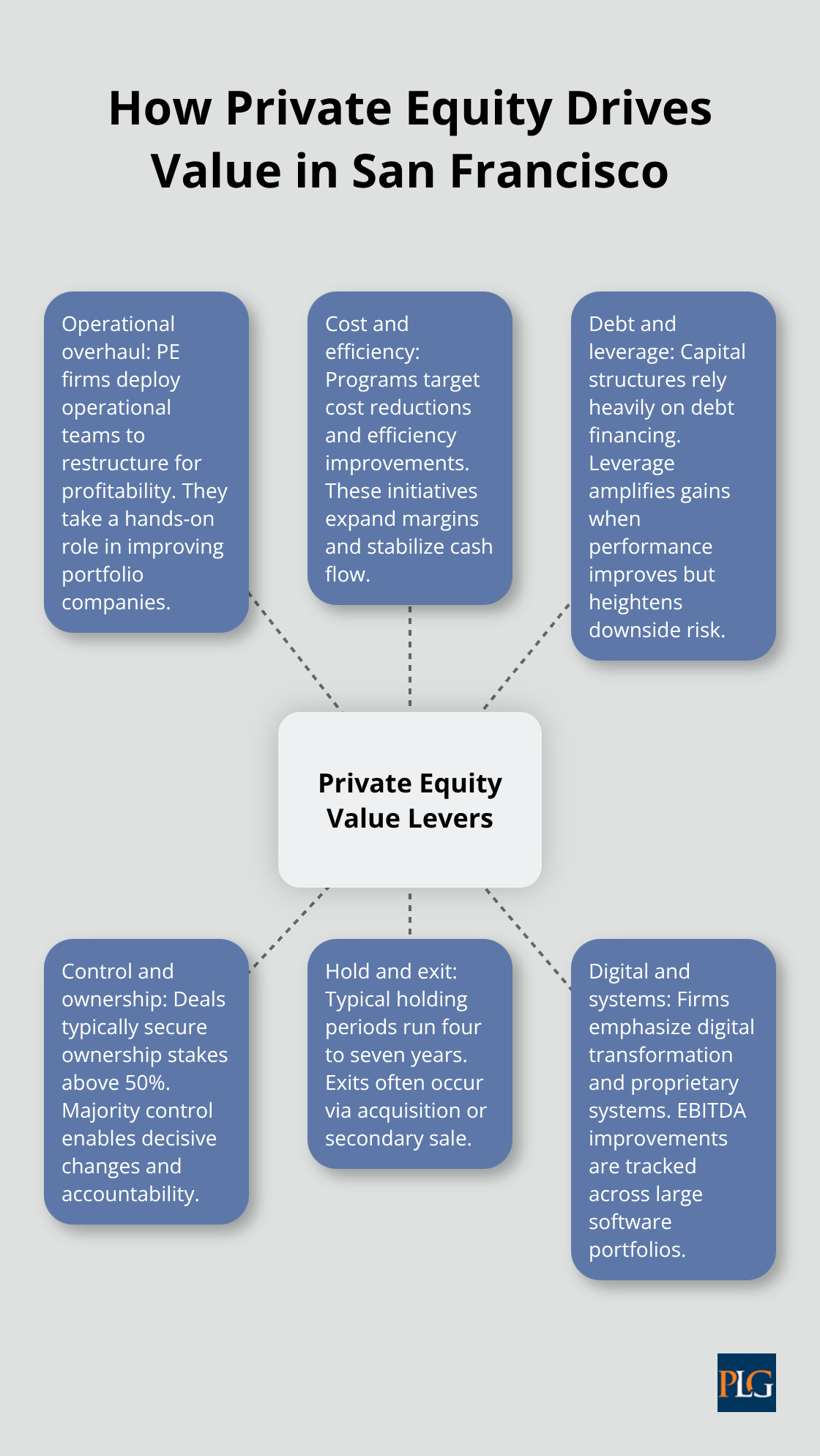

San Francisco’s private equity market focuses on mature businesses with proven cash flows. Firms like TPG manage around $251 billion in assets as of March 2025 and acquire established companies to restructure them for profitability. These PE firms deploy operational teams to overhaul portfolio companies, focusing on cost reductions, efficiency improvements, and debt restructuring. Hellman & Friedman (managing approximately $115 billion) and Silver Lake (roughly $103 billion) concentrate on digital transformation and operational leverage rather than rapid growth.

Vista Equity Partners, another San Francisco heavyweight with over $100 billion in assets, has completed more than 600 transactions since inception by focusing on enterprise software and data. Their portfolio includes 90+ companies that generate measurable EBITDA improvements. PE investments typically exceed $100 million per deal, with ownership stakes above 50%, and holding periods of four to seven years before exit via acquisition or secondary sale. The capital structure relies heavily on debt financing, which magnifies returns when operations improve but increases risk during downturns.

Venture Capital Backs High-Growth Startups

Venture capital in San Francisco operates on the opposite end-early-stage startups with high growth potential attract VC funding through minority stakes of 15% to 35% per round. VC investment in the U.S. rose more than 63 percent year over year, reaching the highest level since 2021, according to PitchBook data cited by the Wall Street Journal Pro. The Bay Area captured the majority of these dollars, driven largely by the AI boom as private AI startups secured jumbo rounds that compressed traditional funding timelines.

VC deal sizes commonly range from $25 million to $100 million per round, though many early-stage Series A investments fall below $10 million. Unlike PE’s structured buyout approach, VC involves staged capital injections tied to milestones. Founders retain operational autonomy while VCs provide strategic guidance, board representation, and network access.

Risk Models Diverge Significantly

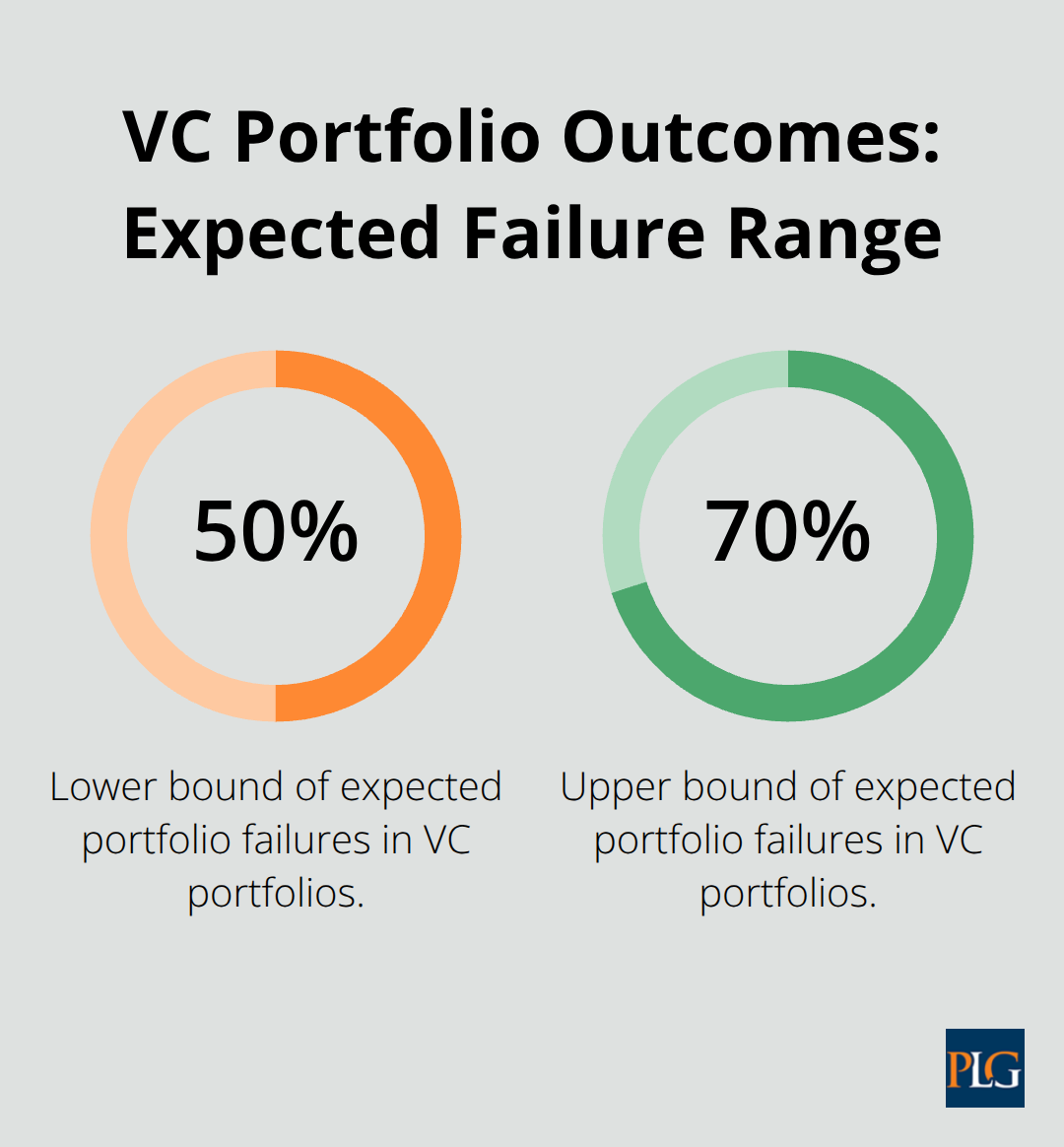

The risk model differs fundamentally between these two approaches. VC expects portfolio failure rates of 50 to 70 percent, betting that a handful of winners will generate outsized returns. PE targets fewer, larger bets with lower risk of total loss, relying on operational improvements to drive value across a concentrated portfolio.

San Francisco’s concentration of VC capital creates both opportunity and challenge. Founders outside the region face tougher competition for dollars, while those in the Bay Area benefit from proximity to talent networks and proven exit pathways through IPOs and acquisitions. This geographic concentration shapes which funding path makes sense for your company’s location and growth stage.

Where the Money Goes and How Long It Stays

Deal Size Reveals Different Risk Appetites

PE firms write checks exceeding $100 million per deal and acquire established companies that generate steady cash flow. VC funds deploy $25 million to $100 million per round into startups still finding product-market fit, with many Series A rounds falling below $10 million. This size gap reflects fundamentally different risk calculations. A PE firm betting $200 million on a software company with $50 million in annual revenue expects operational improvements to drive returns. A VC fund investing $5 million in an AI startup with zero revenue bets on exponential growth.

San Francisco’s leading PE firms illustrate this scale. TPG manages $251 billion in assets and targets companies ready for transformation. Vista Equity Partners has deployed capital across 600+ transactions in enterprise software, where established products generate predictable revenue. Sixth Street Partners operates with $110 billion in assets and structures flexible deals for large commitments.

Holding Periods and Exit Timelines Differ Dramatically

PE firms hold companies for four to seven years, then exit via acquisition or secondary sale. This extended timeline allows for systematic operational overhaul and debt paydown before investors realize returns.

VC operates on a different clock. The AI boom pushed VC investment up 63 percent year over year according to PitchBook data, with jumbo rounds compressing traditional timelines. Founders now race to hit growth milestones within 18 to 24 months before the next funding round. This creates vastly different pressure. A PE-backed manufacturing company might have years to optimize supply chains. A VC-backed fintech startup must demonstrate user acquisition rates and unit economics within quarters.

Operational Teams Transform Portfolio Companies

PE firms deploy dedicated operational teams into portfolio companies. KKR maintains teams focused solely on operational transformation. These professionals cut costs, consolidate vendors, and restructure management before exit. Vista Equity Partners built proprietary systems to drive EBITDA improvements across its 90+ portfolio companies.

VC involvement looks different. VCs take board seats and provide strategic guidance, but founders retain day-to-day control. A VC board member might advise on go-to-market strategy or introduce customers, but they rarely hire and fire executives or restructure operations. This distinction matters enormously for founders. Accepting PE capital means accepting operational oversight and pressure to hit specific financial targets. Accepting VC capital preserves autonomy but demands founder execution on growth metrics.

San Francisco’s Market Shows Two Distinct Paths

Francisco Partners has completed 450+ transactions in technology by providing strategic input without operational takeover. Alpine Investors uses a people-first approach with software and services companies, maintaining lighter operational involvement than traditional PE. These differences shape which founders thrive under each model. Founders who excel at financial engineering and operational discipline fit PE. Founders who move fast and prioritize product development fit VC.

The choice between these paths hinges on how much control you want to retain and how quickly you need to scale. Understanding your company’s operational strengths and growth timeline helps clarify which approach aligns with your vision.

Which Funding Path Matches Your Company’s Stage

Established Businesses Fit Private Equity

Established businesses in San Francisco with predictable revenue streams and operational maturity should consider private equity. Your company likely qualifies for PE if you generate $10 million to $50 million in annual revenue, operate with positive EBITDA, and have a clear path to scale through operational improvements rather than product innovation. PE firms like Vista Equity Partners target software companies with 90+ portfolio holdings that produce measurable EBITDA improvements, meaning they acquire businesses already functioning at scale. If your team excels at financial discipline, cost management, and execution against defined targets, PE capital accelerates growth through leverage and systematic operational oversight.

A manufacturing company with $30 million in revenue and room to consolidate suppliers or optimize supply chains fits this profile perfectly. PE holds companies for four to seven years, so you need patience for the restructuring process and willingness to accept operational teams that will implement changes across your organization. The capital injection typically exceeds $100 million per deal according to PitchBook data, giving you resources to acquire competitors or expand geographically while debt financing magnifies returns as operations improve.

Early-Stage Startups Thrive With Venture Capital

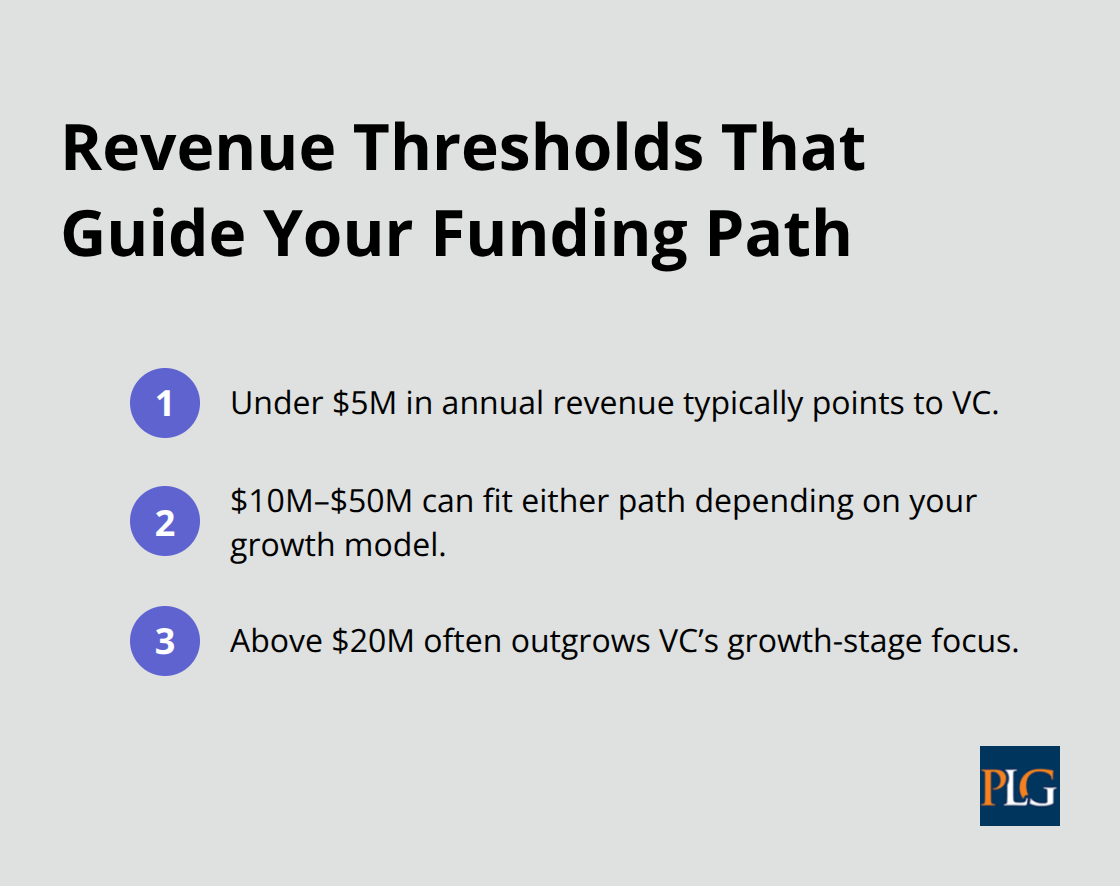

Early-stage startups in the Bay Area pursuing rapid growth in technology, AI, or software should pursue venture capital. VC investment in the U.S. rose more than 63 percent year over year according to PitchBook data cited by the Wall Street Journal Pro, with AI startups securing jumbo rounds that compressed traditional funding timelines. If your company has less than three years of operating history, generates under $5 million in annual revenue, and operates in a high-growth market, VC aligns with your trajectory.

Series A rounds typically range from $25 million to $100 million, though many early-stage investments fall below $10 million. VC investors expect failure across their portfolio but bet that a few winners produce outsized returns, so they tolerate the uncertainty inherent in scaling new products. You retain operational control while VCs provide board representation, strategic guidance, and network access to customers and talent. The compressed timelines mean you must demonstrate user acquisition, unit economics, or revenue growth within 18 to 24 months before the next funding round. When negotiating with VC investors, understanding venture capital term sheets helps you secure favorable terms and recognize key clauses that protect your interests. Francisco Partners has completed 450+ technology transactions by providing strategic input without operational takeover, illustrating how VC involvement preserves founder autonomy while accelerating growth through market access and advisory support.

Revenue Thresholds Separate These Paths

The revenue threshold separates these funding approaches clearly. Companies under $5 million in annual revenue lack the operational stability PE requires, while those above $20 million in revenue often outgrow VC’s growth-stage focus. Companies at $10 million to $50 million in revenue occupy the middle ground where both paths become viable, but your growth model determines which fits better.

A SaaS company with $15 million in recurring revenue and 30 percent annual growth should consider VC to fund aggressive customer acquisition and product development. The same revenue level at a staffing services firm with stable margins but limited growth potential signals PE opportunity, where operational improvements and margin expansion drive returns. San Francisco’s geographic concentration of VC capital creates advantages for startups in the Bay Area, while established companies anywhere in the region can access PE capital. Your location matters less than your company’s operational maturity and growth trajectory.

Management Teams Must Match Capital Partners

PE demands management teams comfortable with external operational oversight and financial engineering. You need CFO-level financial management, clear cost accounting, and willingness to implement systems that PE firms install across portfolio companies. KKR maintains dedicated operational teams that will hire and fire executives, restructure departments, and demand specific performance metrics. If your current management team resists external input or lacks deep financial discipline, PE capital creates friction.

VC demands founder execution on growth metrics but preserves your ability to lead product development and company culture. You need a team that moves fast, experiments constantly, and scales go-to-market functions without operational hand-holding from investors. Alpine Investors uses a people-first approach with software companies, maintaining lighter operational involvement than traditional PE, but you still need strong operational discipline to hit growth milestones quarterly. The wrong capital partner creates misalignment that derails company performance, so assess your management team’s strengths honestly before choosing.

Final Thoughts

Private equity vs venture capital represents a fundamental choice about how your company grows and who controls that growth. PE firms acquire established companies and deploy operational teams to drive profitability through systematic improvements and financial engineering. VC funds back early-stage startups with high growth potential, providing capital and strategic guidance while founders retain operational control.

San Francisco’s market demonstrates both paths thrive simultaneously. TPG, Vista Equity Partners, and Hellman & Friedman manage hundreds of billions in assets by acquiring mature software and services companies. Meanwhile, VC investment in the U.S. rose more than 63 percent year over year according to PitchBook data, with the Bay Area capturing the majority of these dollars through AI startups securing jumbo rounds.

Your next step depends on your company’s stage and operational maturity. Companies generating $10 million to $50 million in annual revenue with positive EBITDA and clear operational improvement opportunities should explore PE conversations. Companies under $5 million in revenue pursuing rapid growth in technology or software should pursue VC funding, and we at Primum Law Group help founders navigate both paths by handling venture capital and private equity transactions throughout San Francisco and Silicon Valley.