Founders often face a critical decision when seeking growth capital: should they pursue venture capital or private equity? These two funding paths look similar on the surface, but they operate under completely different rules.

At Primum Law Group, we’ve guided countless business owners through this choice. Understanding the distinctions between venture capital and private equity can mean the difference between finding the right financial partner and wasting months on the wrong path.

What Venture Capital Actually Is

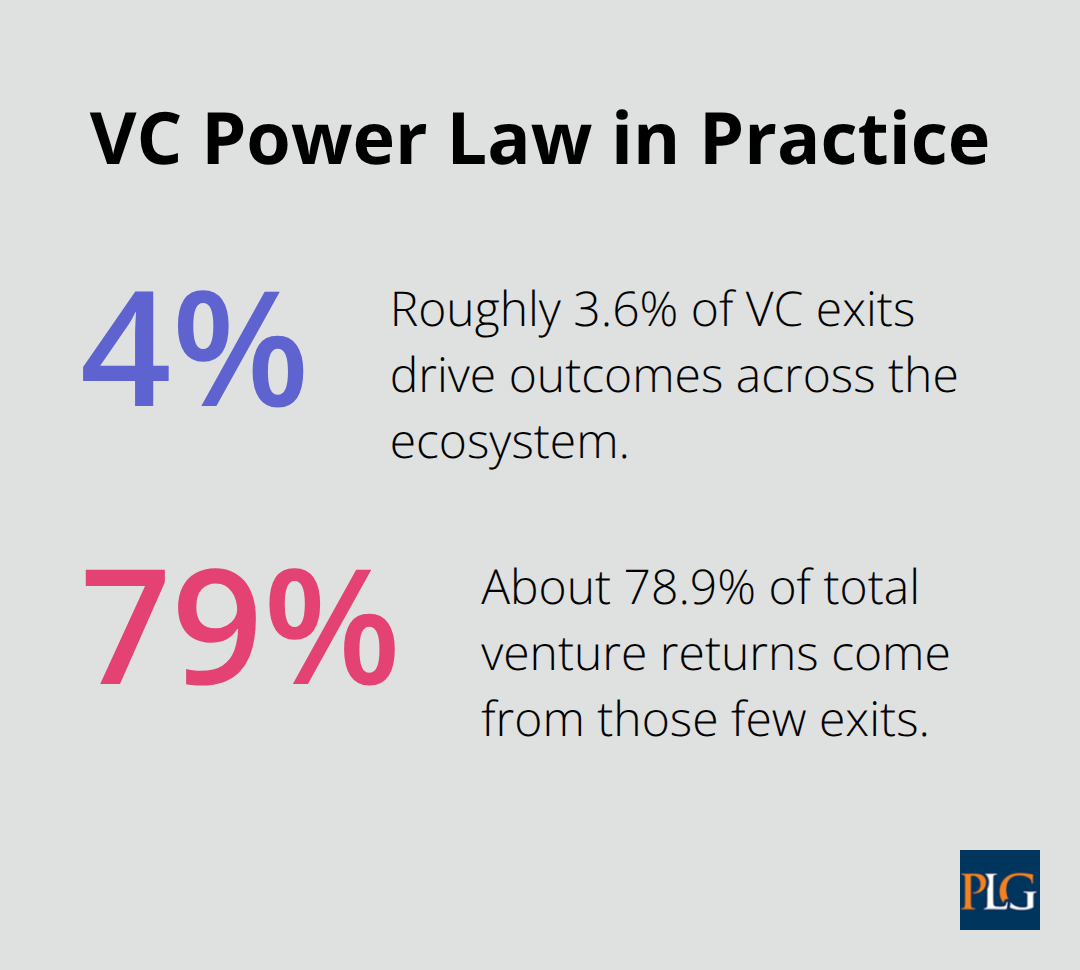

Venture capital funds early-stage companies with unproven business models but massive growth potential. These are the startups that lack predictable cash flows, have not yet turned profitable, and often operate in sectors like software, biotech, or fintech. VC investors accept that many of their bets will fail completely. According to data through 2024, about 3.6% of VC exits produced roughly 78.9% of returns across the entire venture ecosystem. This power law dynamic means VC firms intentionally build portfolios where a single breakout success can offset dozens of failed investments.

The typical Series A round sits under $10 million, though later funding rounds scale significantly higher. VC investors take minority stakes, usually under 25%, which means founders retain meaningful control and upside. The relationship between VC and founder is fundamentally a partnership in building something new from scratch.

Where Venture Capital Comes From

Venture capital pools money from wealthy individuals, pension funds, university endowments, and specialized VC firms. These investors commit capital to a fund that typically has a 10-year lifecycle. The fund manager then sources deals, performs due diligence, invests in companies, and works to generate returns through exits. Funding arrives in stages, not all at once. A startup might raise a seed round of $500k to $2 million, then a Series A of $5 to $15 million, then Series B, C, and beyond as the company scales. Each round introduces new investors, dilutes existing shareholders, and comes with specific milestones the company must hit.

The Value Beyond Capital

VC firms like Sequoia Capital, Andreessen Horowitz, and Benchmark actively participate in board governance and strategy, providing far more than just capital. They offer introductions to customers, help recruit senior talent, and share lessons from portfolio companies. This hands-on involvement is a core value proposition, not a side benefit. The VC firm becomes a strategic partner invested in the company’s trajectory and success.

How Venture Capital Exits and Returns Work

Venture capital exits happen through acquisition or initial public offering. The VC firms that invested in Instagram exited when Facebook acquired the company for $1 billion in 2012, just two years after the Series A. Other exits take seven to ten years. The median VC fund targets a net IRR around 18–25% for early-stage investments, though actual returns vary dramatically by fund and vintage year. Late-stage growth rounds target lower IRRs, typically 18–22%, because the risk profile is lower.

Unlike private equity, which uses debt to amplify returns, venture capital relies purely on equity appreciation. The company’s valuation must increase substantially for investors to achieve their return targets. This means the startup must grow revenue at 100% annually or faster, demonstrate clear product-market fit in a large addressable market, and show a path to profitability or a large exit event. Companies that grow steadily but modestly will never satisfy VC return requirements, which is why venture capital and slower-growth businesses are fundamentally misaligned.

This fundamental mismatch between VC expectations and business reality shapes which companies should pursue venture funding-and which should look elsewhere. Understanding this distinction becomes critical when you evaluate whether private equity might offer a better fit for your capital needs.

What Private Equity Actually Does

Private equity acquires mature, profitable companies and restructures them for value creation over a 4–7 year holding period. Unlike venture capital, which bets on unproven growth, private equity targets businesses already generating consistent cash flows. These companies have established customer bases, predictable revenue streams, and stable margins. PE firms acquire majority control, typically 50% or higher, and often take 100% ownership. The investment sizes dwarf venture capital-North American PE dry powder sits around $1 trillion with assets under management exceeding $3 trillion. A typical PE deal ranges from $25 million to several hundred million dollars.

The Core PE Strategy

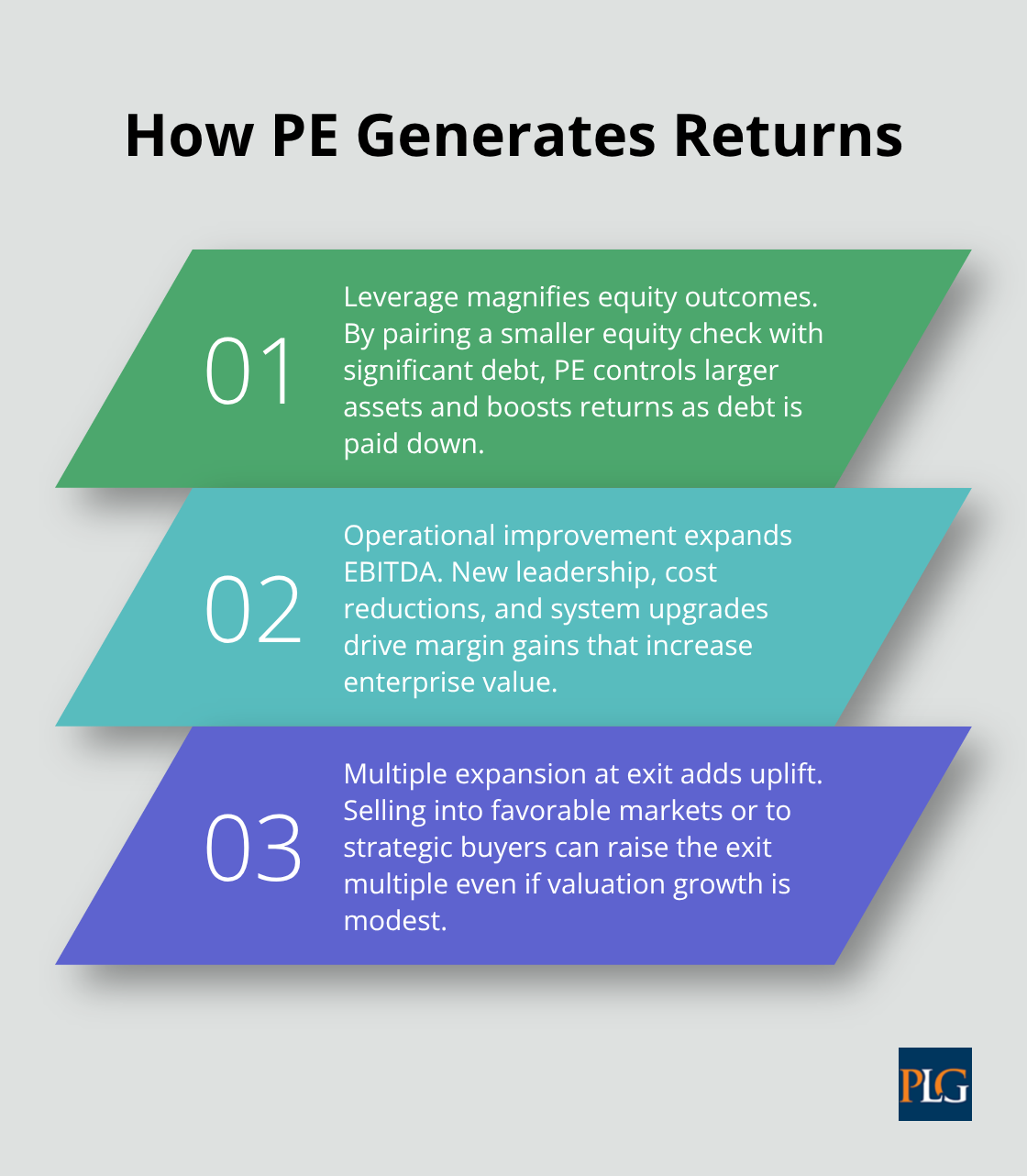

The fundamental difference is this: VC funds growth; PE funds stability and operational improvement. PE firms like Apollo Global Management, Blackstone, and KKR deploy capital across industries including manufacturing, retail, software, and infrastructure. They remain indifferent to sector as long as the company demonstrates strong free cash flow and debt capacity. This is where leverage becomes central to the PE playbook. A PE firm might acquire a company for $100 million using $30 million in equity and $70 million in debt. The company’s cash flows service the debt while PE management works to expand EBITDA margins. At exit, typically through strategic sale or secondary market divestiture, the combination of debt paydown and multiple expansion generates returns.

Target net IRRs for PE buyouts sit around 15–20%, lower than early-stage VC but achieved through a fundamentally different mechanism.

How Leverage Powers PE Returns

Debt is the engine that separates PE from every other investment strategy. Lenders typically require a minimum 25% equity contribution, meaning PE firms control deals with far less capital than the purchase price suggests. This leverage amplifies returns when operations improve but creates real downside risk if cash flows deteriorate. A company facing declining revenue must still service debt obligations, which is why PE targets non-cyclical businesses with contracted revenue or predictable demand.

The operational focus distinguishes PE from growth equity or late-stage venture capital. PE firms install new management teams, implement cost reduction programs, upgrade IT systems, and pursue add-on acquisitions to build platform companies. Vista Equity Partners, one of the largest PE firms, has built a portfolio leveraging software contracts that provide cash-flow priority relative to debt service, illustrating how recurring revenue streams unlock leverage capacity.

PE Involvement and Operational Control

PE involvement is deep and hands-on. Unlike VC board participation, PE typically holds majority board seats and direct operational control. This isn’t advisory partnership-it’s active management aimed at specific EBITDA targets and margin improvements. The metrics differ significantly from venture capital. VC measures product-market fit and revenue growth rates exceeding 100% annually. PE measures EBITDA multiples, free cash flow conversion, and debt service coverage ratios. A company growing 5% annually with 40% EBITDA margins represents a PE home run. The same company would never attract serious venture capital attention.

This fundamental misalignment between PE and VC investment criteria means the right funding source depends entirely on your company’s maturity stage and financial profile. A profitable business with stable cash flows will struggle to satisfy VC return requirements but will thrive under PE ownership. Understanding which category your company falls into determines whether you should pursue private equity or look toward venture capital instead.

Where the Money Comes From and Where It Goes

VC Funding Arrives in Stages, PE Deploys Capital Upfront

Venture capital arrives in tranches tied to specific milestones, not as a lump sum. A startup raising Series A receives $8 million upfront, then another $2 million when it hits user growth targets six months later. This staged approach protects investors by validating progress before deploying additional capital. Private equity operates differently-PE firms deploy the full acquisition price on day one. A PE firm acquiring a $100 million company transfers the entire purchase price at closing, funded through a combination of equity and debt.

The timeline difference matters enormously. VC rounds typically close within 90 days of final term sheet, while PE transactions often take six to twelve months from initial contact to closing due to debt financing, regulatory approvals, and operational due diligence.

Investment Size Reveals Company Maturity

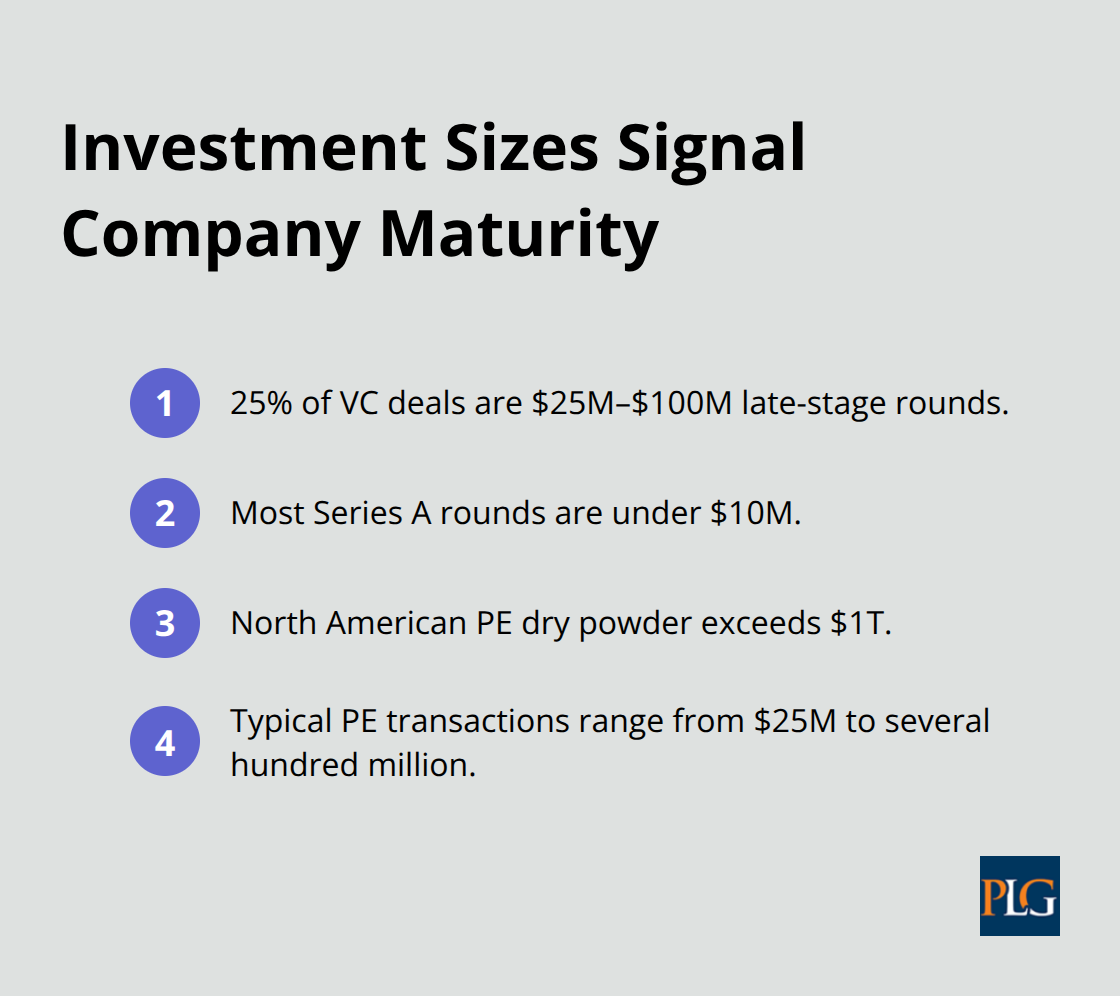

Investment sizes tell the real story about company maturity. According to PitchBook data, approximately 25% of VC deals fall in the $25 million to $100 million range, representing late-stage growth rounds. Most Series A rounds stay well under $10 million because early-stage companies lack the revenue base to justify larger checks.

PE deals dwarf these numbers, with North American PE dry powder exceeding $1 trillion and typical transactions ranging from $25 million to several hundred million dollars.

A company generating $2 million in annual revenue will never attract PE interest, but that same company might raise a $5 million Series A. Conversely, a company with $20 million in stable EBITDA will never satisfy VC return requirements but represents an ideal PE acquisition target.

Exit Timing and Return Mechanisms Differ Fundamentally

Venture capital expects exits within seven to ten years, with some exits occurring in two to three years when acquisition offers arrive. According to Cambridge Associates data through the end of 2023, early-stage VC achieved IRRs around 18.28%, while late-stage growth rounds targeted 18–22% returns. These returns depend entirely on massive valuation increases, which means the company must either go public or get acquired at a much higher valuation than the VC’s entry price.

Private equity targets 4–7 year holding periods with net IRRs around 15–20%, achieved through a fundamentally different mechanism. PE returns come from three sources: debt paydown, operational EBITDA improvement, and multiple expansion at exit. A PE firm might acquire a company at an 8x EBITDA multiple, improve operations to grow EBITDA by 25%, then exit at a 9x multiple. That combination generates substantial returns even if the absolute company valuation stays flat.

Risk Profiles and Performance Metrics Diverge Sharply

VC accepts that many portfolio companies will fail completely, relying on the power law where roughly 3.6% of exits produce 78.9% of total returns across the entire venture ecosystem according to 2024 data. This means VC investors expect and plan for failure across most of their portfolio. PE firms, by contrast, use leverage and control to minimize failure rates. A PE-backed company facing declining revenue must still service debt obligations, which creates real downside risk if operations deteriorate. This is why PE targets non-cyclical businesses with contracted revenue or predictable demand, while VC accepts companies with entirely unproven business models.

The metrics used to evaluate performance differ just as sharply. VC measures product-market fit, annual revenue growth exceeding 100%, and the size of the addressable market. PE measures EBITDA multiples, free cash flow conversion, debt service coverage ratios, and margin improvement. A company growing 5% annually with 40% EBITDA margins represents a PE success story but would never attract VC attention.

Final Thoughts

The choice between venture capital and private equity hinges on your company’s financial maturity and growth trajectory. Venture capital funds unproven businesses betting on explosive growth, while private equity acquires stable, cash-generating companies and restructures them for operational improvement. These are not interchangeable funding sources, and pursuing the wrong one wastes months of your time and energy.

If your company generates minimal revenue, lacks profitability, and operates in a high-growth sector, venture capital is your path. VC investors expect to lose money on most bets but accept that risk because a few massive wins offset the failures. Your job is to demonstrate product-market fit, show that you can grow revenue at 100% annually or faster, and prove that your addressable market is large enough to justify VC return requirements.

If your company already generates consistent cash flows, maintains stable margins, and operates in a non-cyclical market, private equity represents a fundamentally different opportunity. PE firms acquire controlling stakes and deploy operational expertise to expand EBITDA and improve margins. They use leverage to amplify returns, which means your company must demonstrate the cash flow stability to service debt. The venture capital private equity distinction matters because misalignment between your company and your funding source creates friction that derails negotiations and wastes resources. We at Primum Law Group help founders and business owners navigate this decision by analyzing your company’s financial profile, growth stage, and capital needs, then structure the transaction to align your interests with the right investor class through our transaction services.