Venture capital trends are shifting faster than ever, and the landscape looks nothing like it did five years ago. Series A funding has become harder to secure, while new players like micro-VCs are reshaping how early-stage companies get capital.

At Primum Law Group, we’re tracking how AI, climate tech, and fintech are dominating investor attention. Geography matters too-the Bay Area’s dominance is fading as funding spreads across new hubs and international markets.

Early-Stage Funding Shifts and Series A Crunch

The Series A Reality Check

Series A funding has become brutally selective. In 2025, startups face a dramatically different environment than even two years ago. The data tells a clear story: seed valuations dropped 20 to 30 percent from 2023 peaks, according to the VC Lab Q2 2025 Venture Trends survey. This correction forces founders to prove unit economics and revenue traction before investors write larger checks.

The old playbook of growth-at-all-costs no longer works. Founders must now demonstrate clear paths to profitability, not just ambitious user acquisition targets. This shift favors startups with disciplined spending and honest projections over those chasing vanity metrics. Investors scrutinize burn rates and runway calculations far more closely than they did in 2023.

Micro-VCs and Angel Networks Fill the Gap

Micro-VCs and angel networks have filled gaps left by traditional venture firms retreating from early-stage bets. These smaller investors move faster and accept higher risk because they’re not managing billion-dollar funds with limited partner patience. Angel networks in the Bay Area actively deploy capital into pre-seed and seed rounds, often providing $500,000 to $2 million per company.

They bring operational experience alongside capital, which matters more than ever. Meanwhile, established VC funds increasingly skip seed rounds entirely, waiting until Series A when companies show real traction. This two-tier system rewards founders who can bootstrap longer or tap angel capital early. Startups that secure 12 to 18 months of runway before pursuing Series A have dramatically better negotiating power and can command higher valuations.

The Profitability Pressure Reshapes Spending

Time to profitability has extended significantly, but the tolerance for runway has shrunk. Founders now spend 36 to 48 months reaching profitability on average, yet investors expect tighter monthly burn rates. This contradiction forces hard choices: hire slower, focus on fewer products, or pursue revenue faster than growth-focused competitors.

The winners treat profitability as an engineering problem, not an afterthought. They model unit economics ruthlessly, cut unprofitable customer segments early, and build unit-level margins before scaling. Startups that reach Series A with positive unit economics or clear paths to contribution margin profitability command valuations 30 to 50 percent higher than peers still burning cash on unproven channels. These founders understand that investors now reward discipline over ambition alone.

As Series A becomes harder to secure, the strategic focus areas that attract capital have shifted dramatically. AI, climate tech, and fintech now dominate investor attention-and the capital flowing into these sectors tells a compelling story about where founders should direct their efforts.

Strategic Focus Areas Driving VC Investment

Where VC Money Actually Flows Right Now

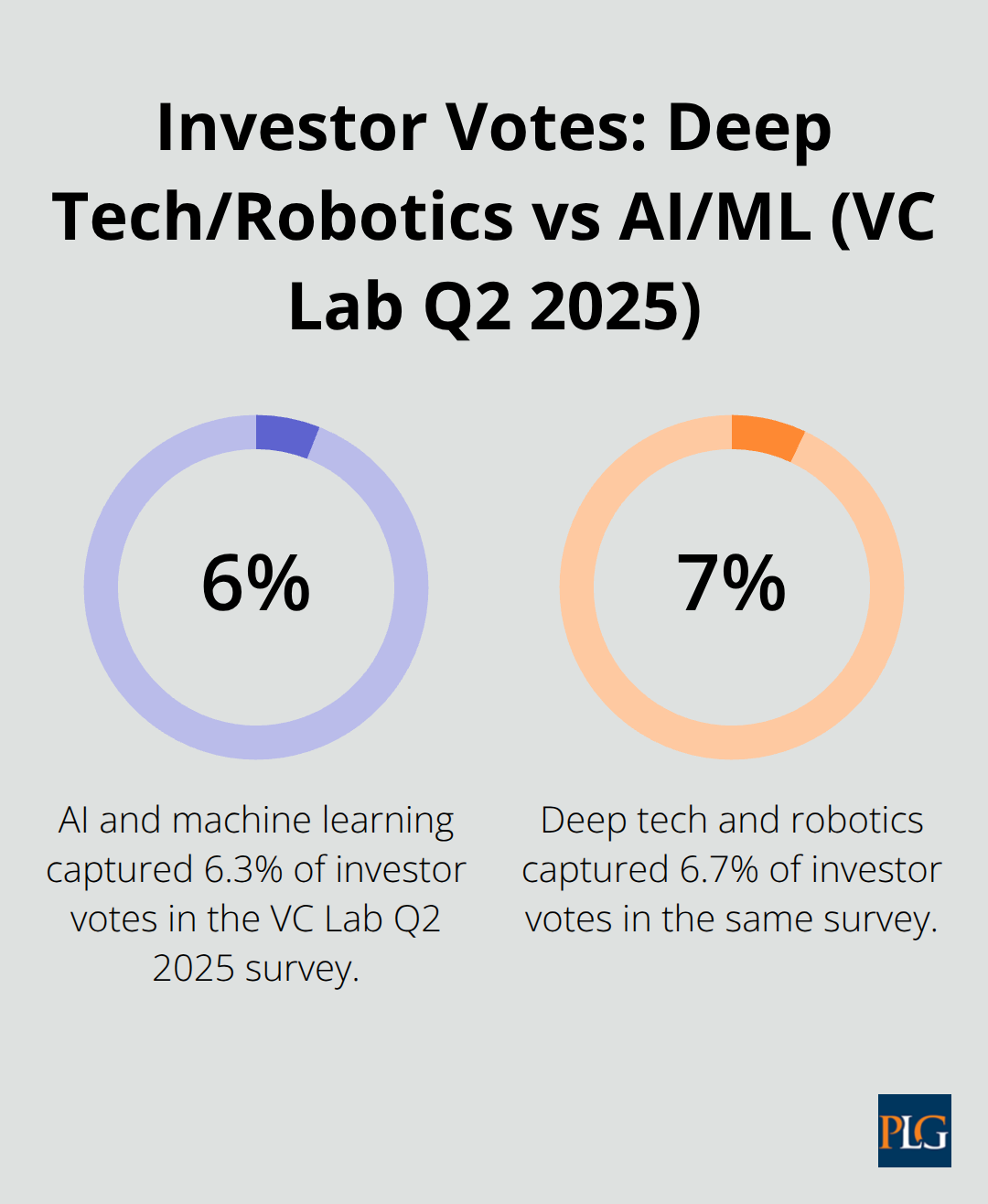

AI and machine learning dominate the conversation, but the real story is more nuanced. According to the VC Lab Q2 2025 Venture Trends survey, deep tech and robotics captured 6.7 percent of investor votes, edging out AI and machine learning at 6.3 percent. This shift signals investor appetite for hardware-enabled technologies with longer development cycles and defensible moats. AI isn’t losing relevance-it becomes table stakes instead.

The startups that win capital now use AI as an operational tool rather than their entire value proposition. They embed machine learning into supply chain optimization, manufacturing quality control, and robotics systems. Founders who pitch pure language models or generic AI applications face brutal skepticism. Investors reward teams that solve specific problems in verticals like manufacturing, logistics, or industrial automation where AI creates measurable cost reductions or revenue uplift.

Climate tech and sustainability attract capital because they align with regulatory tailwinds and corporate purchasing power. Fintech remains active, but the sector has matured past the hype cycle. Decentralized finance and Web3 innovations continue attracting capital, though at more realistic valuations than 2021 peaks. The practical takeaway: founders should identify which technology solves a real problem customers will pay for, not which technology sounds most cutting-edge.

San Francisco’s AI Concentration Reshapes Capital Flow

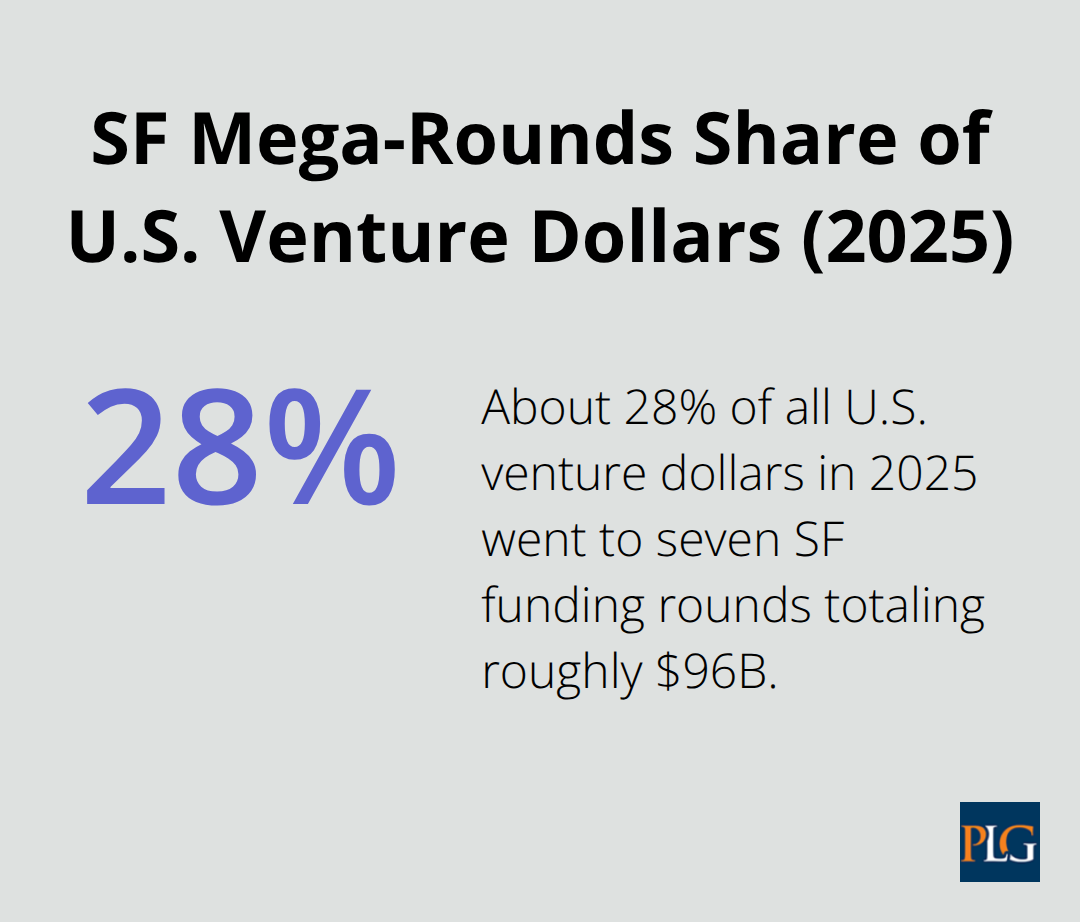

San Francisco’s AI dominance reshapes where capital flows. Seven of the top ten largest funding rounds in 2025 went to SF startups, totaling roughly 96 billion dollars, which represents about 28 percent of all venture dollars nationwide. OpenAI’s 40 billion dollar funding round alone accounted for more than 10 percent of U.S. startup venture dollars in 2025. This concentration creates a talent and capital feedback loop: more AI engineers attract more startups, which attract more capital and talent.

Garry Tan of Y Combinator reinforced this by telling founders they must be in San Francisco, a move that reversed the Rise of the Rest trend and pulled investment back toward the Bay Area. For founders outside San Francisco, this creates real friction. Competing for Series A capital becomes harder when the best-funded AI startups operate in one geographic cluster.

The solution isn’t relocating at all costs. Instead, founders should build deep domain expertise in their specific AI application and prove unit economics before raising Series A. Investors increasingly reward founders who articulate sourcing strategy, trade compliance, and tariff exposure as a leadership signal. These operational details differentiate credible teams from those chasing AI hype.

Building Defensibility Beyond Technology

Investors now scrutinize business model durability more carefully. Cybersecurity has become the currency of startup value, according to Deloitte Insights. Strong cyber defenses correlate with higher valuations because they reduce investor risk and regulatory exposure. Startups should develop a scalable cybersecurity plan early, not as an afterthought before Series A. This means implementing basic controls-data encryption, access management, incident response protocols-from day one.

Climate tech founders must understand tariff implications and supply chain costs. Robust tariff strategies (bonded warehouses, optimized free trade agreements, smart customs documentation) can meaningfully reduce tariff liabilities. Fintech teams need to map regulatory requirements by jurisdiction before scaling internationally. The pattern across all three sectors is identical: founders who combine strong technology with operational sophistication and risk awareness attract capital faster and at higher valuations than pure technologists.

Geographic Shifts Beyond the Bay Area

While San Francisco dominates AI funding, capital flows increasingly toward geographic diversification in other sectors. Founders in climate tech and fintech find receptive investors outside the Bay Area, particularly when they demonstrate strong unit economics and regulatory readiness. This geographic shift creates opportunities for teams that build deep local expertise and relationships rather than chasing the SF hype cycle.

The next section examines how demographic shifts and international capital flows are reshaping the entire venture landscape, creating new pathways for founders who understand these broader market movements.

Geographic and Demographic Shifts Reshaping Capital Access

San Francisco’s AI dominance masks a critical reality: capital fragments geographically in ways that create real opportunities for founders willing to move away from the hype. The Bay Area captured 44.9 percent of all U.S. venture dollars in 2025 according to PitchBook and NVCA data, but this concentration signals weakness elsewhere rather than strength in the Bay Area. Founders in climate tech, fintech, and robotics secure meaningful capital outside San Francisco when they build deep domain expertise and prove unit economics in their specific markets. The Presidio has emerged as San Francisco’s premier venture hub, hosting prominent firms like Felicis, Forerunner, and Headline in a dense cluster that operators describe as the new Sand Hill Road. This geographic centralization within SF itself creates friction for distributed teams. Demand for remaining Presidio space exceeds available supply by more than three times, according to Presidio Trust data, making it nearly impossible for emerging managers to secure prime locations. Founders should evaluate whether relocating to the Presidio actually accelerates fundraising or simply increases operating costs. Many climate tech and fintech teams have found that strong unit economics and regulatory compliance in secondary markets attract Series A capital just as effectively as proximity to Sand Hill Road.

Founder Diversity Opens New Capital Pathways

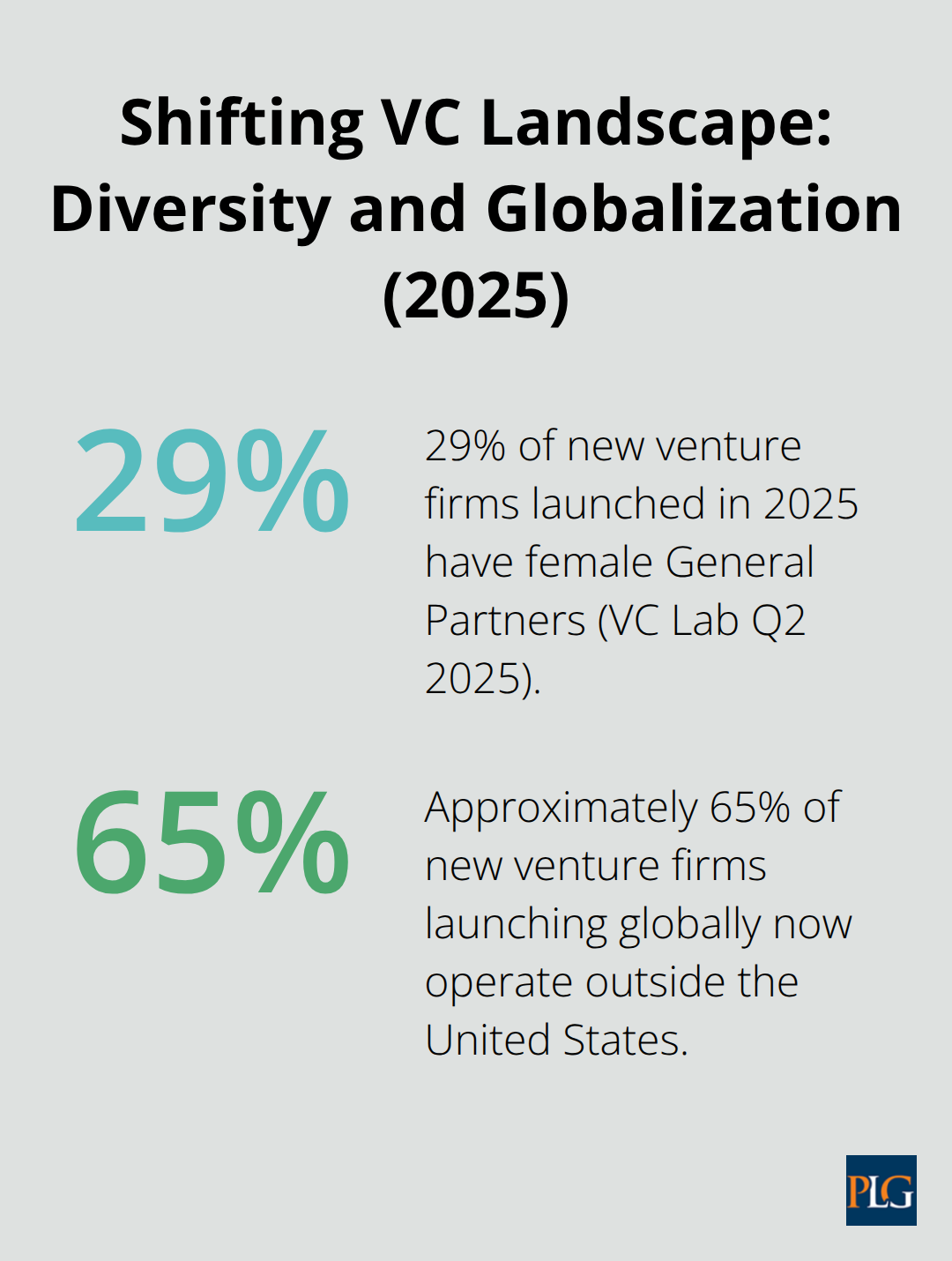

Demographic shifts in founder composition reshape which teams attract capital, though progress remains uneven. The VC Lab Q2 2025 Venture Trends survey showed that 29 percent of new venture firms launched in 2025 have female General Partners, signaling meaningful structural change in who controls capital allocation. However, this statistic masks persistent gaps in early-stage capital access. Startups with diverse founding teams often face longer fundraising timelines despite identical business fundamentals.

Teams should document customer acquisition costs, retention rates, and pathways to profitability with obsessive precision. Investors increasingly reward founders who articulate supply chain strategy and tariff exposure as a leadership signal, creating opportunities for teams with international operational experience or deep sector knowledge that traditional VC firms may overlook. International LPs and family offices expanding VC allocations now comprise a growing share of capital, and these investors often evaluate founder teams through different lenses than legacy Sand Hill firms. For founders from underrepresented backgrounds, this LP diversification creates genuine pathways to capital without requiring relocation to the Bay Area or navigation of exclusionary network dynamics.

International Capital Flows Reshape Startup Valuations

International capital flows into U.S. venture markets have accelerated despite geopolitical uncertainty ranking as the top VC trend in Q2 2025 according to the VC Lab survey. Approximately 65 percent of new venture firms launching globally now operate outside the United States, creating reciprocal capital flows into American startups from European, Asian, and Middle Eastern investors. This international capital influx matters because foreign LPs often evaluate startups against different benchmarks than U.S. investors and show higher tolerance for longer time horizons in deep tech and climate solutions. Founders should understand that international investors increasingly require robust tariff strategies and supply chain documentation before committing capital. Deloitte analysis emphasizes that founders who articulate sourcing strategy and customs documentation decisions signal operational maturity that attracts international capital. Startups with global supply chains or international revenue exposure should model tariff scenarios and prepare multi-jurisdiction regulatory analyses before Series A conversations. This operational sophistication appeals specifically to international LPs who face currency and tariff risks themselves. For U.S. founders, international capital access often requires demonstrating risk awareness that purely domestic competitors overlook.

Final Thoughts

The venture capital trends reshaping investment today force founders and investors to rethink fundamental assumptions about growth, geography, and risk. Series A has transformed into a profitability checkpoint rather than a growth accelerator, while micro-VCs and angel networks now control meaningful capital allocation. AI concentration in San Francisco creates both opportunity and friction-founders outside the Bay Area can build valuable companies by proving unit economics and operational discipline rather than chasing proximity to Sand Hill Road.

The sectors attracting capital have matured beyond hype cycles. Deep tech and robotics now edge out pure AI applications because investors reward teams solving specific problems with measurable returns. Climate tech and fintech founders who understand tariff implications, regulatory requirements, and supply chain risks command higher valuations than pure technologists, and cybersecurity has become table stakes rather than an afterthought. International capital flows into U.S. markets create new pathways for founders willing to articulate supply chain strategy and tariff exposure as leadership signals.

Founders who combine strong technology with operational sophistication and risk awareness attract capital faster and at higher valuations than pure technologists. We at Primum Law Group help founders and investors navigate these shifting dynamics through startup counseling and venture capital transactions tailored to your specific market position and risk profile. The founders who succeed in 2025 and beyond build disciplined unit economics, develop operational maturity beyond technology, and understand their regulatory and tariff landscape before raising Series A.