San Francisco startups raised $63.2 billion in venture capital during 2023, making funding stage navigation more competitive than ever.

We at Primum Law Group see founders struggle with venture capital stages daily. Understanding each funding round’s legal requirements can make or break your startup’s growth trajectory.

This guide breaks down every stage from pre-seed to exit, covering documentation needs and common legal pitfalls that derail deals.

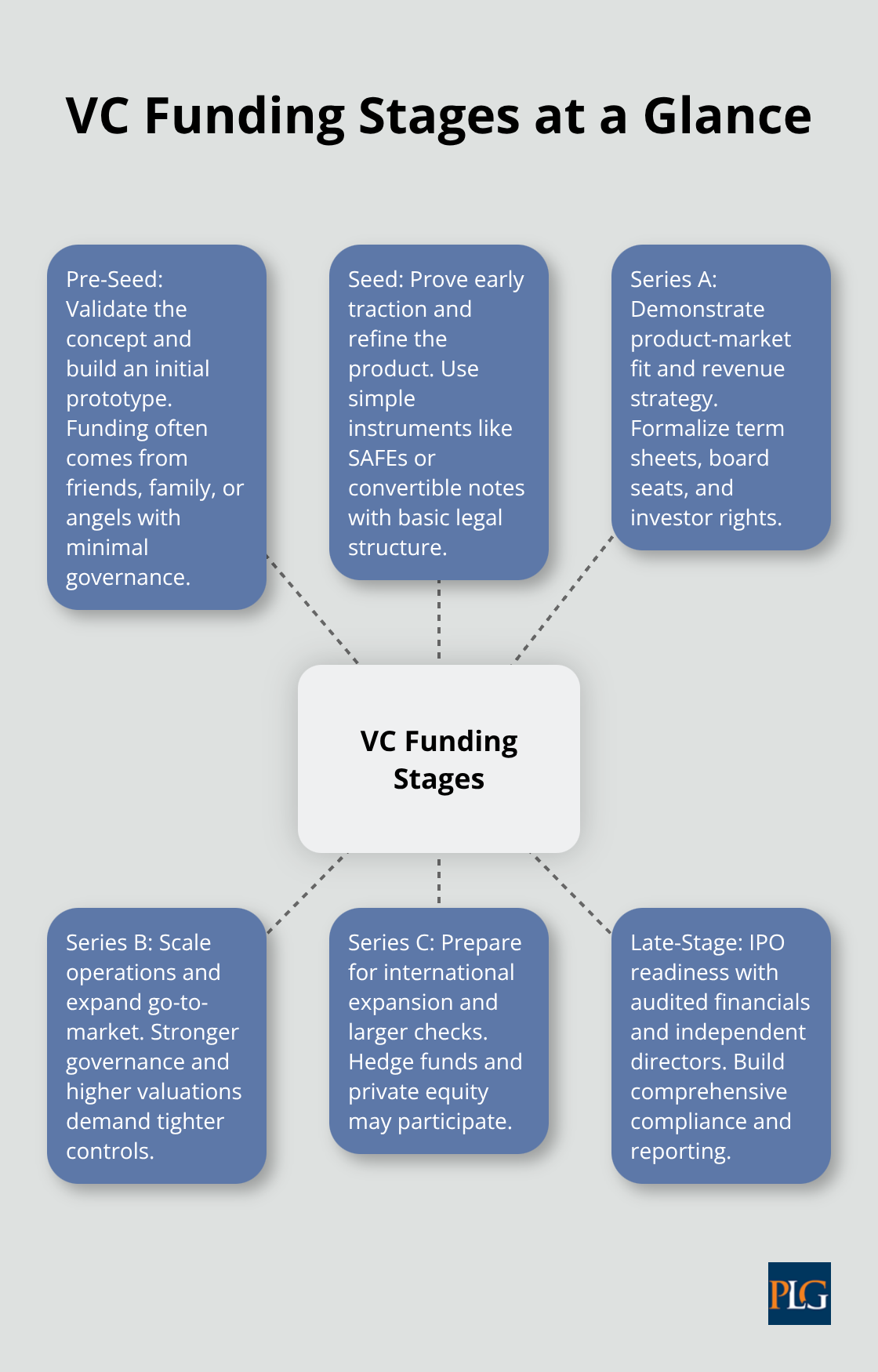

What Defines Each VC Funding Stage

Pre-Seed and Seed Rounds Set the Foundation

Pre-seed funding typically ranges from $100,000 to $5 million and focuses on business concept validation. Founders often raise these amounts from friends, family, or angel investors without formal board structures. Seed rounds follow with $500,000 to $2 million investments and require basic legal documentation like convertible notes or SAFE agreements.

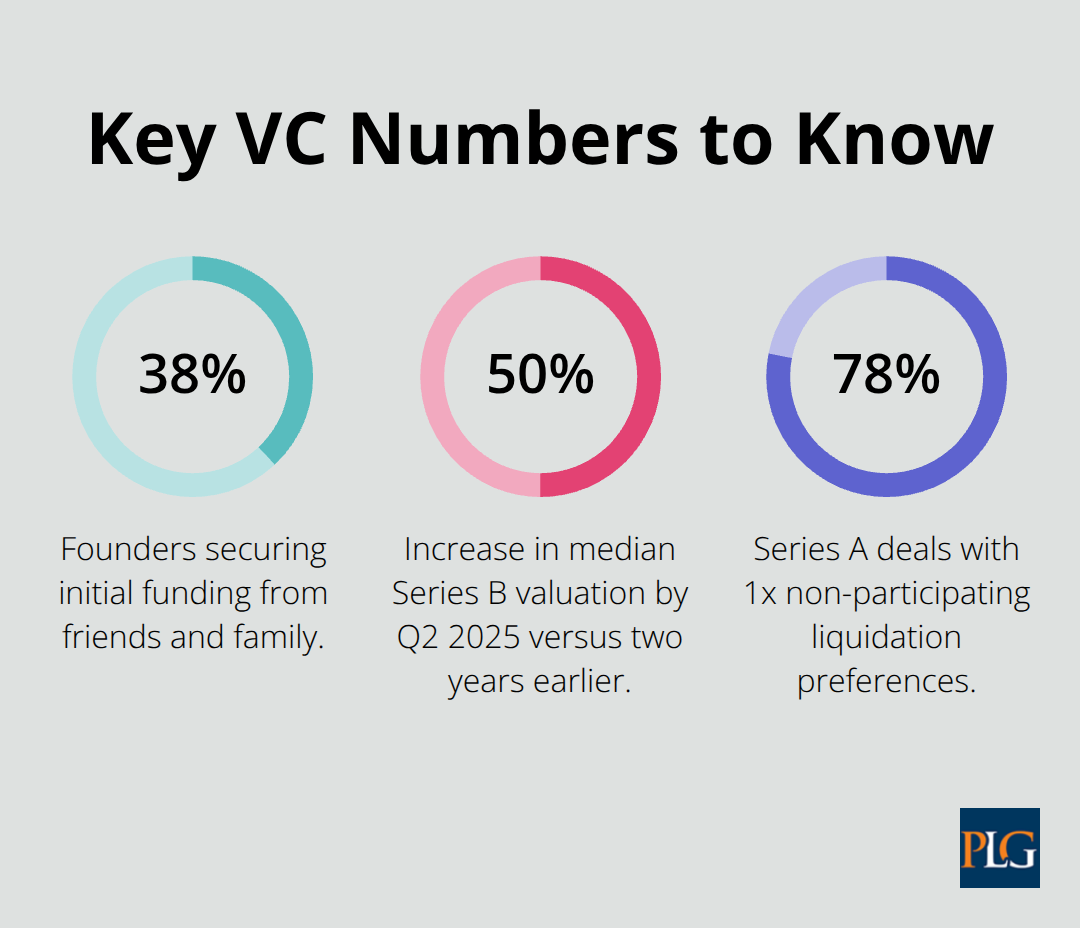

Fundable reports that 38% of startup founders secure initial funding from friends and family. The median time between seed and Series A rounds spans 12 to 18 months, which makes early legal preparation essential for future success. Most pre-seed companies operate with minimal governance structures and simple equity arrangements.

Series A Through C Rounds Demand Formal Structure

Series A funding averages $19.3 million in 2025 and requires comprehensive legal frameworks that include term sheets, board composition agreements, and investor rights provisions. Companies must demonstrate product-market fit and clear revenue strategies to attract venture capital firms like Sequoia Capital.

Series B rounds reached a median valuation of $120 million in Q2 2025 (a 50% increase from two years earlier according to Carta). Series C funding often exceeds $30 million and attracts hedge funds and private equity firms that seek established businesses ready for international expansion. Each round increases investor involvement and board oversight, which fundamentally changes your company’s governance structure.

Late-Stage Capital Prepares for Public Markets

Late-stage funding rounds serve as bridges to IPOs, with companies that raise tens or hundreds of millions for global expansion and acquisitions. These rounds require audited financial statements, formal board structures with independent directors, and comprehensive compliance frameworks.

Investment banks and institutional investors dominate this stage and expect detailed exit strategies plus proven scalability models before they commit capital. The legal complexity at this stage often requires specialized counsel to navigate securities regulations and prepare for eventual public market requirements.

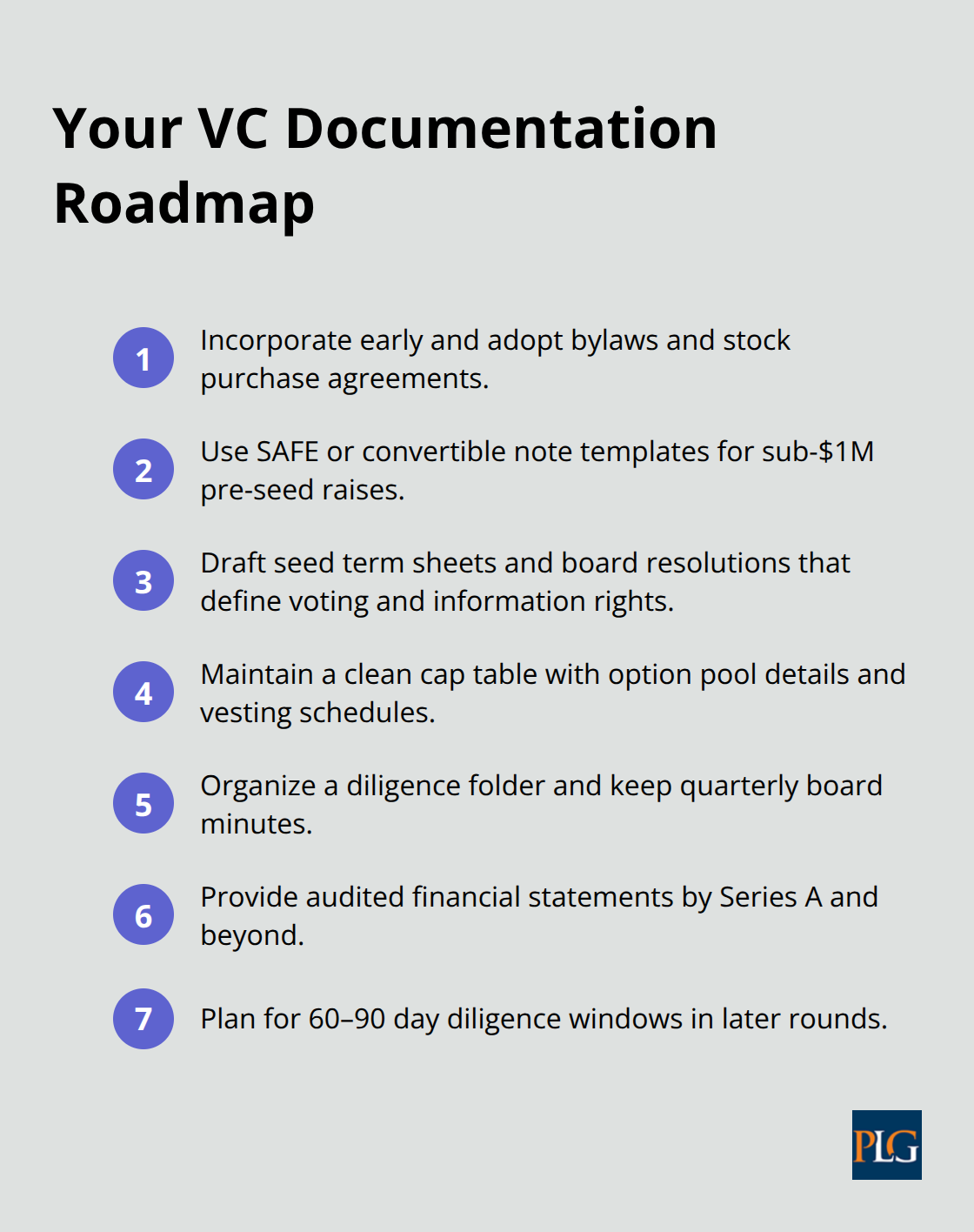

What Documentation Do You Need for Each Funding Stage

Pre-Seed and Seed Round Essentials

Pre-seed rounds operate with minimal paperwork but still demand foundational legal structures. Simple convertible notes or SAFE agreements suffice for amounts under $1 million, though we recommend you establish basic bylaws and stock purchase agreements from day one.

Seed rounds require formal term sheets, board resolutions, and investor rights agreements that define voting powers and information rights. Companies that raise seed funding must prepare capitalization tables and basic financial statements that demonstrate burn rate and runway calculations.

Series A Documentation Expands Significantly

Series A rounds demand extensive legal preparation that includes detailed term sheets with liquidation preferences, anti-dilution provisions, and board composition requirements. Stock purchase agreements expand to 40-50 pages and cover drag-along rights, tag-along provisions, and transfer restrictions.

Investors expect audited financial statements, comprehensive due diligence materials, and formal board meeting minutes from previous quarters. Valuation methods shift from revenue multiples to discounted cash flow models (with investors requiring detailed financial projections that span three to five years).

Advanced Rounds Multiply Complexity

Due diligence timelines extend to 60-90 days and include legal, financial, and technical reviews that investor teams conduct. Series B and C rounds multiply these requirements with additional regulatory filings, enhanced governance structures, and sophisticated voting agreements.

These later-stage documents can exceed 100 pages in complexity and require specialized legal counsel to navigate securities regulations properly. The documentation burden increases exponentially as companies approach public market readiness (making early legal foundation work even more valuable).

The complexity of these legal requirements directly impacts how you value your company and negotiate with investors.

Common Legal Challenges in VC Transactions

Term Sheet Negotiations Create Deal Breakers

Term sheet negotiations reveal the biggest disconnect between founder expectations and investor demands. Liquidation preferences rank as the most contentious provision, with 78% of Series A deals including 1x non-participating preferences that protect investor downside while they limit founder upside. Anti-dilution provisions create another battleground where weighted average formulas favor investors during down rounds and potentially wipe out founder equity in companies that struggle.

Board composition negotiations often stall deals when founders resist control transfers, yet investors typically demand at least one board seat in Series A rounds and majority control in Series B transactions. Voting thresholds for major decisions like acquisitions or additional rounds require careful structure to prevent deadlock situations that freeze company operations entirely.

Investor Rights Impose Operational Burdens

Information rights provisions force startups into quarterly cycles that consume significant management time and legal costs. Tag-along and drag-along rights become problematic when founders want to sell personal shares or when majority investors push for exits that minority stakeholders oppose. Right of first refusal clauses on employee stock transfers can delay key decisions and complicate equity compensation plans.

Pro rata rights allow investors to maintain ownership percentages in future rounds, but these provisions can block new investor participation and limit options during difficult periods (especially when companies face down rounds or extended timelines).

Exit Strategy Complications Surface Late

IPO readiness demands three years of audited financial statements and formal governance structures that most startups lack until Series C rounds. Acquisition negotiations frequently fail due to poorly structured employee option pools and schedules that create retention issues during due diligence periods.

Delaware incorporation becomes essential for serious exit plans, as 89% of IPOs and major acquisitions involve Delaware corporations due to established legal precedents and investor familiarity. Tag-along rights complicate acquisition timing when minority shareholders can force inclusion in sale processes (potentially derailing deals with strategic buyers who prefer clean cap tables).

Protecting your ownership requires understanding these legal complexities and securing experienced legal expertise throughout the funding process.

Final Thoughts

Venture capital stages demand strategic preparation and solid legal foundations from your first investor conversation. Companies that build proper structures during pre-seed rounds face smoother Series A negotiations and avoid expensive restructuring costs later. Documentation requirements multiply with each round, which makes early investment in quality legal counsel a competitive advantage.

San Francisco startups compete for $63.2 billion in annual venture capital funding. Your legal strategy affects valuation negotiations, board composition, and exit opportunities directly. Poor preparation during early rounds creates compounding problems that can destroy promising companies entirely.

We at Primum Law Group help startups navigate these complexities through experienced legal guidance that covers venture capital transactions and corporate governance. Our team provides cost-effective strategies that scale with your growth trajectory. Build your legal foundation now rather than scramble during due diligence when investors demand perfect documentation immediately.