Corporate finance and securities law shape every major decision a growing company makes, from raising capital to closing acquisitions. Getting these fundamentals right protects your business and unlocks real growth opportunities.

At Primum Law Group, we’ve guided countless San Francisco companies through these complex decisions. This guide breaks down what you need to know to move forward with confidence.

Building the Right Capital Structure for Growth

Capital structure determines how your company funds operations and growth, and it shapes everything from investor returns to your control over the business. The choice between debt and equity financing isn’t theoretical-it directly affects cash flow, tax liability, and who makes decisions at your company. Many San Francisco founders treat this decision as a one-time event, but the most successful companies revisit their capital structure as they scale.

Debt Financing vs. Equity Financing

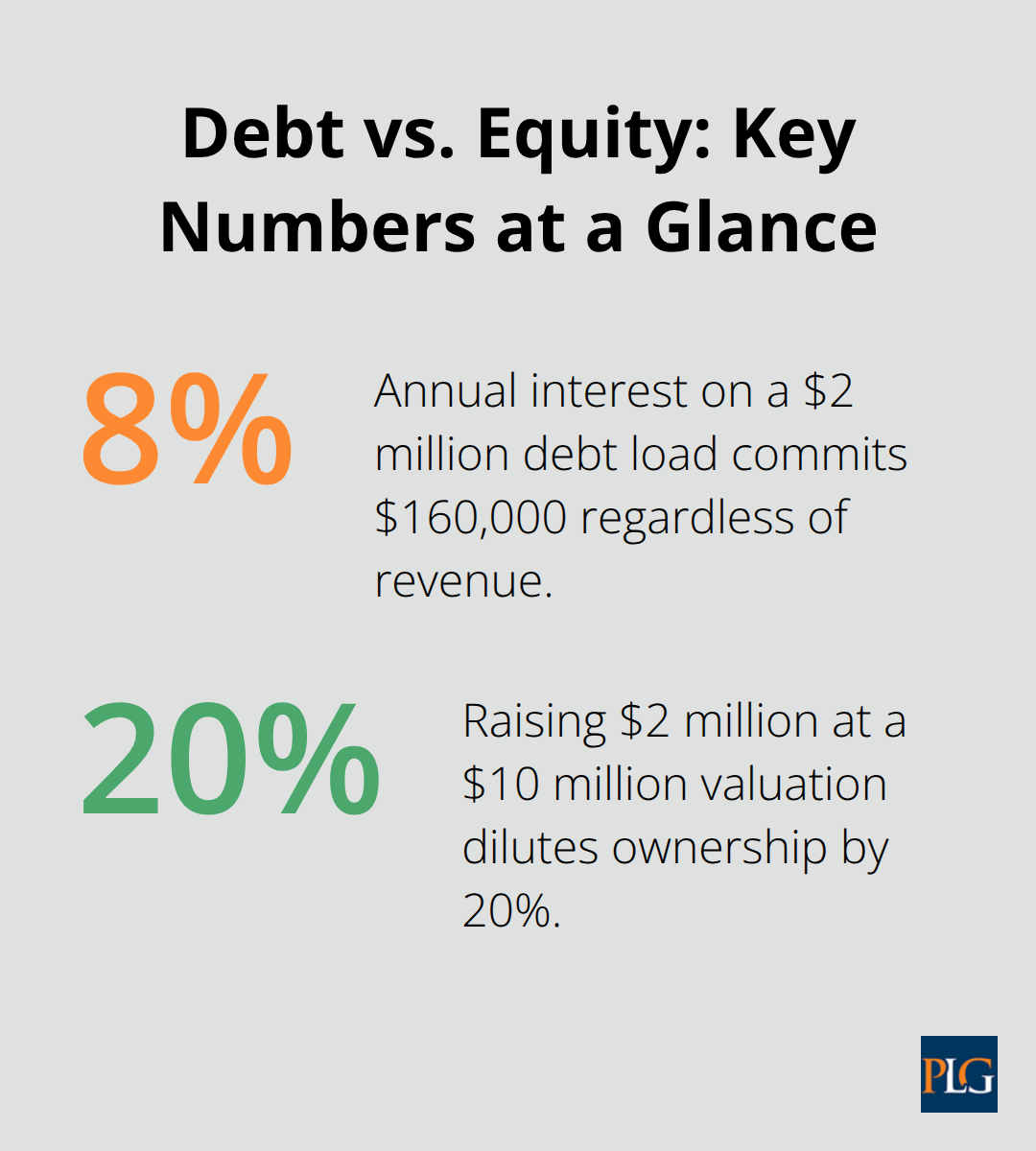

Debt financing through bank loans or bonds requires fixed repayment schedules and interest payments, which reduces cash available for operations but lets you retain full ownership and control. Equity financing means selling shares to investors, which brings capital without debt obligations but dilutes your ownership and introduces new stakeholders into major decisions. The math matters here: if you take on $2 million in debt at 8% interest, you commit $160,000 annually to repayment regardless of revenue. Equity financing avoids this fixed obligation, but if you raise $2 million at a $10 million valuation, you give up 20% of your company.

A 2024 survey from PitchBook found that venture-backed startups in California raised a median of $3.5 million in Series A funding, typically structured entirely as equity to minimize burn rate concerns early on. However, many growth-stage companies in San Francisco now layer in debt financing-convertible notes or venture debt-to extend their runway without further dilution.

When Debt Makes Sense for Your Business

Debt works best when your company generates predictable cash flow and has assets to pledge as collateral. Real estate companies, established software-as-a-service businesses with annual contracts, and manufacturing operations all use debt extensively because their revenue is stable enough to service debt obligations. Venture debt has become a practical tool for venture-backed startups in recent years; lenders like Horizon Technology Finance offer short-term debt products designed for early-stage companies with investor backing. The catch: venture debt typically costs 8–12% annually plus warrant coverage of 10–15%, meaning the lender gets options to buy shares at a discount. This structure protects lenders but increases your true cost of capital.

San Francisco biotech companies commonly use venture debt to extend runway between funding rounds because their development timelines are long and their equity rounds are infrequent. The key question isn’t whether debt is cheaper than equity in nominal terms-it’s whether your business can reliably generate cash to repay it.

Valuation Methods Shape Your Negotiating Power

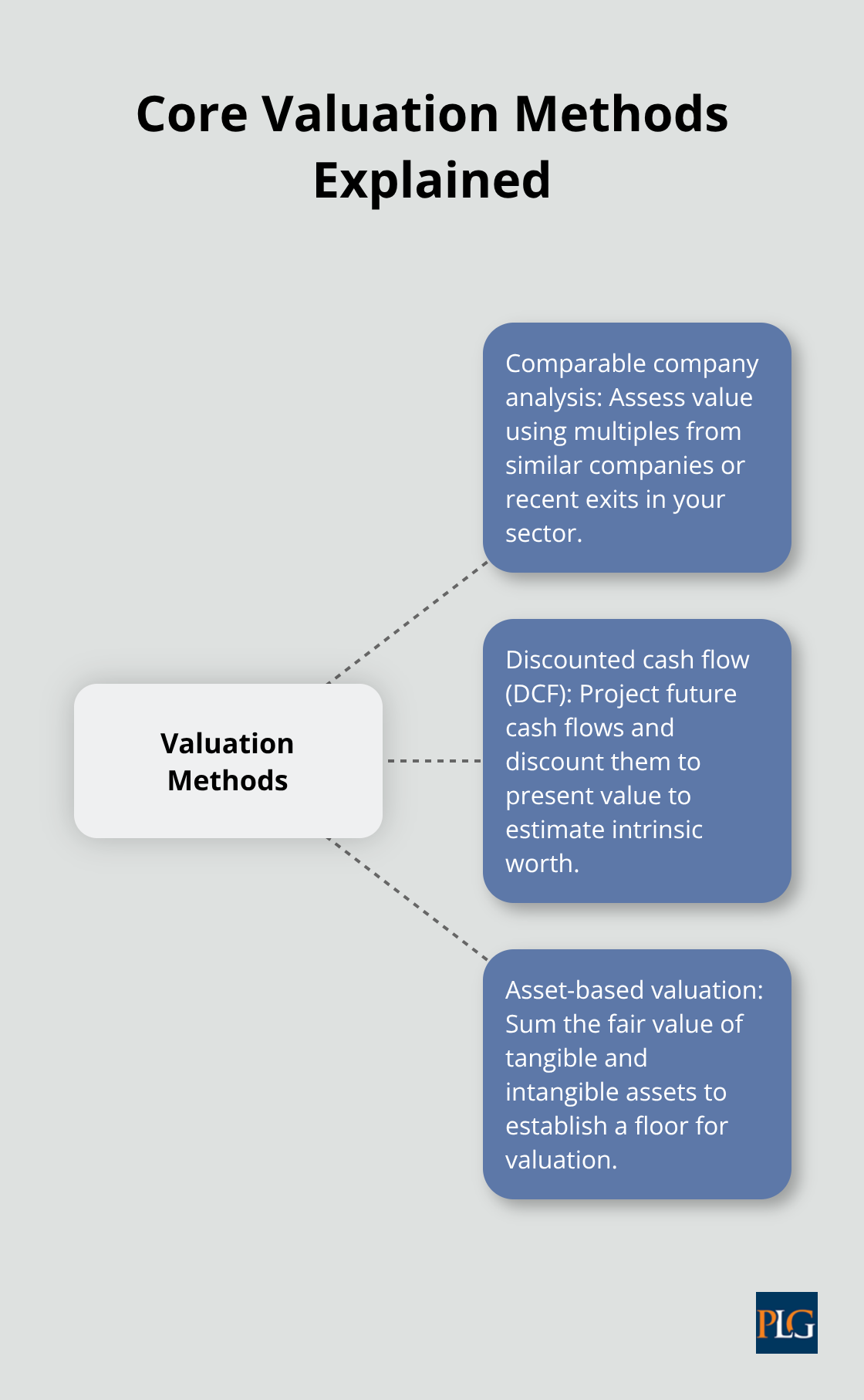

How your company is valued affects how much equity you give up in funding rounds and how much you pay in acquisitions. Three main valuation approaches dominate corporate finance: comparable company analysis (looking at what similar companies sold for), discounted cash flow analysis (projecting future earnings and discounting them to present value), and asset-based valuation (valuing tangible and intangible assets).

Early-stage startups with no revenue rarely use discounted cash flow because projections are too speculative; instead, venture investors rely on comparable company multiples or market benchmarks. A Series A software startup in San Francisco might command a 5–8x revenue multiple based on comparable exits, while a mature SaaS business might trade at 10–15x revenue. These multiples shift with market conditions-during the 2023–2024 correction, San Francisco tech valuations compressed significantly as investor appetite declined.

If you’re raising capital, understanding which valuation method investors are using helps you spot fair offers from inflated ones. If you’re acquiring another company, undervaluation happens when the seller doesn’t know what comparable transactions achieved; using public data on recent M&A deals in your sector gives you negotiating leverage. Understanding what a fair deal looks like before entering negotiations prevents both underselling and overpaying, which is why many San Francisco companies work through their valuation assumptions with counsel before discussions begin.

What Securities Laws Apply When You Raise Capital

Raising capital in California triggers overlapping federal and state securities laws that govern how you approach investors, what you must disclose, and when you file documents. Most San Francisco startups avoid full SEC registration by using exemptions under Regulation D, Regulation A, or California’s Limited Offering Exemption, but choosing the wrong path creates compliance gaps that regulators and investors exploit later. Your exemption choice determines your investor pool, your filing costs, your timeline, and your ongoing reporting burden.

Regulation D: The Venture Financing Standard

Regulation D Rule 506(b) dominates venture financing in San Francisco because it allows unlimited accredited investors with no general solicitation-you pitch only to people you know or have a preexisting relationship with, and they must have a net worth of at least $1 million excluding their primary residence or annual income above $200,000. Rule 506(c) lets you advertise broadly and use general solicitation, but all investors must be accredited and you must verify their accreditation status, which adds cost and friction. If you have fewer than 35 non-accredited investors who are sophisticated (meaning they understand the risks), Rule 506(b) works fine without verification requirements.

Most venture rounds use Rule 506(b) because venture investors are accredited by definition and the absence of advertising requirements speeds up the process. However, if you want to run a public marketing campaign to find investors-posting on LinkedIn, running ads, hosting webinars open to the public-Rule 506(c) is your only option, though the accreditation verification requirement typically pushes costs up by $10,000 to $25,000 depending on your investor base size.

California State Compliance and Filing Requirements

Federal exemptions do not preempt California state law; you must also comply with California’s merit review standards and file appropriate notices or qualifications with the Department of Financial Protection and Innovation. California uses a merit standard requiring that offerings be fair, just, and equitable-meaning the state can reject an offering even if it’s federally exempt if the terms are unreasonable or the offering structure is unfair to investors.

California’s Limited Offering Exemption under Section 25102(f) lets you raise from up to 35 purchasers with a preexisting relationship or sufficient investment sophistication without federal preemption, but you cannot advertise and you must file a notice with the DFPI and pay a filing fee. For offerings under $1 million in California, the Small Corporate Offering Registration process uses standardized forms and streamlines the DFPI review, reducing legal costs and review time.

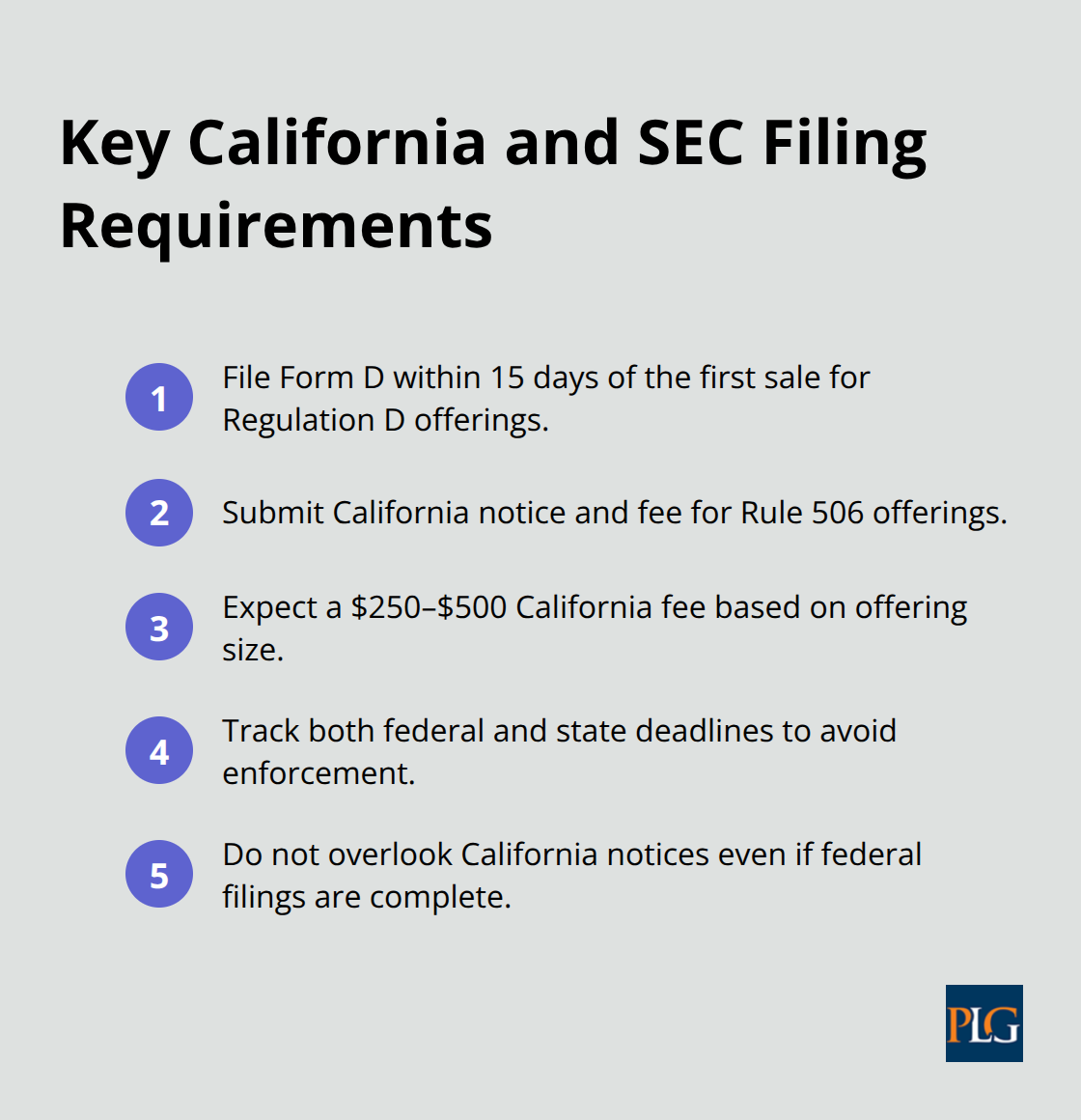

Form D filings with the SEC are required for Regulation D offerings within 15 days of the first sale, and late filing or failure to file triggers SEC enforcement risk and can void your exemption. California requires a separate notice filing and fee for Rule 506 offerings; the fee is typically $250 to $500 depending on the offering size. Many San Francisco companies miss California notice requirements because they focus only on federal compliance, then face DFPI enforcement letters months after closing.

Alternative Exemptions for Different Fundraising Goals

For smaller raises under $5 million, Regulation Crowdfunding through SEC-registered platforms like Wefunder or SeedInvest works if you accept non-accredited investors, though investment limits apply per investor and you face ongoing reporting obligations to the platform and the SEC. If you’re raising between $20 million and $75 million, Regulation A Tier 2 lets you access non-accredited investors with investment caps, file an offering circular with the SEC, and skip state qualification in most cases-but the SEC review process takes 4–6 months and costs $50,000 to $150,000 in accounting and legal fees.

The choice between these paths isn’t academic: a $2 million seed round under Rule 506(b) costs $8,000 to $15,000 in legal and filing fees and closes in 6–8 weeks, while a $50 million Regulation A Tier 2 offering costs $100,000 to $200,000 and takes 5–6 months. Map your fundraising timeline and target investor base first, then select the exemption that minimizes cost and delay without creating compliance risk down the road.

Disclosure Obligations and Antifraud Rules

Antifraud rules apply to all offerings regardless of exemption, meaning you cannot make false or misleading statements about the company, its financials, or the investment risk, even in casual conversations with potential investors. If you’re raising multiple tranches over time, track your aggregate sales carefully-Rule 504 caps raises at $10 million in any 12-month period, and Regulation Crowdfunding caps raises at $5 million in 12 months, so exceeding these limits voids your exemption retroactively.

Disclosure obligations vary by exemption: Rule 506(b) requires minimal disclosure for accredited-only offerings, but if you have even one non-accredited investor, you must provide audited or reviewed financial statements and detailed business disclosures. Regulation A Tier 2 and Regulation Crowdfunding require ongoing annual reporting to investors and the SEC, creating compliance obligations that persist long after the offering closes. Many founders view the offering as the finish line and stop tracking their obligations, but failure to file annual reports triggers SEC enforcement and can expose you and your officers to personal liability.

Disclosure standards also require you to update investors on material changes-if your company misses a revenue target, loses a major customer, faces litigation, or changes its business plan materially, you must disclose this promptly to your investor base, not just to new investors. This obligation applies even for Rule 506(b) offerings with accredited investors only, because antifraud rules require that material information reach investors when they make decisions about their holdings. Understanding which exemption you’ve chosen and what it requires determines whether your capital raise protects your company or exposes it to enforcement action and investor disputes.

How to Structure Deals and Protect Your Business

Structuring transactions correctly determines whether you capture value or leave money on the table, and it shapes your legal exposure for years after closing. Most San Francisco companies approach deal structure reactively-responding to what the other party proposes-but the companies that negotiate better outcomes plan their structure before discussions begin. This means understanding what financial and legal risks matter most to your business, what protections are actually enforceable, and where tax planning can reduce your total cost of capital.

Investigate the Company You’re Acquiring

Due diligence investigates the company you’re acquiring or the investor you’re taking money from, and it reveals hidden liabilities or overvalued assumptions that most founders miss. Many founders skip rigorous due diligence because they want to close quickly, then discover six months later that the acquired company’s customer contracts contain change-of-control clauses that let clients terminate, or that promised revenue rests on handshake agreements with no documentation. Kroll and similar firms charge $50,000 to $200,000 for comprehensive due diligence on mid-market deals, and this investment pays for itself when it prevents acquisition of undisclosed liabilities.

Start with financial records-request three years of tax returns, audited or reviewed financial statements, and detailed revenue and expense reports broken down by customer and product line. If the target company’s financial statements don’t reconcile with tax returns, that signals either accounting errors or intentional misstatement. Request customer contracts and validate that major customers actually exist and that their contracts don’t contain termination rights triggered by the acquisition. In one 2023 acquisition of a San Francisco software company, due diligence revealed that 40% of reported annual recurring revenue came from a single customer with a 30-day termination clause-the deal price dropped 25% once this became clear. Request litigation records, regulatory filings, and employment agreements to identify pending disputes or obligations the seller hasn’t disclosed. Many sellers omit litigation or regulatory investigations because they hope they’ll resolve quietly, but once you own the company, you own the liability.

Shift Risk Through Contract Language

Contract negotiation determines who bears the cost when something goes wrong-whether the seller misrepresented revenue, whether a key employee leaves, whether regulatory changes make the business model unviable. San Francisco acquirers often accept seller-friendly language because they’re focused on closing speed, then face disputes when the target company’s performance falls short of expectations. The most important protective clauses are representations and warranties from the seller about the accuracy of financial statements, the absence of undisclosed liabilities, and the validity of customer contracts and intellectual property. These aren’t theoretical protections-they’re the basis for indemnification claims when the seller’s statements prove false.

Include a purchase price adjustment or earn-out structure that ties part of the payment to post-closing performance. If the seller claims the business generates $5 million in annual recurring revenue, structure the deal so that 30–40% of the purchase price depends on hitting that revenue target in the year following closing. This aligns the seller’s incentives with accuracy and gives you recourse if the numbers were inflated. Escrow arrangements where 10–20% of the purchase price sits in trust for 12–18 months give you leverage to pursue indemnification claims if representations prove false. Many sellers resist escrow because it reduces their cash at closing, but escrow is standard in San Francisco M&A deals and signals that you’re taking due diligence seriously.

Non-compete and non-solicitation clauses prevent the seller from launching a competing business or recruiting your employees immediately after closing. California courts rarely enforce non-competes under state law, so focus instead on customer non-solicitation clauses that prevent the seller from recruiting your customers for 12–24 months. Intellectual property assignment clauses must explicitly transfer all patents, trademarks, and software code to the buyer; vague language creates disputes later about who owns what. Many San Francisco founders inherit IP disputes because the original purchase agreement didn’t clearly assign all IP or because the seller retained rights to certain technology. Working with counsel to draft clear, specific language prevents these disputes from arising in the first place.

Reduce Your Deal Cost Through Tax Structure

How you structure a transaction for tax purposes can reduce your actual cost of capital by 15–30% compared to a naive approach. If you’re acquiring another company, structuring the deal as an asset purchase versus a stock purchase changes what tax basis you get in the acquired assets and whether you can step up the basis to fair market value. In an asset purchase, you buy specific assets and assume certain liabilities, and you get a stepped-up basis in those assets equal to what you paid for them-this creates depreciation deductions that reduce taxable income over time. In a stock purchase, you buy the company’s shares, and the seller’s old basis carries forward, meaning you get fewer depreciation deductions. The tax savings from an asset purchase structure can amount to hundreds of thousands of dollars on larger deals, which is why acquirers typically prefer asset purchases even though they’re operationally messier.

If you’re raising capital through equity financing, the tax treatment of different security types matters for your long-term cost of capital. Preferred stock issued to investors receives preferential treatment in liquidation and often has dividend rights, which creates a higher cost of capital than common stock because investors demand returns for the additional rights. Convertible notes and SAFEs defer the valuation question until a future priced round, which reduces upfront negotiation friction but can create unpleasant surprises when the conversion terms are finalized. If you raise $1 million on a convertible note with a $5 million valuation cap and the Series A round values the company at $20 million, your note converts at the $5 million cap, meaning your investors get shares worth 20% more than they would have at the Series A valuation. This dilution is the cost of deferring the valuation conversation.

Navigate International Transaction Structures

If you’re structuring an international transaction, consider where different entities are taxed and whether you can defer or reduce US tax on foreign income through proper entity structure. Many San Francisco companies with international operations use holding companies in lower-tax jurisdictions to manage IP and licensing arrangements, but this strategy requires careful documentation and compliance with transfer pricing rules. The IRS scrutinizes transfer pricing on transactions between related entities, so document the economic rationale for any pricing you use between your US operations and foreign subsidiaries. Working with counsel experienced in international corporate structure before you set up foreign entities prevents costly restructuring later when the IRS challenges your transfer pricing approach.

Final Thoughts

Corporate finance and securities law decisions compound over time, and getting them right early prevents costly restructuring later. Structure your capital stack deliberately based on your cash flow and growth timeline, choose your securities law exemption before you start fundraising, and investigate thoroughly before you commit capital to acquisitions or accept investor money. Companies that skip these steps often face avoidable problems-missed filing deadlines that void exemptions, acquisition surprises that destroy deal economics, or capital structures that create conflicts between founders and investors down the road.

The most common pitfall is treating corporate finance and securities law as compliance checkboxes rather than strategic decisions. Your choice between debt and equity shapes your company’s trajectory for years, your choice of securities exemption determines your investor pool and your ongoing reporting burden, and your due diligence depth determines whether you overpay for acquisitions or miss hidden liabilities. California’s merit review standards and state filing requirements create a second layer of obligations that many San Francisco companies overlook, and missing California notice filings triggers DFPI enforcement even when your federal exemption is solid.

The right time to seek legal guidance is before you make irreversible decisions, not after. We at Primum Law Group help San Francisco startups and growing companies navigate these decisions through outsourced general counsel, venture capital transactions, and business structuring services that align your legal strategy with your business goals. The cost of getting advice upfront is far lower than the cost of fixing problems after they arise.