Venture capital funds are the financial engines behind many of the world’s most successful startups. Understanding how a venture capital fund works is essential if you’re raising money or building a business in today’s competitive landscape.

At Primum Law Group, we’ve guided countless founders through VC funding rounds. This guide breaks down the mechanics of how these funds operate, from capital raising to exits.

How VC Funds Raise and Structure Capital

The Fund Lifecycle and Capital Commitments

Venture capital funds operate as pooled investment vehicles, and understanding their capital structure reveals why so few startups actually receive funding. A typical VC fund closes with a committed capital target-say $100 million to $500 million for mid-stage funds in San Francisco-and GPs (general partners) spend 6 to 12 months convincing institutional investors to commit. These LPs (limited partners) include pension funds, university endowments, insurance companies, and family offices. Sequoia and Andreessen Horowitz, two of the largest San Francisco-based firms, manage billions across multiple funds, but even established firms face intense pressure to deploy capital within defined investment periods.

Most VC funds operate on a 10-year life: a 3 to 5-year investment period where the GP actively writes checks, followed by 5 to 7 years of portfolio management and exits. This timeline matters because it forces discipline. A GP cannot hold capital indefinitely; if they miss their investment window, returns suffer and LPs withhold capital from future funds.

How Fund Size Shapes Investment Strategy

Fund size determines check size, which determines which startups a fund can realistically back. A $50 million fund might write $500k to $2 million checks, while a $300 million fund writes $3 million to $10 million initial checks. This explains why emerging managers struggle to fund seed-stage companies-their funds are too small to make meaningful bets at scale.

Capital commitments from LPs come with strict terms that fundamentally shape fund behavior. An LP committing $10 million to a fund does not hand over cash upfront; instead, they sign a limited partnership agreement pledging capital that the GP calls down over time, typically in tranches as deployment accelerates. This mechanism protects LPs from overpaying fees on dry powder but creates cash flow complexity for GPs.

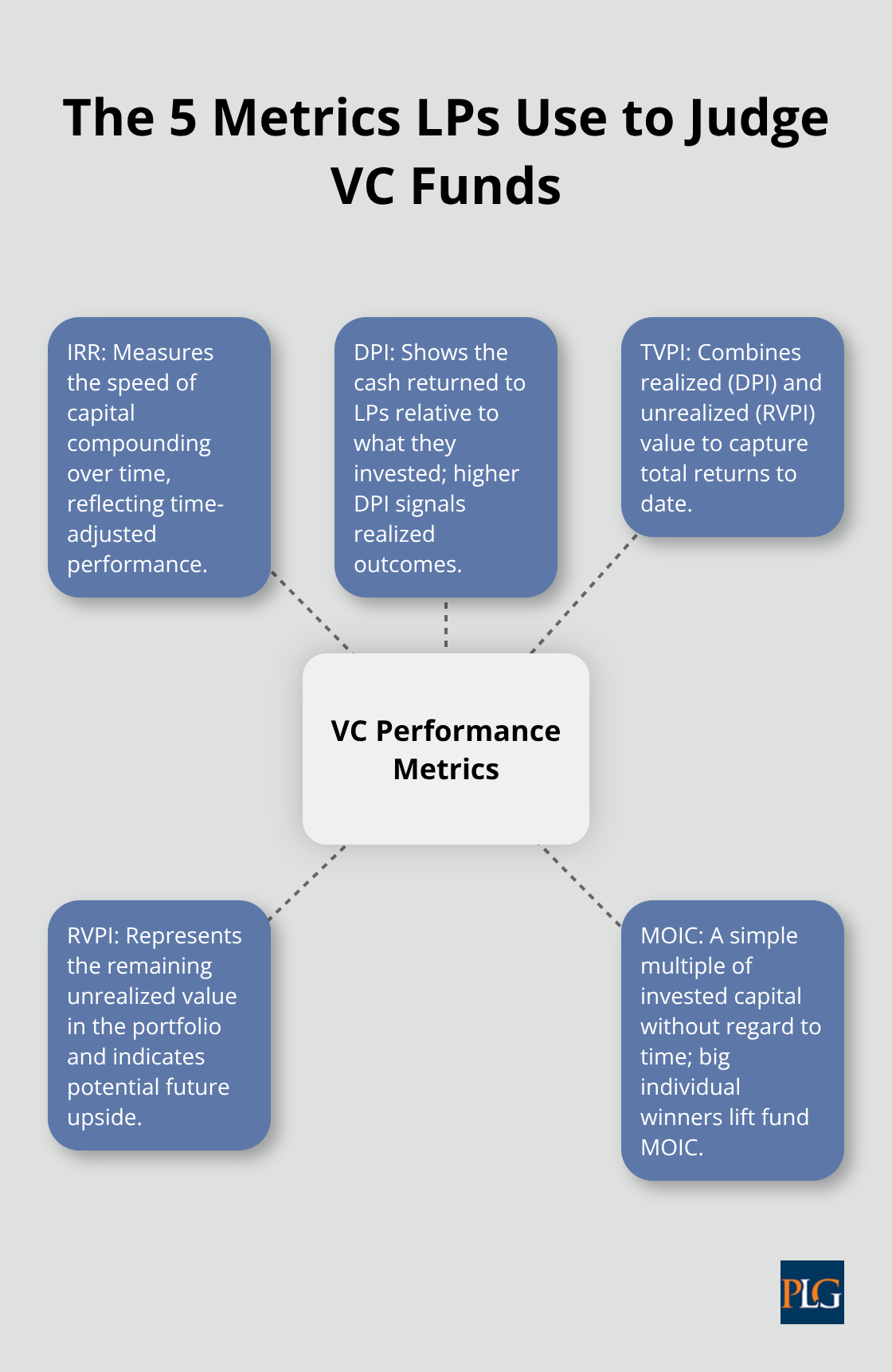

Performance Metrics That Drive LP Decisions

LPs evaluate fund performance using five interconnected metrics: IRR (Internal Rate of Return), DPI (Distributions to Paid-In capital), TVPI (Total Value to Paid-In), RVPI (Residual Value to Paid-In), and MOIC (Multiple on Invested Capital). A strong fund targets net IRR above 20%, DPI greater than 1.5× (meaning they return more cash than invested), and TVPI around 2.0× or higher. These benchmarks drive LP behavior; if a fund underperforms, LPs cut capital from the next fund and shift to competitors.

San Francisco’s dominant firms like Menlo Ventures and Bessemer Venture Partners maintain institutional memory and track records that attract repeat LP capital, while new funds face extreme skepticism.

The Trade-Off Between Fund Size and Performance

Fund size itself creates tension. Larger funds ($300 million and above) write bigger checks and support portfolio companies longer, but they sacrifice agility and struggle with smaller early-stage rounds. Smaller funds ($50 million to $150 million) move faster and build deeper founder relationships, but they lack the capital to lead Series B and Series C rounds, forcing exits or dilution of existing positions.

A 2023 analysis showed that mid-sized funds ($100 million to $300 million) often outperform both mega-funds and micro-funds on IRR, though mega-funds capture more absolute dollars and media attention. This performance variation reflects a fundamental reality: the best fund size depends on the stage and sector a GP targets. Once a fund closes and LPs commit capital, the GP faces the next challenge-actually finding and evaluating startups worth backing.

Finding and Evaluating Startup Opportunities

Deal Sourcing in San Francisco’s Competitive Market

Venture capital funds generate returns only if they identify startups before competitors do. In San Francisco, where over $63 billion flowed into Bay Area startups in 2023, deal sourcing separates winners from mediocre performers. GPs source deals through founder referrals, accelerator demo days, existing portfolio company networks, and cold inbound pitches.

Y Combinator’s Demo Day alone attracts 1,000+ investors annually and surfaces hundreds of pre-Series A companies; founders who graduate from YC report dramatically faster fundraising timelines because Demo Day creates competitive tension among investors.

Most VC firms receive 5,000 to 10,000 inbound pitches annually and fund fewer than 50 companies. This brutal conversion rate forces GPs to develop repeatable evaluation frameworks. Strong teams look for founders with prior operating experience, a clear market wedge rather than vague positioning, and early traction that proves demand exists.

Identifying Real Traction Before Series A

A startup showing $100k monthly recurring revenue before Series A fundraising signals real product-market fit; those without measurable traction face skepticism regardless of the team’s pedigree. San Francisco firms like Menlo Ventures and First Round Capital prioritize founders who articulate their unfair advantage in 60 seconds and back claims with data. Investors explicitly reject founders who rely on hype over metrics.

Unit economics matter equally. For SaaS companies, a 3-to-1 LTV-to-CAC ratio signals healthy growth, while monthly churn under 5% indicates product stability. Net revenue retention above 100% means existing customers expand spending-a powerful indicator of market fit that separates strong performers from struggling ones.

Due Diligence: The 40-to-60-Hour Reality Check

Due diligence happens after a GP decides a startup fits their thesis, and this phase separates serious investors from window-shoppers. A typical Series A due diligence process takes 40 to 60 hours and examines cap tables for clarity, IP assignments for completeness, and financial statements for accuracy. Revenue recognition must follow ASC 606 standards; customer contracts exceeding $100,000 warrant legal review because they reveal concentration risk.

Founders working with experienced legal counsel-such as Primum Law Group, which provides venture capital transaction services to startups and investors in San Francisco and Silicon Valley-navigate this phase more efficiently and protect their interests during negotiations.

Portfolio Management Begins Immediately After Investment

Once due diligence closes, portfolio management begins immediately. Early-stage companies need board support, not just capital: founders report that investor help with capital raises, culture development, and strategic partnerships drives outcomes as much as the initial check. Structure Capital, a San Francisco-based fund managing 91 portfolio companies across 53 countries, emphasizes this through programs like BrandCamp, where portfolio founders receive hands-on branding support from creative agencies.

This value-add mentality separates funds that compound returns from those that merely write checks and hope. The firms that build deep operational relationships with founders create competitive advantages that persist across market cycles. Once a GP builds a strong portfolio and begins supporting these companies through growth, the focus shifts to how returns actually materialize-through exits and the metrics that determine whether a fund succeeded or failed.

How VC Funds Actually Make Money

Venture capital funds generate returns through two distinct mechanisms: capital appreciation when portfolio companies grow in value, and distributions when those companies exit through acquisition or IPO. The math is straightforward but the execution brutal. A fund investing $1 million at a $10 million pre-money valuation owns 9% of the company. If that company reaches a $100 million valuation at Series B, the fund’s stake is worth $9 million on paper. If the company exits at a $500 million acquisition price, the fund receives roughly $45 million from that single investment. However, most startups fail or stagnate, meaning a single successful exit must compensate for numerous write-offs. This reality explains why VC funds need portfolio diversity and why GPs obsess over identifying the rare companies that achieve 10x or 100x returns.

How San Francisco Funds Measure Success

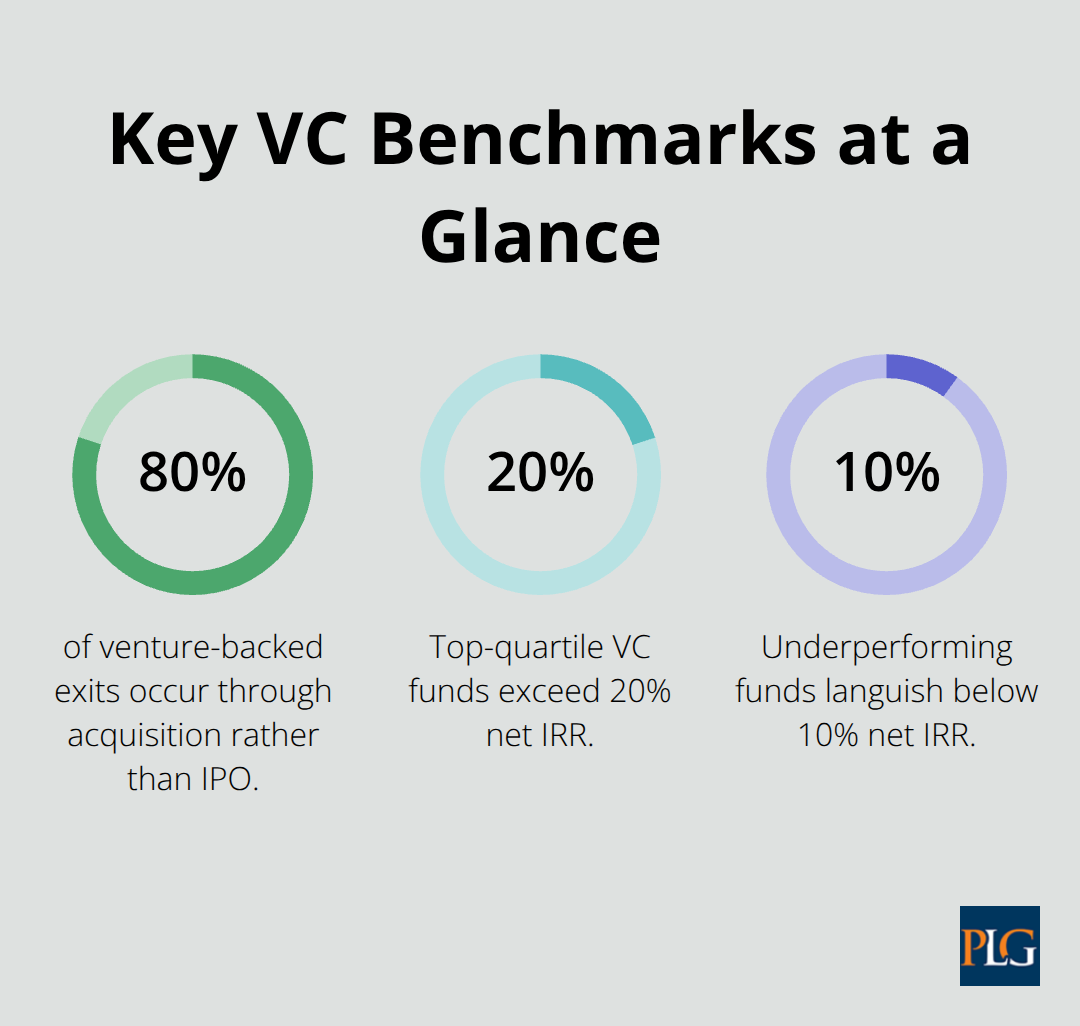

San Francisco firms measure success through five interconnected metrics that LPs scrutinize relentlessly. IRR, or internal rate of return, measures how fast capital compounds; top-quartile funds exceed 20% net IRR, while underperformers languish below 10%. DPI (distributions to paid-in capital) shows actual cash returned to LPs relative to what they invested; anything above 1.5x is solid, above 2.0x is exceptional.

TVPI combines realized and unrealized value to show total returns; a 2.0x TVPI is considered strong. RVPI captures unrealized value in remaining portfolio companies and signals future upside. MOIC ignores time and simply measures gross returns; individual deals hitting 5x or higher drive fund performance, though a fund-level MOIC of 2.5x to 3.5x is considered strong. These metrics interact in complex ways. A fund with high RVPI but low DPI signals unrealized potential but raises questions about whether mark-to-market valuations are accurate. Early-stage funds naturally show higher RVPI and lower DPI since exits take years, while mature funds flip the ratio as companies exit and cash distributions arrive. LPs comparing funds across different ages must contextualize metrics accordingly; a three-year-old fund cannot be judged by the same benchmarks as a nine-year-old fund wrapping up its investment period.

Where Returns Actually Materialize

Acquisition remains the dominant exit path in San Francisco. According to PitchBook data, roughly 80% of venture-backed exits occur through acquisition rather than IPO, with median acquisition prices ranging from $50 million to $500 million depending on sector and timing. A software company with $10 million ARR might sell for 10x revenue, translating to a $100 million exit. A hardware company with similar revenue might fetch 3x to 5x revenue due to lower margins and capital intensity. Acquirers include strategic buyers seeking technology or talent, larger venture-backed companies consolidating their markets, and private equity firms building platforms. The acquirer’s motivation shapes deal terms; a strategic buyer desperate for your technology may offer higher valuations than a financial buyer focused purely on cash flow. IPOs require scale that only a tiny fraction of venture-backed companies achieve. Companies going public typically have crossed $100 million ARR with clear paths to profitability or dramatic growth. In San Francisco, the IPO window opened in 2020 and 2021 but slammed shut in 2022 and 2023 as public market multiples compressed. Secondary sales, where existing investors sell shares to new investors before exit, have become increasingly common as companies stay private longer. A Series F or G company might facilitate a secondary where early VCs cash out portions of their stake rather than waiting for acquisition or IPO.

The Brutal Mathematics of Portfolio Construction

A typical VC fund expects roughly 30% of investments to fail completely, losing all capital. Another 40% to 50% generate modest returns of 1x to 3x invested capital. The remaining 20% to 30% must generate outsized returns of 10x or higher to compensate for failures and mediocre performers. This distribution explains why GPs obsess over identifying the rare category-defining companies early. If a fund invests $50 million across 50 companies at $1 million each, it needs perhaps 2 to 3 companies to return $50 million or more just to break even after fees. Most funds charge 2% annual management fees on committed capital plus 20% carried interest on profits, meaning a $100 million fund generates $2 million annual fees regardless of performance. These fees cover overhead, salaries, and operating costs. Only profits beyond the initial capital invested generate carry, and only if returns exceed an 8% hurdle rate that compensates LPs for the risk premium over public markets. This fee structure creates misalignment between GPs and LPs in underperforming funds; the GP still collects management fees while LPs watch their capital erode. Strong-performing funds attract repeat LP capital and command larger fund sizes, while underperformers struggle to raise subsequent funds.

Performance Across San Francisco’s Fund Landscape

Mega-funds like Andreessen Horowitz and Sequoia manage $4 billion to $5 billion in assets and generate institutional returns, but their size creates inflexibility. They cannot lead seed rounds because a $500,000 investment is immaterial relative to their fund size. Mid-sized funds between $100 million and $300 million often outperform mega-funds on IRR according to 2023 analysis, though mega-funds capture more absolute dollars due to larger check sizes and later-stage exposure. Emerging managers launching inaugural funds face brutal skepticism; LPs scrutinize track records obsessively. A founder who led successful exits at a larger firm gains credibility, but first-time GPs without prior investing experience struggle to raise capital. This gatekeeping explains why VC remains concentrated among repeat players and why emerging managers often start with $30 million to $50 million funds focused on narrow geographies or sectors where they have deep networks. Regional performance varies significantly. San Francisco and New York consistently generate higher returns than other regions due to density of quality startups and follow-on capital availability. A strong company in San Francisco can raise Series A through Series D without geographic friction, while equally strong companies in secondary markets struggle to find later-stage capital, forcing suboptimal exits. Returns also correlate with sector timing; funds that backed cloud infrastructure in 2010 to 2015 generated exceptional returns, while those betting on consumer hardware faced extended timeframes and lower multiples. This sector variability means LP patience and GP conviction matter enormously when returns take years to materialize.

Final Thoughts

Understanding how a venture capital fund works reveals why startup funding concentrates among founders who grasp these mechanics. VC funds succeed when GPs identify rare companies capable of 10x returns, support them through growth, and exit at valuations that compensate for portfolio failures. The math is unforgiving: most startups fail, a few generate modest returns, and a tiny fraction drive outsized gains that justify the entire fund.

For entrepreneurs raising capital in San Francisco, this knowledge matters intensely. You now understand why investors obsess over unit economics, traction metrics, and market wedges rather than polished pitch decks. You recognize that Series A due diligence takes 40 to 60 hours and demands clean cap tables, proper IP assignments, and auditable financials. Founders working with experienced legal counsel navigate these dynamics more effectively, and Primum Law Group guides startups through venture capital transactions, cap table management, and investor negotiations in San Francisco and Silicon Valley.

VC funds shape entire startup ecosystems through capital density, operational support, network access, and follow-on funding that established firms provide. Accelerators like Y Combinator create competitive tension among investors and compress fundraising timelines, while portfolio company networks generate warm introductions and partnership opportunities that accelerate growth. This ecosystem effect means founders benefit not just from capital but from proximity to other founders, operators, and investors solving similar problems.