Investors scrutinize startups during due diligence to assess financial health, team capability, and market position. Most founders underestimate how thoroughly investors examine documents, legal structures, and historical records.

We at Primum Law Group help startups prepare for this process by organizing materials and addressing vulnerabilities before investors arrive. Getting your due diligence preparation right separates deals that close from those that stall.

What Investors Actually Scrutinize

Investors don’t just glance at your numbers and move on. They conduct a systematic financial autopsy that reveals whether your business can survive and scale.

Financial Performance and Unit Economics

Investors want to see 24 months of revenue history with gross margin trends, clean unit economics, and honest cash flow projections under best, base, and worst-case scenarios. For SaaS companies specifically, investors expect gross margins between 70 and 85 percent, Net Dollar Retention above 120 percent, Customer Acquisition Cost payback within 16 months, and a Lifetime Value to CAC ratio of at least 3 to 1.

If your financials show declining margins, rising churn, or unit economics that don’t work, you’ll lose credibility before the conversation even starts. Present your financials in both CAD and USD if you operate across borders. Vague projections or numbers that don’t connect to real customer data will trigger skepticism.

Cap Table and Ownership Structure

Investors examine your cap table with surgical precision to understand founder ownership, option pool allocation, and prior investor terms like anti-dilution clauses and participation rights. A messy cap table with too many small investors or an undersized option pool signals poor planning and future dilution problems.

Team Execution and Leadership

Investors bet on people, not just ideas. They look for founders and leadership who have shipped products, acquired customers, or scaled operations before. This doesn’t mean you need a Fortune 500 resume, but you need concrete evidence of execution: Did you launch a previous company? Did you grow a team from five to fifty people? Did you close enterprise deals?

Investors want to see that your team understands the problem you’re solving because you’ve lived it. They also assess whether your board composition is credible and whether insiders and institutional owners are aligned on the same exit timeline. Weak leadership signals translate into deal hesitation faster than almost anything else.

Market Position and Competitive Advantage

Your competitive position determines whether your market opportunity is real or imaginary. Investors expect you to define your addressable market with credible TAM, SAM, and SOM estimates and benchmark yourself against two or three relevant competitors. They want to know why customers choose you over alternatives and whether switching costs exist that reduce churn.

If you claim a massive market but can’t articulate how you’ll capture a meaningful slice, investors will see through it. Demonstrate product viability with customer testimonials, written case studies, pilot programs, and measurable retention rates. Third-party satisfaction scores and high renewal rates prove your solution solves a real problem. Without this traction evidence, investors assume your product-market fit is theoretical, which brings us to the next critical phase: organizing your materials so investors can verify every claim you make.

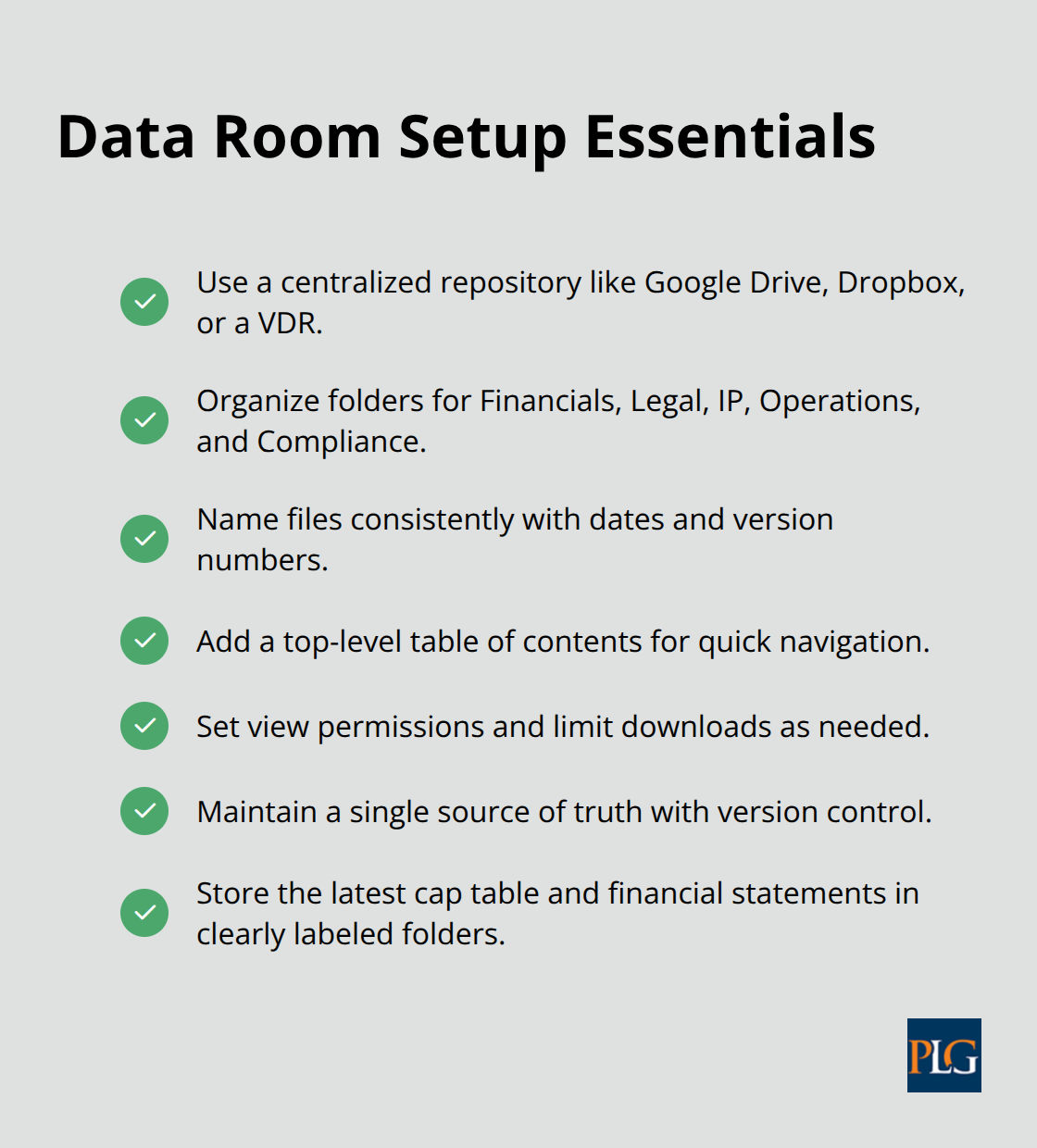

Organize Your Data Room for Investor Review

Investors expect to find what they need in minutes, not days. A disorganized data room signals sloppy operations and hidden problems. We have seen deals stall or collapse because founders buried critical documents in email threads or stored them across five different platforms. Investors lose patience quickly, and a chaotic data room becomes the first red flag that stops momentum.

Start with a centralized digital repository using Google Drive, Dropbox, or a dedicated virtual data room platform. Structure it into clear folders: Financials, Legal, Intellectual Property, Operations, and Compliance. Name files consistently and descriptively-use dates and version numbers so investors know they’re seeing the latest cap table or financial statements.

Include a table of contents at the top level that maps each folder and its contents. This single document saves investors hours and demonstrates that you respect their time.

Financial Statements and Cash Flow Projections

Compile three to six months of audited or internally prepared financial statements alongside corresponding tax returns. Include monthly revenue reports, gross margin calculations, and customer acquisition costs for the past 24 months. Investors cross-reference these numbers obsessively. A gap between what your pitch deck claims and what your general ledger shows will kill trust immediately.

Provide cash flow projections under best, base, and worst-case scenarios with transparent assumptions about growth rates, churn, and expansion revenue. Label your assumptions clearly so investors understand what drives each scenario. Include a monthly cash burn calculation and runway projection-this tells investors how much runway you have and when you’ll need capital again. If you operate across borders, present everything in both CAD and USD using consistent conversion dates and rates. Vague numbers or unexplained variances between months signal that your accounting practices are weak or your financial controls don’t exist.

Cap Table, Governance, and Ownership Documentation

Gather your Articles of Incorporation, Bylaws, Shareholder Agreements, Board Resolutions, and meeting minutes dating back to your founding. Investors verify that your company is properly incorporated in Delaware or another founder-friendly jurisdiction and that all governance records remain accurate.

Create a clean, current cap table showing founder ownership, employee option pool allocation, and all prior investor stakes. Include vesting schedules, strike prices, and any anti-dilution or participation rights from previous rounds. A messy cap table with too many small seed investors or an undersized option pool (try for roughly 20 percent of total capitalization) signals poor planning and raises dilution concerns. Document all 83(b) elections filed within 30 days of option grants-investors want proof that tax complications were managed correctly from the start. Include a cap table sensitivity analysis that models dilution under different valuation scenarios so investors see how their ownership will shift if future rounds price higher or lower than expected.

Intellectual Property Ownership and Product Traction

List all patents, trademarks, copyrights, and trade secrets your company owns or licenses. Include patent application numbers, filing dates, and jurisdiction coverage. Document IP assignments from all founders, employees, and contractors to prove your company owns what it claims to own. Many deals have stalled because IP ownership was unclear or an employee retained rights to core technology. Add domain registrations, software licenses, and open-source component compliance documentation.

Include customer testimonials, case studies, and pilot program results that demonstrate product viability and traction. Organize contracts separately: customer agreements, supplier agreements, employment agreements, leases, and loan documents. Investors scrutinize customer contracts to understand revenue recognition, payment terms, and whether customers can cancel on short notice. A high-churn customer base or unfavorable payment terms will concern investors about your growth sustainability. These documents form the foundation of what investors examine next-the red flags that can derail even well-funded startups.

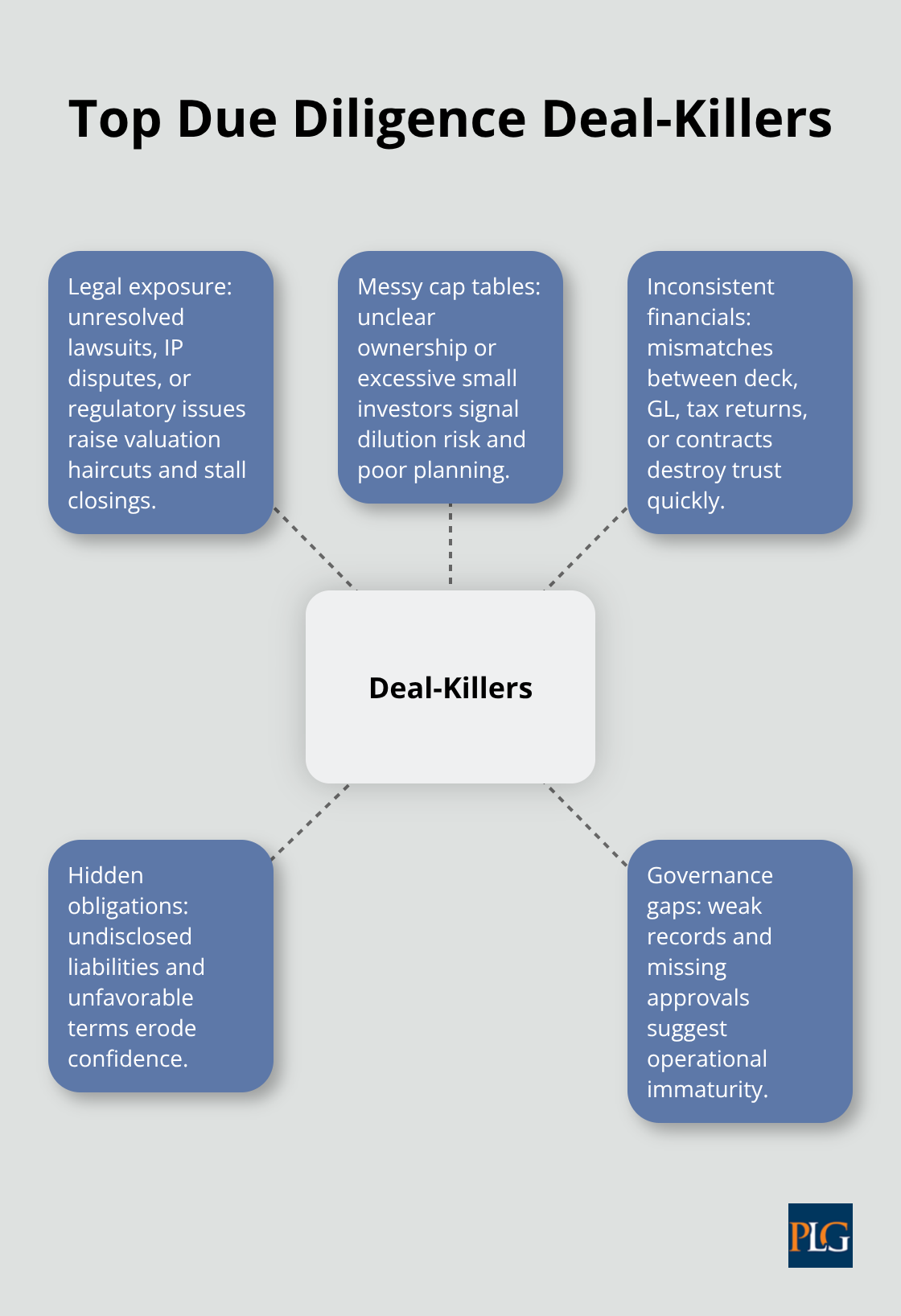

What Kills Deals in Due Diligence

Nearly half of all venture deals collapse during due diligence, according to research from Baker McKenzie and partner reports tracking M&A outcomes. The culprit isn’t always a bad business model or weak market fit. Often it’s preventable mistakes that compound into deal-killers: unresolved lawsuits that create financial liability, cap tables so tangled that ownership becomes unclear, or financial statements that don’t match your tax returns. Investors tolerate ambition and market risk, but they won’t tolerate governance gaps or hidden obligations.

A single outstanding lawsuit without a resolution plan, an unsigned IP assignment from a co-founder, or six months of unexplained variance between your accounting records and your pitch deck will stop momentum faster than almost anything else. The pattern matters more than the size of each individual problem. Investors interpret a collection of small governance failures as a proxy for how your leadership team operates at scale. If you can’t manage basic corporate hygiene now, how will you handle compliance when you process thousands of transactions monthly or manage enterprise customers with strict security requirements?

Unresolved Legal Exposure That Compounds Risk

List every active or dormant legal issue your company faces: pending lawsuits, regulatory investigations, intellectual property disputes, expired licenses, or unpaid tax liabilities. Each one creates quantifiable risk that investors must account for in their valuation and deal structure. A lawsuit that sits unresolved for eighteen months signals either that your legal team dropped the ball or that settlement costs are so high you’re avoiding them. Either interpretation damages investor confidence. If you have a trademark dispute, a patent challenge from a competitor, or a former employee claiming IP ownership of your core technology, these aren’t minor details to disclose in passing. They’re deal-critical issues that require a concrete remediation plan with timelines and estimated costs.

Run a pre-diligence internal audit six to nine months before you expect investor meetings. Identify every unresolved legal matter, quantify its potential cost, and outline how you’ll resolve it. Close out old regulatory issues, renew expired licenses, and settle minor disputes before investors arrive. Transparency about known problems paired with a credible action plan builds trust. Silence about legal exposure until diligence starts destroys it.

Equity Structure and Ownership Clarity

Your cap table must tell a clear story about who owns what and why. Investors expect to see founder equity, employee option pool allocation (ideally around 20 percent of total capitalization), and prior investor stakes with their terms spelled out. If your cap table has twenty small seed investors from a crowdfunding round, a co-founder whose vesting status is ambiguous, or option grants where strike prices don’t align with your latest 409A valuation, you’ve created unnecessary friction. Investors will demand clarity before they commit capital, which means your legal team will scramble to reconstruct documents under time pressure. That scramble costs time and money and signals poor corporate housekeeping.

Document all 83(b) elections with filing dates to prove you managed tax implications correctly from the start. Include vesting schedules and anti-dilution language from prior rounds so investors understand what they’re inheriting. A clean cap table with founder vesting on a standard four-year schedule with a one-year cliff, a reasonable option pool, and prior investor terms that are documented and accessible will speed diligence substantially.

Financial Records That Tell Consistent Stories

Investors cross-reference your pitch deck against your general ledger, your tax returns, your bank statements, and your customer contracts. A variance between claimed revenue and reported revenue, a gap between your stated gross margin and what your accounting records show, or inconsistency in how you recognize revenue across different customer contracts will trigger deeper scrutiny and skepticism. If your financials show a spike in revenue one month followed by a sharp drop the next, investors want to understand why. Was it a one-time deal? A customer cancellation? A timing issue in how you recognize revenue? Vague explanations or missing documentation around large transactions will make investors question whether your accounting practices meet basic standards.

Implement cloud-based accounting systems, reconcile your accounts monthly, and maintain clear revenue recognition policies that align with GAAP or IFRS standards depending on your structure. Document your accounting assumptions and keep them consistent across all financial statements you present to investors. If you’ve been using spreadsheets and manual processes to track revenue, migrate to a proper accounting platform before diligence starts. The investment in time and software pays dividends in credibility and speed during investor review.

Final Thoughts

Due diligence readiness requires continuous attention, not last-minute scrambling. The startups that close funding fastest maintain organized financial records, current cap tables, and centralized data rooms at all times. When investors request materials, you hand them a complete package within hours-that speed signals operational maturity and builds confidence immediately.

The red flags outlined throughout this post-unresolved legal issues, murky equity structures, and inconsistent financial records-are entirely preventable. Run an internal audit six to nine months before you plan to fundraise, identify gaps in governance and documentation, and close out old legal matters. This proactive approach costs far less than fixing problems under investor pressure, and it positions your startup to move faster through due diligence.

We at Primum Law Group help startups build the legal and financial foundations that make due diligence straightforward. From structuring your cap table and documenting IP ownership to organizing your data room, we support your fundraising readiness at every stage. Contact our team to discuss how we can help you prepare for investor conversations and strengthen your due diligence startup position.