A venture capital term sheet can feel overwhelming at first glance. It’s packed with legal language, financial terms, and conditions that will shape your company’s future.

At Primum Law Group, we’ve helped founders navigate these documents countless times. This guide breaks down what actually matters so you can negotiate with confidence.

What Actually Moves the Needle in Your Term Sheet

The three numbers that will shape your decisions for years are valuation, investment amount, and liquidation preferences. Founders often fixate on valuation because it feels like public validation of their company’s worth. The reality is different: your actual return at exit depends far more on liquidation preferences than on the headline valuation number.

How Liquidation Preferences Determine Your Real Payout

A $10 million pre-money valuation sounds impressive until you realize a 1x non-participating liquidation preference means investors get their money back first, then you split what remains with other shareholders. If your company sells for $15 million and investors put in $5 million, they take $5 million and you split the remaining $10 million with your co-founders and employees. Swap that for a 2x participating preference and investors walk away with $10 million, leaving only $5 million for everyone else. This is why modeling multiple exit scenarios matters more than negotiating another $1 million on valuation.

The Price Per Share Calculation That Determines Your Dilution

Your share price gets calculated from pre-money valuation divided by your fully diluted capitalization table. Most founders get this wrong because they forget to include the option pool in the fully diluted count. If you raise $5 million at a $20 million pre-money valuation, your post-money is $25 million. But if you reserved a 10% option pool for future hires, that pool dilutes everyone, including the new investor. Your effective ownership drops faster than the headline math suggests.

The fully diluted cap table must include all shares, options, and warrants outstanding to give an accurate picture of who owns what. Founders should calculate their own ownership percentage by dividing invested capital by post-money valuation to see the real impact before signing.

Investment Amount and Milestone Conditions Shape Your Funding Timeline

The investment amount sounds straightforward until you encounter milestone conditions. Some investors tie fund disbursement to hitting specific revenue targets or product milestones. Set these targets realistically or you’ll miss funding tranches when you need them most.

Liquidation preferences determine the waterfall of payouts at exit, and this is where most founders get blindsided. A 1x non-participating preference protects investors’ downside but lets you keep upside above their payout. A 1x participating preference means investors get their money back and then participate in remaining proceeds alongside common shareholders, essentially double-dipping. A 2x or 3x preference multiplies the investor’s initial investment before any founder payout occurs.

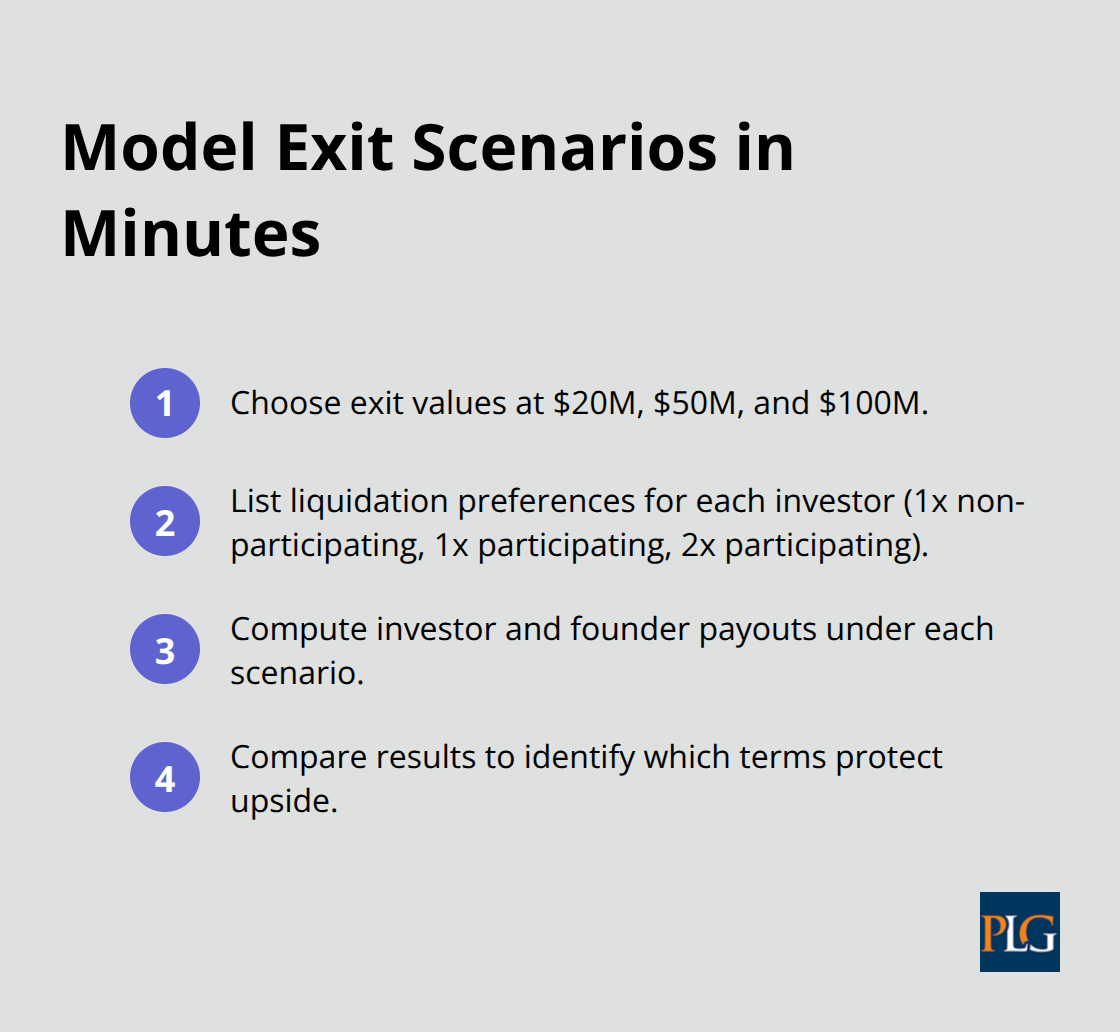

Model Exit Scenarios to Reveal Which Terms Protect Your Upside

The preference also compounds if multiple rounds came before yours, stacking obligations that shrink founder returns in modest exits. Model three scenarios: a $20 million exit, a $50 million exit, and a $100 million exit. Calculate investor and founder payouts under each liquidation preference option you’re considering (1x non-participating, 1x participating, 2x participating). The math will reveal which terms actually protect your upside versus which ones sound fair but aren’t.

These calculations form the foundation for your negotiation strategy. Once you understand how different preferences affect your returns across multiple exit values, you’ll know exactly which terms matter and which ones you can concede.

What Investor Protections Really Mean for Your Control

Investor protections in a term sheet aren’t theoretical safeguards-they shift decision-making power away from founders. The three protections investors push hardest for are voting rights tied to board seats, anti-dilution clauses that adjust share prices downward, and information rights that let them monitor your business continuously. Understanding how each one actually works in practice will show you where to push back and where conceding makes sense.

Board Seats and Protective Provisions

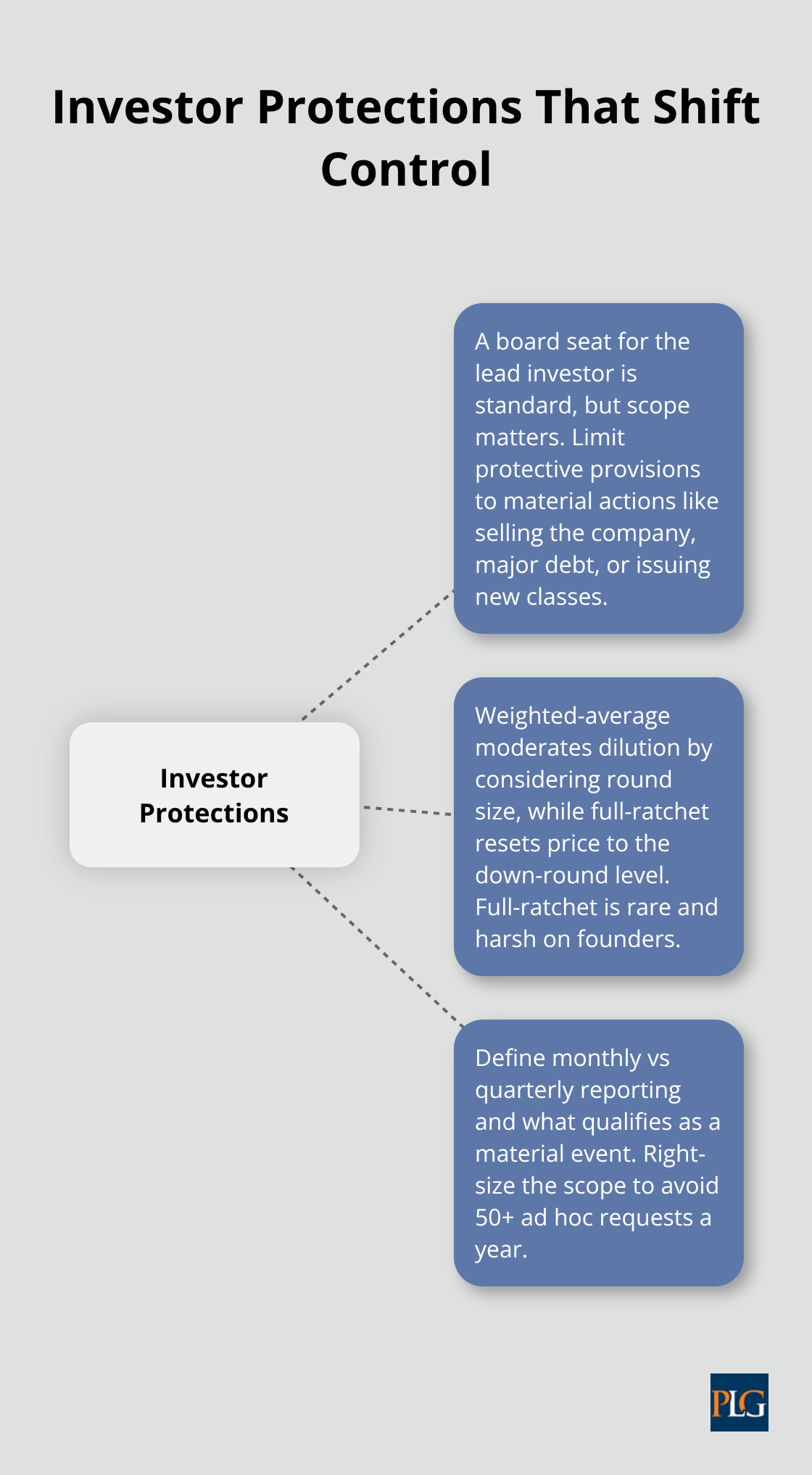

A board seat for your lead investor is standard in Series A rounds, but the real question is whether that seat gives them veto power over daily operations or just visibility into major decisions. Most investors demand protective provisions allowing them to block certain actions without full board approval: selling the company, taking on large debt, issuing new share classes, or approving related-party transactions.

The problem is scope creep. Some investors try to expand these provisions to cover hiring decisions, marketing spend, or product direction. Push back hard here. Protective provisions should apply only to material decisions that affect the company’s fundamental structure or exit path, not operational matters you control as CEO. If an investor demands veto rights over hiring or spending decisions, that’s a red flag signaling they don’t trust your judgment-and that relationship will deteriorate fast once market conditions shift.

Anti-Dilution: Weighted-Average vs. Full-Ratchet

Anti-dilution provisions protect investors when you raise future rounds at lower valuations, but the mechanism matters enormously for your dilution. A weighted-average anti-dilution clause adjusts the investor’s effective price based on the down round’s size relative to their original investment, moderating their protection. A full-ratchet provision resets their price to whatever the new round commands, meaning if you raise Series B at half your Series A valuation, your Series A investor’s shares are repriced downward and your ownership gets crushed to compensate them.

Full-ratchet is brutal for founders and rare in legitimate VC deals, but you’ll see it occasionally in seed rounds or with less experienced investors. Weighted-average is market standard and acceptable, though you should negotiate whether it applies to all future issuances or excludes employee option pools and strategic partnerships.

Information Rights and Reporting Scope

Information rights require you to deliver monthly or quarterly financial statements, cap table updates, and board materials to all investors, plus notify them of material events within a set timeframe. This sounds reasonable until you’re running 50+ reporting requests annually across multiple investor groups.

Set clear reporting timelines upfront-monthly financials for the lead investor, quarterly for others-and define what constitutes a material event so you’re not sending emergency notifications about customer churn or staff departures. Information rights are non-negotiable, but you can shape their scope and frequency to match your operational reality rather than drowning in compliance work.

These protections form the foundation of investor governance, but they also reveal how much control you’ll retain as the company scales. The next section examines which terms you should fight to keep and which ones you can trade away without sacrificing your ability to run the business.

How to Negotiate Without Leaving Money on the Table

Most founders approach term sheet negotiation as a binary choice: accept or reject. The reality is messier and more profitable. You have leverage at specific points in the negotiation, and spending that leverage on the wrong terms costs you millions at exit.

Know Your Market Standards Before You Sit Down

The first step is understanding what market standards actually are for your stage and geography, not what sounds fair in isolation. Series A rounds in Silicon Valley typically feature 1x non-participating liquidation preferences, board seats for lead investors, and weighted-average anti-dilution clauses. These are baseline expectations, not ceiling limits. If an investor demands 2x participating preferences or full-ratchet anti-dilution without exceptional circumstances, they’re testing how much you know about market norms.

Benchmark your term sheet against recent rounds in your industry using Crunchbase or PitchBook data, which track thousands of actual deals. Knowing that Series A median valuations for SaaS companies hit $15-25 million pre-money in 2025 gives you concrete ground to stand on when an investor suggests half that valuation. Demonstrating traction and having a clear path to profitability can allow you to negotiate better terms and retain more equity.

Separate Deal-Killers from Negotiable Concessions

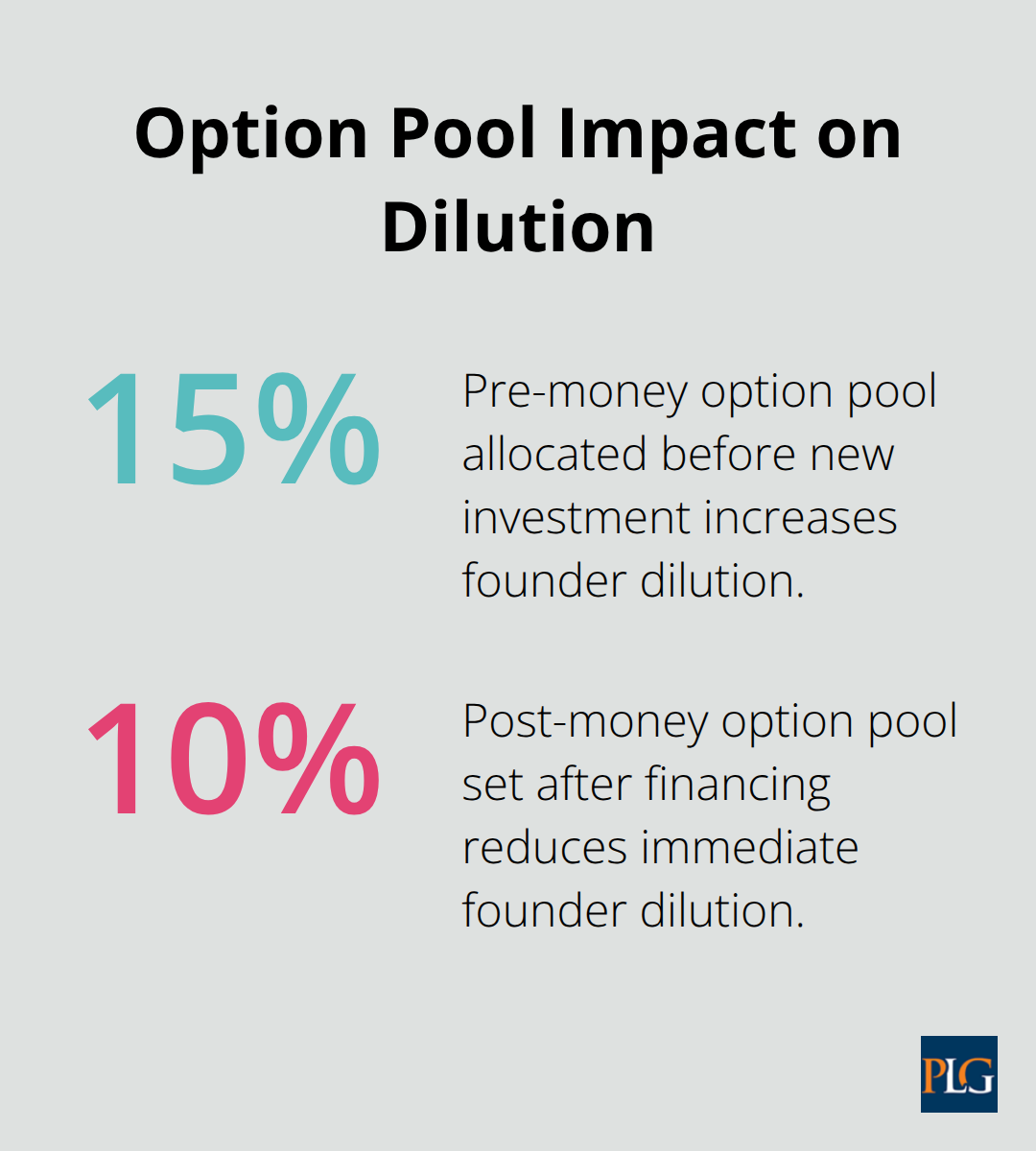

Valuation and liquidation preferences are deal-killers because they compound across exits and future rounds. The option pool size matters enormously: a 15% pre-money pool dilutes you more than a 10% post-money pool, yet founders often accept the first number without modeling the difference.

Board composition and protective provisions fall into the negotiable category if you keep scope narrow. Accept an investor board seat and protective provisions over major exits or debt, but fight fiercely against veto rights over hiring, product decisions, or operational spending. Most investors will accept this boundary once you explain that micromanagement kills execution velocity.

Define Information Rights That Match Your Operations

Information rights are non-negotiable but scoped: monthly financials and quarterly cap table updates are standard, but push back against requests for weekly reporting or real-time expense access. Set clear reporting timelines upfront so you’re not drowning in compliance work while running the business.

Hire a Lawyer Before You Start Negotiating

Hire a lawyer experienced in venture deals before you start negotiating, not after you have a term sheet. The cost of legal review upfront is 5-15K, far cheaper than negotiating away a 2% ownership stake because you missed an anti-dilution trap. A lawyer helps you identify which terms create downstream problems in Series B or C rounds, which most founders cannot see until too late. They also model your cap table under different scenarios so you understand the real dollar impact of each concession before you make it.

Final Thoughts

A venture capital term sheet is a roadmap, not a prison sentence. The terms you negotiate today ripple through every future funding round and ultimately determine how much of your company you own at exit. Valuation, liquidation preferences, and board composition matter most-everything else is negotiable if you understand what you’re trading away.

The most common mistake founders make is focusing on headline valuation while ignoring liquidation preferences. A $30 million pre-money valuation with a 2x participating preference leaves you with less money at exit than a $20 million pre-money with 1x non-participating. Model your exit scenarios before you sign anything and calculate what you actually take home under different preference structures at $20 million, $50 million, and $100 million exits. This math takes two hours and prevents years of regret.

Hire a lawyer before you have a term sheet, not after. The cost is minimal compared to the ownership stake you’ll preserve by catching anti-dilution traps and option pool mistakes that most founders miss. We at Primum Law Group help founders navigate venture deals from term sheet through closing so you can focus on building.