Valuing a startup is one of the hardest decisions investors face. Get the number wrong, and founders either leave money on the table or price themselves out of funding rounds.

We at Primum Law Group help founders and investors navigate this challenge by breaking down the venture capital valuation methods that actually work. This guide walks you through the frameworks, metrics, and common pitfalls that determine whether your startup gets valued fairly in San Francisco’s competitive funding landscape.

Three Frameworks That Matter for Startup Valuation in San Francisco

Discounted Cash Flow Analysis

The Discounted Cash Flow method works backward from a startup’s future earnings to today’s value. You project five to ten years of cash flows, apply a discount rate that reflects risk and the time value of money, then add a terminal value for anything beyond your forecast window. For a pre-revenue startup, this means estimating when the company will turn profitable and how much cash it will generate annually.

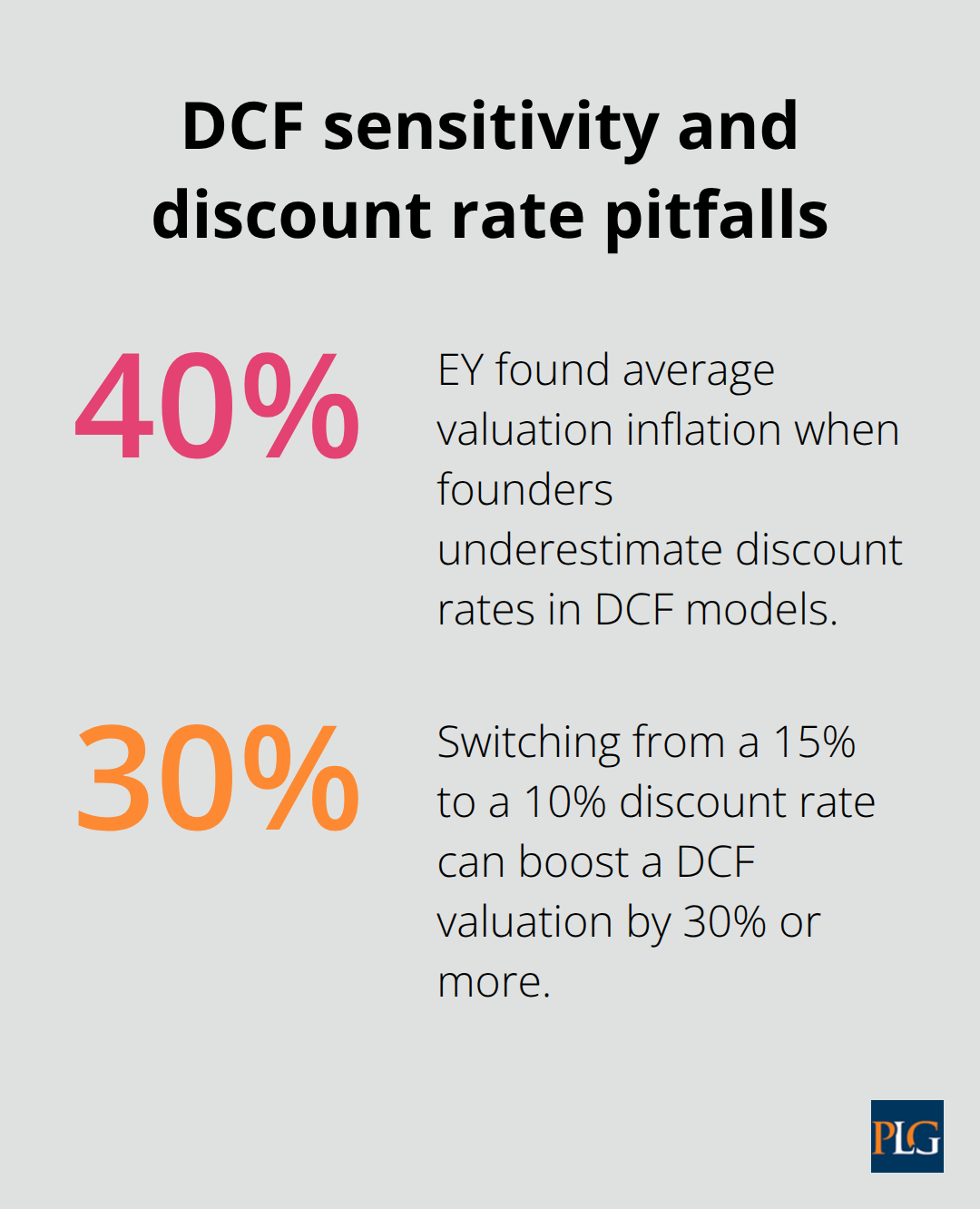

The math itself is straightforward: divide each year’s projected free cash flow by (1 + discount rate) raised to the power of that year, then sum the results. The challenge is that small changes in assumptions create massive valuation swings. If you assume a 10% discount rate instead of 15%, your valuation could jump by 30% or more.

EY’s 2019 analysis of startup DCF models showed that founders typically underestimate their discount rate, inflating valuations by an average of 40%. Build your five-year financial model with realistic revenue growth tied to actual customer traction, not wishful thinking. Include working capital changes because they materially affect free cash flow.

Use a terminal growth rate between 2% and 3%, anchored to inflation, rather than assuming your startup will grow forever at 20%. Treat your DCF as a ballpark figure, not gospel.

Comparable Company Analysis

Comparable Company Analysis takes a different path: it finds similar startups that recently raised funding or sold and uses their valuations as benchmarks for yours. If five comparable SaaS startups in your space raised Series A rounds at 8x annual recurring revenue, and your startup has 500k ARR, then your valuation range sits around 4 million dollars.

The strength of this method is that it grounds your valuation in actual market prices, not theoretical models. PitchBook and Crunchbase publish thousands of funding rounds annually, giving you real data. The weakness is that early-stage startups rarely have perfect comparables, and private deal terms stay hidden. You see the headline valuation but not the liquidation preferences, anti-dilution clauses, or other terms that actually matter to investors.

Select five to ten startups that match your stage, market, and business model, then calculate the median multiple across recent rounds. If your internally derived valuation falls within 20% of the comparable range, you are in reasonable territory. If you sit far outside that range, document why: a stronger team, faster traction, better unit economics, or defensible technology. Use comparables as a sanity check, not the final answer.

The Venture Capital Method

The Venture Capital Method cuts through the noise by asking what an investor needs to earn. An investor targets a 30% annual return over five years. Your startup projects 100 million dollars in exit value in Year 5. Divide 100 million by (1.30 to the power of 5) and you get 27 million dollars as the post-money valuation today. Subtract the investment amount and you have pre-money valuation.

This method is brutal in its honesty: it forces you to name an exit value and a timeline, then work backward. Most founders hate it because it exposes how unlikely their 10x exit really is. That’s precisely why VCs prefer it. You cannot hand-wave your way to a high valuation when the VC Method is on the table. Use it early in venture capital financing conversations so both sides understand what the numbers actually mean.

These three frameworks form the foundation of how investors think about startup value. Each one reveals different truths about your business, and the metrics you track-revenue multiples, customer acquisition costs, and burn rate-determine which method makes the most sense for your stage.

Key Metrics That Drive Startup Valuations

Investors value startups based on measurable performance, not founder charisma. Revenue multiples, customer acquisition costs, and burn rate form the backbone of every valuation conversation. If you cannot articulate these numbers clearly, your valuation pitch collapses regardless of which framework you use.

Revenue Multiples and Growth Efficiency

A SaaS startup with 1 million dollars in annual recurring revenue trading at an 8x multiple appears worth 8 million dollars, but that multiple only holds if churn stays below 5% annually and customer acquisition cost sits below 30% of lifetime customer value. CB Insights analyzed 1,500 SaaS companies and found that startups with churn above 10% rarely command multiples higher than 3x to 4x, even with strong growth.

Growth rate matters more than absolute revenue. A company growing 50% year-over-year justifies higher multiples than a larger competitor growing 15%, because investors bet on trajectory, not current size. Calculate your magic number by dividing new annual recurring revenue added in a quarter by total sales and marketing spend from that quarter. A magic number above 0.75 signals efficient growth. Anything below 0.5 means you burn cash to acquire customers at unsustainable rates, and investors will demand a lower valuation or pass entirely.

Customer Acquisition Cost and Lifetime Value

Your unit economics determine whether investors see a viable business. If you spend 500 dollars acquiring a customer and that customer generates 2,000 dollars in total revenue over their relationship with you, your LTV-to-CAC ratio reaches 4 to 1, which most investors consider healthy. This assumes your customer stays for at least three years.

If your average customer leaves after 18 months, that same customer generates only 1,000 dollars, dropping your ratio to 2 to 1. Most founders underestimate CAC by excluding salaries, overhead, and failed marketing experiments. Include fully loaded costs. Crunchbase shows that B2B SaaS companies typically spend 18 to 24 months recouping their customer acquisition costs through gross margin.

Burn Rate and Runway

Burn rate and runway determine whether your startup survives long enough to reach the next milestone. Burn rate is how much cash you spend monthly. Runway is how many months you can operate at that burn rate before cash runs out. If you raise 2 million dollars and burn 150,000 dollars monthly, your runway reaches approximately 13 months.

That number controls everything about your next fundraising timeline. Most founders try for 18 to 24 months of runway at the time of funding, giving them time to hit milestones that justify higher valuations in the next round. If you only have 12 months of runway, you negotiate from weakness. Investors know you must raise again soon, and they use that urgency to push down valuations.

Building Your Metrics Foundation

Track these metrics monthly and build them into your financial model. Show investors a clear path to unit-positive economics and a declining burn rate as revenue grows. The companies that command premium valuations prove they can grow revenue faster than they grow expenses. These performance indicators set the stage for understanding how different valuation methods apply to your specific situation and stage.

Common Valuation Mistakes and How to Avoid Them

Overestimating Growth Projections

Most founders inflate revenue projections because they conflate market opportunity with achievable growth. Your total addressable market might be 500 million dollars, but that does not mean you will capture even 1% of it. When you project 200% year-over-year growth for five consecutive years, investors mentally discount your entire financial model by 50% because they have seen this pattern repeatedly.

Correlation Ventures analyzed 200 failed startups and found that overestimated growth projections ranked as the number one reason valuations collapsed during due diligence. The fix is brutal honesty: tie your growth model to actual customer acquisition data and sales pipeline, not market size. If you currently acquire 10 customers monthly and plan to hire two additional salespeople, project what those hires realistically add based on your historical cost per acquisition. Most founders add 500% more revenue from one new hire when 30% is more defensible.

Investors will test your assumptions by asking about competitive win rates, average deal size, and sales cycle length. If you cannot answer these questions with concrete numbers from your actual business, your growth projections get thrown out and your valuation gets cut accordingly.

Ignoring Market Size and Competitive Intensity

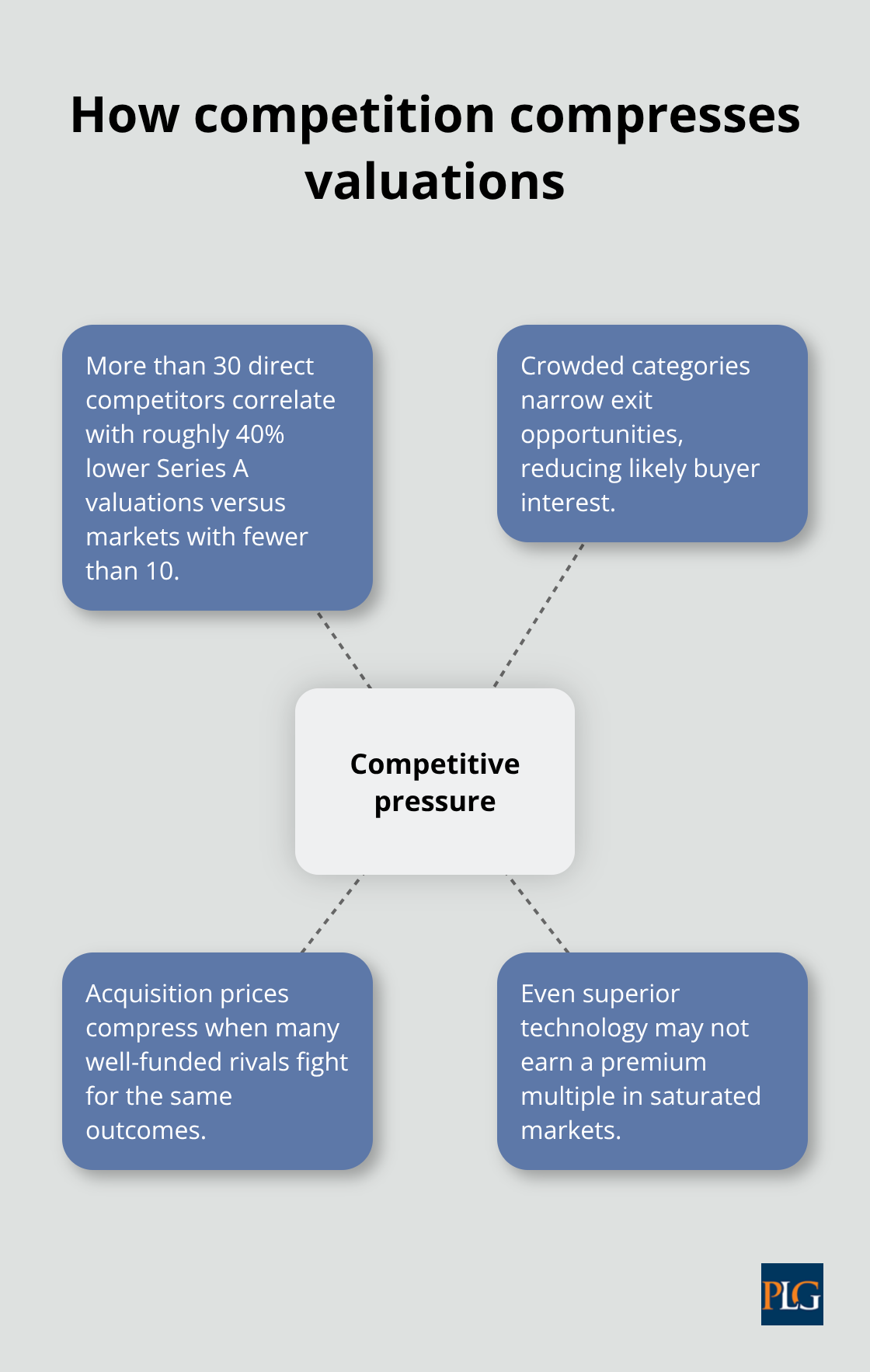

A crowded market with 50 well-funded competitors shrinks your valuation multiple even if you have superior technology, because exit opportunities narrow and acquisition prices compress. Crunchbase data shows that startups in markets with more than 30 direct competitors raise Series A rounds at 40% lower valuations than those in markets with fewer than 10 competitors (controlling for growth rate and customer traction).

Ignoring market size and competitive intensity kills more valuations than any other mistake because it exposes whether you have thought seriously about your business. You must understand who your competitors are, what they charge, and how they acquire customers. This competitive analysis directly affects your valuation because it determines whether acquirers will pay a premium for your technology or simply build it themselves.

Failing to Account for Risk and Dilution

You fail to account for risk and dilution when you ignore how future funding rounds will water down current valuations. If you raise Series A at a 20 million dollar post-money valuation on a 30% discount rate, but your business requires three more funding rounds before exit, your founders’ ownership stake shrinks from 70% to roughly 15% by the time you sell. The dilution is mathematically inevitable, yet most founders price their Series A as if it will be their last round.

Work backward from your exit scenario and model each funding round using the Venture Capital Method. Calculate your pre-money valuation for Series B and Series C based on milestones you need to hit, not wishful thinking about how much more valuable you will be. This forces you to understand the full dilution path and negotiate Series A terms that preserve meaningful founder ownership. When you model dilution accurately, you make better decisions about how much capital to raise in each round and what valuation you should accept today.

Final Thoughts

Startup valuation requires you to apply multiple frameworks to your specific stage and market conditions rather than chase a single number. The Discounted Cash Flow method works when you have revenue and can project cash flows with confidence, while Comparable Company Analysis grounds your valuation in actual market prices. The venture capital valuation method forces you to name an exit value and timeline, then work backward to determine what investors need to earn today.

Accurate valuation determines whether you raise capital at terms that preserve founder ownership or accept dilution that makes the business not worth building. Overestimating growth, ignoring competitive intensity, and failing to model dilution across multiple rounds tank valuations during due diligence. When you apply the venture capital valuation method rigorously and track revenue multiples, customer acquisition costs, and burn rate monthly, you build credibility with investors and negotiate from strength.

We at Primum Law Group help founders and investors structure deals that align incentives and protect both parties through venture capital transactions, cap table management, and term sheet negotiation. Contact our team to discuss your valuation strategy and ensure your deal terms reflect the true value of your business.