San Francisco’s investment landscape presents two distinct paths: venture capital and private equity. Each approach serves different company stages and investor goals.

We at Primum Law Group see how these funding models create unique legal challenges. Understanding their differences helps investors navigate complex deal structures and regulatory requirements effectively.

Venture Capital Fundamentals in San Francisco

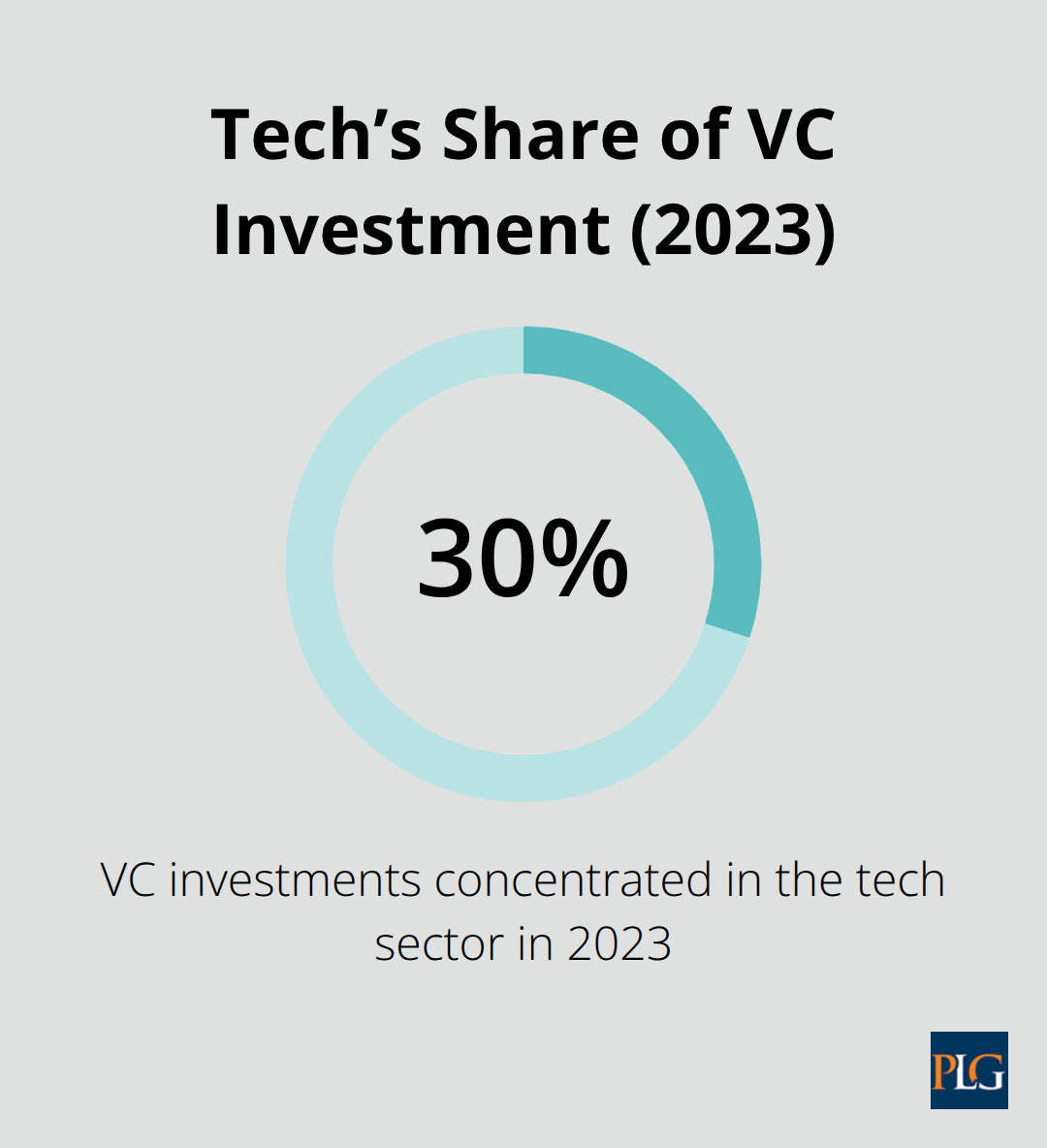

San Francisco venture capital firms target companies at seed through Series B stages, with investments between $1 million and $15 million per round according to PitchBook data. These firms focus heavily on technology startups, biotech companies, and clean energy ventures that demonstrate scalable business models. The National Venture Capital Association reports that 30% of all VC investments in 2023 concentrated in the tech sector, with San Francisco firms at the forefront of this trend.

Early Stage Investment Strategy

Venture capitalists in San Francisco accept extremely high failure rates and expect 70% of their portfolio companies to fail or break even. They target 10x to 100x returns on successful investments to compensate for these losses. Sequoia Capital and Andreessen Horowitz exemplify this approach-they spread investments across 20-30 startups per fund to maximize the probability of breakout companies.

Minority Stakes and Board Control

San Francisco VC deals typically involve minority equity stakes of 15% to 35% per round. Venture capitalists rarely seek majority control and instead negotiate for one to two board seats plus protective provisions that give them veto power over major decisions. Standard terms include anti-dilution provisions, liquidation preferences, and drag-along provisions that protect investor interests while founders maintain operational control.

Exit Timeline and Return Expectations

The average VC investment period spans 3 to 5 years, with exits primarily through acquisitions or initial public offerings when companies reach sufficient scale. This timeline contrasts sharply with private equity approaches, which operate under different investment horizons and target different company profiles entirely.

Private Equity Fundamentals in San Francisco

Private equity firms in San Francisco target mature companies with annual revenues between $50 million and $500 million, according to Bain research. These firms acquire majority stakes or complete ownership through leveraged buyouts and use significant debt to maximize returns. Blackstone Group and Apollo Global Management represent this approach, as they focus on established businesses in healthcare, financial services, and manufacturing sectors that generate stable cash flows. McKinsey data shows private equity firms achieve average internal rates of return around 14% through operational improvements rather than bets on future growth potential.

Target Company Profile and Investment Approach

San Francisco private equity firms select companies with proven business models and predictable revenue streams. They avoid early-stage ventures and instead pursue businesses that need operational restructuring or market consolidation. These firms conduct extensive financial analysis before acquisition, examining EBITDA margins, debt capacity, and competitive positioning. The investment thesis centers on value creation through efficiency gains rather than market expansion or product innovation (unlike venture capital strategies).

Operational Involvement and Value Creation Strategies

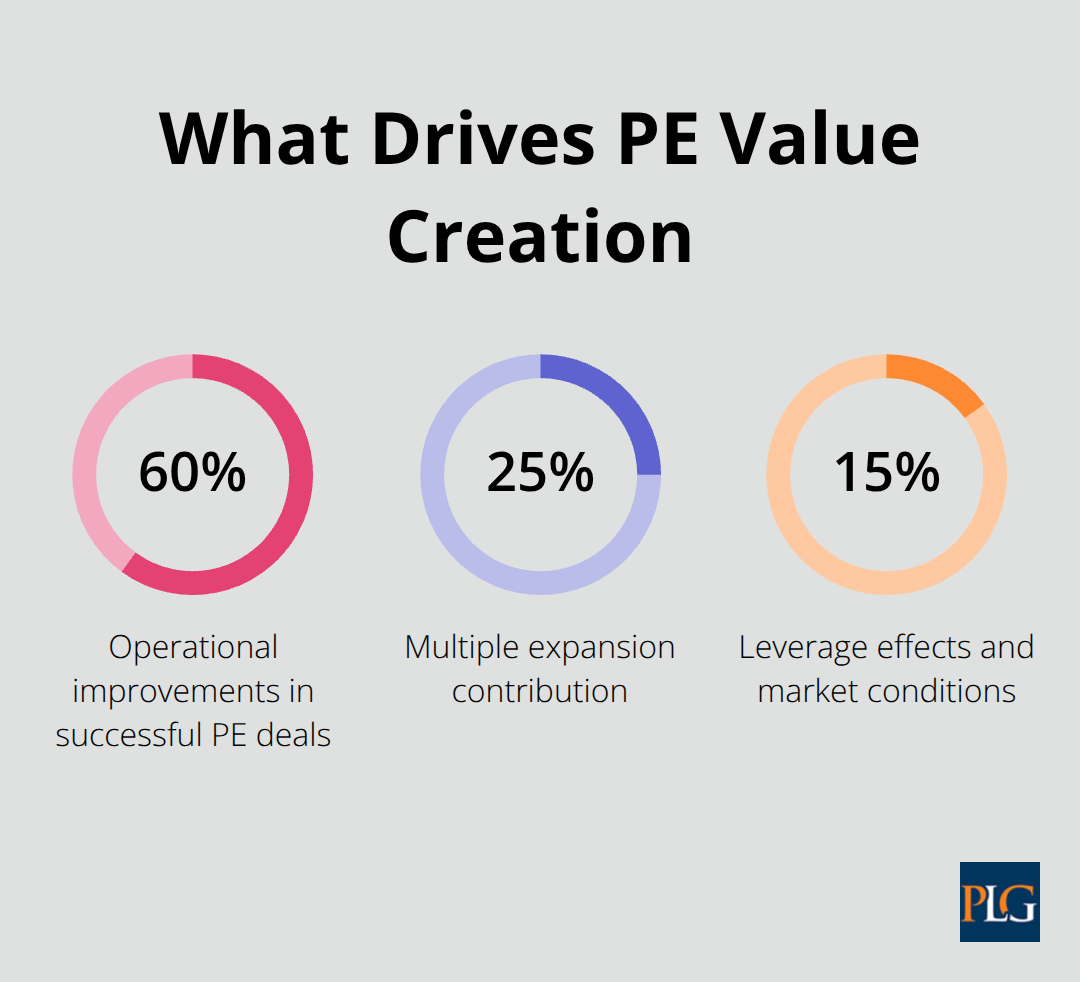

Private equity firms deploy dedicated operational teams to drive efficiency improvements within 12 months of acquisition. They replace underperforming management, streamline supply chains, and consolidate redundant operations to increase profit margins. This intensive involvement contrasts sharply with venture capital’s mentorship approach. PitchBook reports that operational improvements account for 60% of value creation in successful private equity deals, while multiple expansion contributes only 25%. The remaining 15% comes from leverage effects and market conditions.

Exit Timeline and Return Expectations

Private equity firms plan exit strategies from day one and target sales to strategic buyers or secondary buyouts rather than IPOs. They maintain $1.5 trillion in dry powder as of 2023, which enables quick acquisitions when attractive opportunities arise. The average holding period spans 5 to 7 years because operational transformations require sustained implementation. These firms generate returns through debt paydown, operational improvements, and strategic positioning rather than exponential growth expectations. San Francisco private equity firms increasingly pursue add-on acquisitions, where they purchase smaller companies to merge with existing portfolio holdings and create market-leading entities with enhanced valuations.

These fundamental differences in investment philosophy and execution create distinct legal requirements that shape deal documentation and regulatory compliance strategies. Business lawyers specializing in private equity transactions must navigate complex commercial contracts that govern these sophisticated investment structures.

Key Legal Differences Between VC and PE Deals

Due Diligence Requirements and Documentation

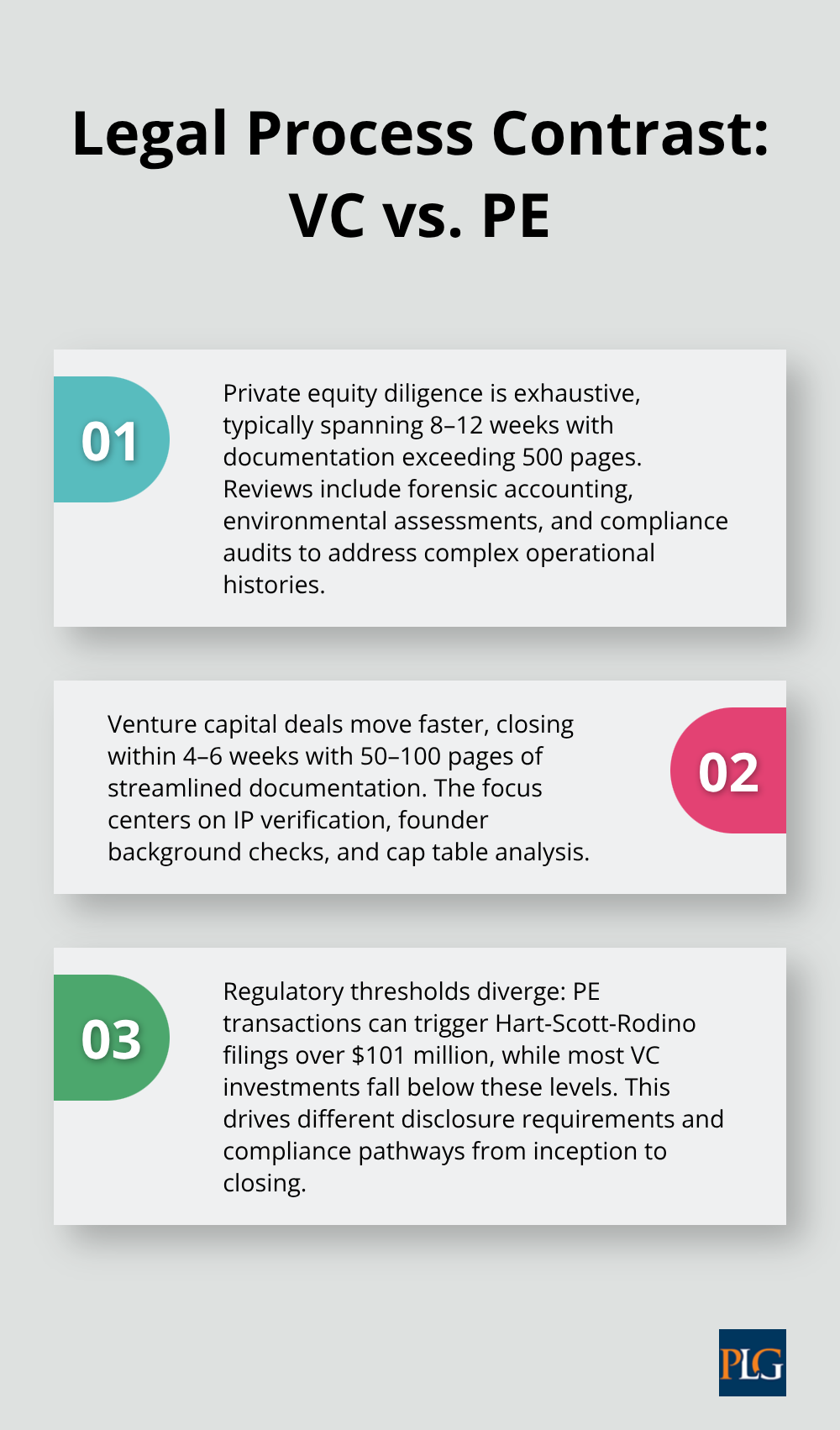

Private equity transactions demand exhaustive due diligence that spans 8-12 weeks and produces documentation that exceeds 500 pages per deal. PE firms conduct forensic accounting reviews, environmental assessments, and regulatory compliance audits because they acquire mature companies with complex operational histories. Venture capital deals move faster with streamlined documentation that averages 50-100 pages and closes within 4-6 weeks. VC firms focus on intellectual property verification, founder background checks, and cap table analysis rather than operational audits.

The Securities and Exchange Commission requires different disclosure levels for these transaction types. PE deals trigger Hart-Scott-Rodino filing requirements for acquisitions that exceed $101 million, while most VC investments fall below regulatory thresholds. This creates distinct compliance pathways that shape legal strategy from deal inception through closing.

Regulatory Compliance and Securities Law Considerations

Private equity firms face stricter regulatory oversight due to their acquisition size and control positions. The Dodd-Frank Act imposes enhanced reporting requirements on PE firms that manage over $150 million in assets, including quarterly filings and annual examinations. VC firms operate under different regulatory frameworks because they take minority positions and invest smaller amounts per transaction.

Securities law compliance varies significantly between these investment types. PE transactions often involve complex debt structures that require extensive securities filings, while VC deals primarily use equity instruments with simpler disclosure requirements. The Investment Company Act of 1940 creates additional compliance burdens for PE firms but provides exemptions for most VC activities (due to their focus on early-stage companies).

Board Composition and Governance Structures

Private equity firms negotiate majority board control and implement extensive reporting requirements that include monthly financial statements and quarterly business reviews. They install independent directors and create specialized committees for audit, compensation, and strategic planning. This governance structure reflects their operational involvement and majority ownership positions.

Venture capital deals feature minority investor protection through liquidation preferences, anti-dilution provisions, and consent rights that don’t require board control. VC firms typically secure one board seat per funding round and rely on protective provisions rather than voting control. The Sarbanes-Oxley Act compliance becomes mandatory for PE-backed companies that plan public exits, while VC-backed startups face lighter regulatory burdens until they reach public company status or significant revenue thresholds.

Final Thoughts

Venture capital and private equity represent fundamentally different investment approaches that create distinct legal requirements in San Francisco’s competitive market. VC deals prioritize speed and flexibility with streamlined documentation, while PE transactions demand comprehensive due diligence and complex governance structures. These differences directly impact legal strategy, from securities compliance to board composition.

The regulatory landscape varies significantly between these investment types. PE firms face enhanced reporting under Dodd-Frank and Hart-Scott-Rodino requirements, while VC investments operate under lighter regulatory frameworks (due to their minority stake approach). Documentation complexity reflects this divide, with PE deals producing 500+ pages compared to VC’s 50-100 page average.

Success in either sector requires legal counsel that understands these nuanced differences between venture capital and private equity transactions. We at Primum Law Group provide comprehensive legal support for both investment types, helping clients navigate complex deal structures and regulatory requirements. Our team supports your investment strategy through each phase of the transaction process.