Equity incentive plan design is one of the most misunderstood decisions startup founders make. Get it wrong, and you’ll struggle to attract talent or retain your best people.

At Primum Law Group, we’ve seen countless startups leave money on the table-or worse, create legal headaches-because they didn’t think through their equity structure carefully. This guide walks you through the mechanics, the mistakes to avoid, and the practices that actually work.

Stock Options and Vesting Schedules in San Francisco Startups

How Stock Options Align Employee and Company Incentives

Stock options remain the primary tool startups use to compete for talent when cash compensation can’t match what employees could earn elsewhere. An option gives an employee the right to purchase company stock at a fixed price, called the exercise price, which equals the fair market value of the stock on the grant date. If the company grows and the stock appreciates, the gap between that original exercise price and the current value becomes the employee’s gain. This structure aligns employee incentives with company growth because the option only becomes valuable if the company succeeds.

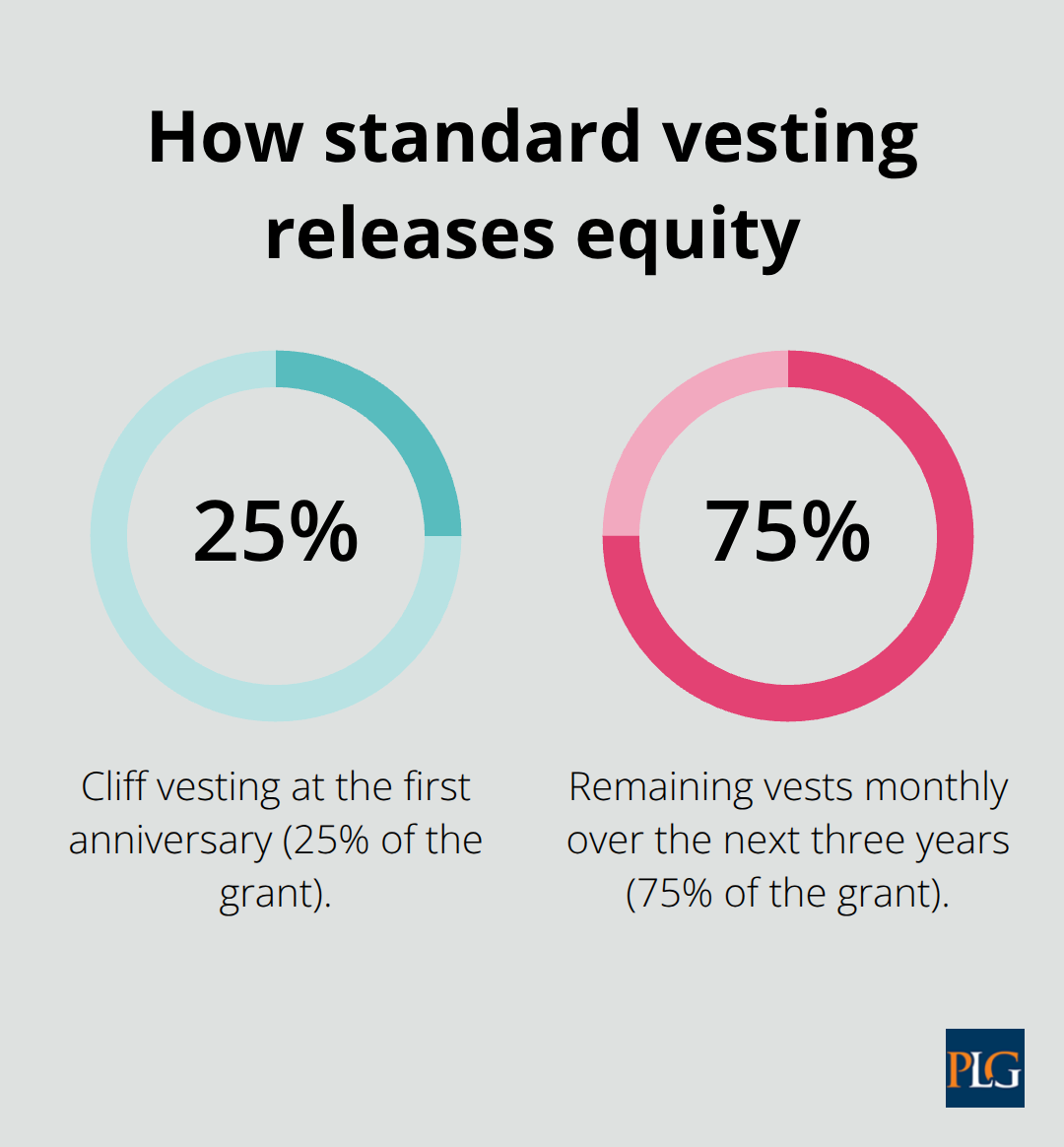

However, the real power of options lies not in the instrument itself but in how you structure the vesting schedule. The standard vesting period in venture-backed startups is four years with a one-year cliff, meaning employees earn nothing until their first anniversary, then gain access to 25% of their grant. After the cliff, the remaining 75% vests monthly over the next three years. This approach solves a critical retention problem: it locks in commitment during the early, uncertain years when the company needs stability most.

Founders sometimes extend vesting to five years to emphasize longer-term alignment, though four years remains the market standard across San Francisco and Silicon Valley startups.

The Cliff: Your Most Powerful Retention Tool

The cliff itself determines whether an employee who leaves early receives any equity at all. A one-year cliff is standard practice, but some startups-particularly those struggling with early turnover-have experimented with shorter cliffs of six months or even three months. Research on startup cap tables shows that employees who vest through a cliff are significantly more likely to stay beyond year one, making this structure one of the highest-impact design choices you’ll make.

When you design your vesting schedule, tie it directly to your expected path to liquidity or significant fundraising. If you plan an IPO or acquisition within five to seven years, four-year vesting ensures that early employees capture meaningful upside at exit. Conversely, if you build a longer-term business, consider refresh grants after year two or three to re-engage top performers whose initial grants are nearly exhausted.

Strike Prices and Securities Compliance

Strike prices must equal fair market value at grant to comply with federal securities rules under Rule 701 and California’s Section 25102(o), but this requirement actually simplifies your planning: you set the exercise price based on a 409A valuation, which is an independent appraisal of your company’s fair value. For 10% shareholders, the strike price must be at least 110% of fair market value.

The Post-Termination Exercise Window Problem

Many founders overlook the post-termination exercise window-the period employees have to purchase their vested shares after leaving the company. Standard windows are 30 to 90 days, but this creates a real problem: employees often lack the cash to exercise and must forfeit vested equity. Clearly document these windows in offer letters and consider secondary sale opportunities or cashless exercise provisions to make participation feasible for departing employees.

These mechanics form the foundation of your equity structure, but they only work if you avoid the common mistakes that undermine retention and create legal exposure. The next section examines the pitfalls that trip up most founders and how to sidestep them.

Where Your Equity Plan Fails

The San Francisco Bay Area raised $177.4 billion in venture funding during 2025, with AI-focused startups driving mega-rounds that concentrate wealth and opportunity in the region. This capital velocity creates intense hiring pressure, and founders responding to that pressure often make equity decisions without thinking through long-term consequences. We’ve reviewed hundreds of cap tables, and the mistakes cluster into three categories that destroy retention, create tax disasters, or both.

Vesting Schedules That Miss Your Business Timeline

Many founders copy the four-year vesting standard without asking whether it fits their company. If you’re building a platform targeting a two-year acquisition window-common in AI infrastructure startups-a four-year cliff means your early team never vests enough equity to feel the upside before exit. Worse, if you extend the cliff to 18 months or two years thinking it increases retention, you’ve created a retention cliff that works backward: employees who make it past year two suddenly have nothing left to earn, and your best people leave right when you need them most.

The math is straightforward: match your vesting schedule to your realistic path to liquidity, and communicate that path explicitly during hiring. If you expect acquisition within 36 months, consider a three-year vesting schedule with a six-month cliff. If you’re targeting a 10-year build, four years with standard monthly vesting works, but plan refresh grants at year three to keep later hires motivated.

Founder Equity That Diverges From Employee Equity

The second pitfall is founder equity that diverges wildly from employee equity without clear justification. Data from real cap tables shows founding CTOs holding around 20% at seed while founding software engineers hold 1%, and by Series A this spreads further: CFOs typically land at 0.75% to 1.0%, VP of Product at 0.29%, and senior engineers at 0.2% to 0.5%.

The number 0% seems to be not appropriate for this chart. Please use a different chart type. These ranges exist for good reasons-founders take more risk, invest time before funding arrives, and negotiate harder.

But when founders hold 40% at Series B while senior engineers who joined at seed hold 0.3%, you’ve created a perception problem that no communication can fix. Employees see the gap and conclude either that founders don’t value their contribution or that the cap table is poorly managed. The actionable fix is to establish explicit grant bands by role and stage before you hire, then stick to them. Document the logic: founders get X% because they assume pre-revenue risk, Series A engineers get Y% because the company is de-risked and they’re replacing founder functions. Transparency here prevents resentment and makes future fundraising easier because investors see a disciplined approach.

Tax Implications You Can’t Ignore

The third failure is overlooking tax implications during plan design. Many founders focus on the exercise price and vesting schedule but miss that Incentive Stock Options (ISOs) carry Alternative Minimum Tax exposure if employees exercise large grants before the company has sufficient liquidity to cover the AMT bill. Non-Statutory Options (NSOs) trigger ordinary income tax at exercise, a cost most employees don’t anticipate. Without modeling both scenarios during grant design, you hand employees an option that looks valuable on paper but becomes worthless when they can’t afford the tax bill.

The solution is to differentiate ISO and NSO grants by role and expected exercise timing, and to provide employees with clear tax projections before they exercise. If your startup has a realistic IPO or acquisition timeline, model the tax impact at exit so employees understand their actual after-tax gain, not just the option value. These three mistakes compound each other: poor vesting schedules reduce retention, misaligned equity creates resentment, and hidden tax costs destroy trust. The next section shows how to build a communication strategy that turns your equity plan into a recruitment and retention weapon instead of a source of frustration.

Building an Equity Plan That Actually Works in San Francisco

Anchor Grants to Company Milestones

Your equity structure only delivers retention and alignment if employees understand what they’re earning and why it matters. The San Francisco Bay Area’s venture concentration-52.3% of all U.S. venture dollars in 2025 according to PitchBook and NVCA data-means competing startups are aggressive about recruiting, and your equity communication either reinforces why staying is valuable or signals that management is disorganized.

Start with concrete company milestones rather than abstract timelines. If you’re building an AI infrastructure company, tie refresh grants or acceleration triggers to product launches, customer acquisition targets, or funding rounds rather than calendar dates. When employees see that their equity accelerates when the company hits Series B or achieves $10 million ARR, they understand the connection between their work and their upside.

Document these milestones in writing during onboarding and reference them during performance reviews so equity doesn’t disappear into background noise. This approach transforms equity from a static grant into a dynamic tool that reinforces company priorities.

Model Tax Exposure Before You Issue Grants

The second actionable step is running tax projections for every grant before you issue it. Model what an employee will owe if they exercise at year two, year three, and at exit under both ISO and NSO scenarios. Share these projections with new hires during offer negotiation so they make decisions with full information about after-tax value. Many founders avoid this step because they fear scaring candidates away, but the opposite is true: candidates who understand their actual tax exposure trust your process more than those left guessing.

If you’re issuing ISOs, flag the AMT exposure explicitly and explain how it affects exercise timing at exit. This transparency prevents surprises that destroy morale later.

Communicate Dilution After Each Funding Round

Treat your equity plan as a living document that evolves with your cap table. After each funding round, run a dilution analysis and communicate it to your team. PitchBook data shows typical dilution of 10–25% per funding round, and employees who see their percentage drop without explanation assume either that founders mismanaged the cap table or that their contribution is less valued than new hires. Instead, send a brief equity update after each round explaining what happened: founders owned 60%, new investors took 20%, the option pool expanded to 15% to attract new talent, and everyone’s percentage dropped but their share count stayed the same and the company valuation increased.

This transparency transforms a potential morale problem into evidence that you’re scaling professionally and managing the cap table with discipline.

Establish Grant Bands by Role and Stage

Finally, establish explicit grant bands by role and stage before you hire your first employee outside the founding team. Your CFO shouldn’t negotiate for 2% while your VP of Engineering lands at 0.5%-that gap signals either that compensation is arbitrary or that you don’t value engineering. Real cap table data from venture-backed companies shows CFOs typically receiving 0.35–1.0% in Series A, VPs of Engineering at 0.32%, and senior software engineers at 0.2–0.5%. Use these ranges as your starting point, document your logic for each band, and stick to it across hiring cycles.

When a candidate pushes back on equity, you have a defensible answer rooted in market data rather than a founder’s mood that day. This consistency builds trust with your team and makes future fundraising easier because investors see a disciplined approach to cap table management.

Final Thoughts

Your equity incentive plan design determines whether your startup attracts the talent you need and keeps them through the critical years before exit. The mechanics matter-vesting schedules, strike prices, and exercise windows all shape how much value employees actually capture-but execution matters more. Founders who treat equity as a one-time decision during incorporation inevitably regret it, while those who revisit their plan after each funding round, communicate dilution transparently, and anchor grants to company milestones build teams that stay through growth.

The San Francisco Bay Area’s venture concentration means you compete against well-funded startups for the same engineers and product leaders, and your equity structure is one of your few advantages over larger companies that match or exceed your salary offers. When you design your plan thoughtfully, model tax implications, and establish clear grant bands by role, you signal that your company operates with professional discipline and values your team’s contribution. Employees who understand their actual after-tax upside and see how their equity accelerates with company milestones become stakeholders rather than hired hands.

Implementation requires legal structure and ongoing discipline-you need a written stock option plan approved by your board, 409A valuations to set strike prices, and securities law compliance under Rule 701 and California Corporations Code Section 25102(o). We at Primum Law Group help startups build equity plans that work by handling the legal structure, cap table governance, and tax planning so you can focus on building your business. If your current plan creates retention problems or you’re uncertain about tax implications before your next funding round, reach out for a consultation on equity strategy.