San Francisco startups face a unique legal landscape that demands more than generic advice. The Bay Area’s regulatory complexity, investor expectations, and competitive pace require startup counsel San Francisco that understands your specific market.

At Primum Law Group, we’ve seen how the right legal foundation transforms growth trajectories. This guide walks you through the legal decisions that matter most at every stage.

Why San Francisco’s Regulatory Complexity Demands Local Counsel

San Francisco and the broader Bay Area operate under a regulatory framework that catches unprepared startups off guard. Unlike generic startup hubs, this region combines California’s notoriously employee-friendly labor laws with San Francisco’s own local ordinances, creating compliance obligations that shift faster than most founders realize. The city’s Paid Sick Leave Ordinance requires all employers to provide at least one hour of paid sick leave per 30 hours worked-a mandate that differs from state requirements and trips up companies relocating from other states. Zoning regulations in SoMa, the Financial District, and Mission Bay each impose distinct restrictions on what types of businesses can operate where, and those rules change. Founders waste months and capital on office buildouts only to discover their intended location violates local use codes.

The California Department of Fair Employment and Housing enforces standards around hiring, promotions, and terminations that are stricter than federal law; a single misclassification of an employee versus contractor exposes your company to back wages and penalties exceeding $10,000. Getting ahead of these requirements from day one isn’t optional-it’s foundational to avoiding costly corrections later.

Investor Expectations in the Bay Area Differ Sharply

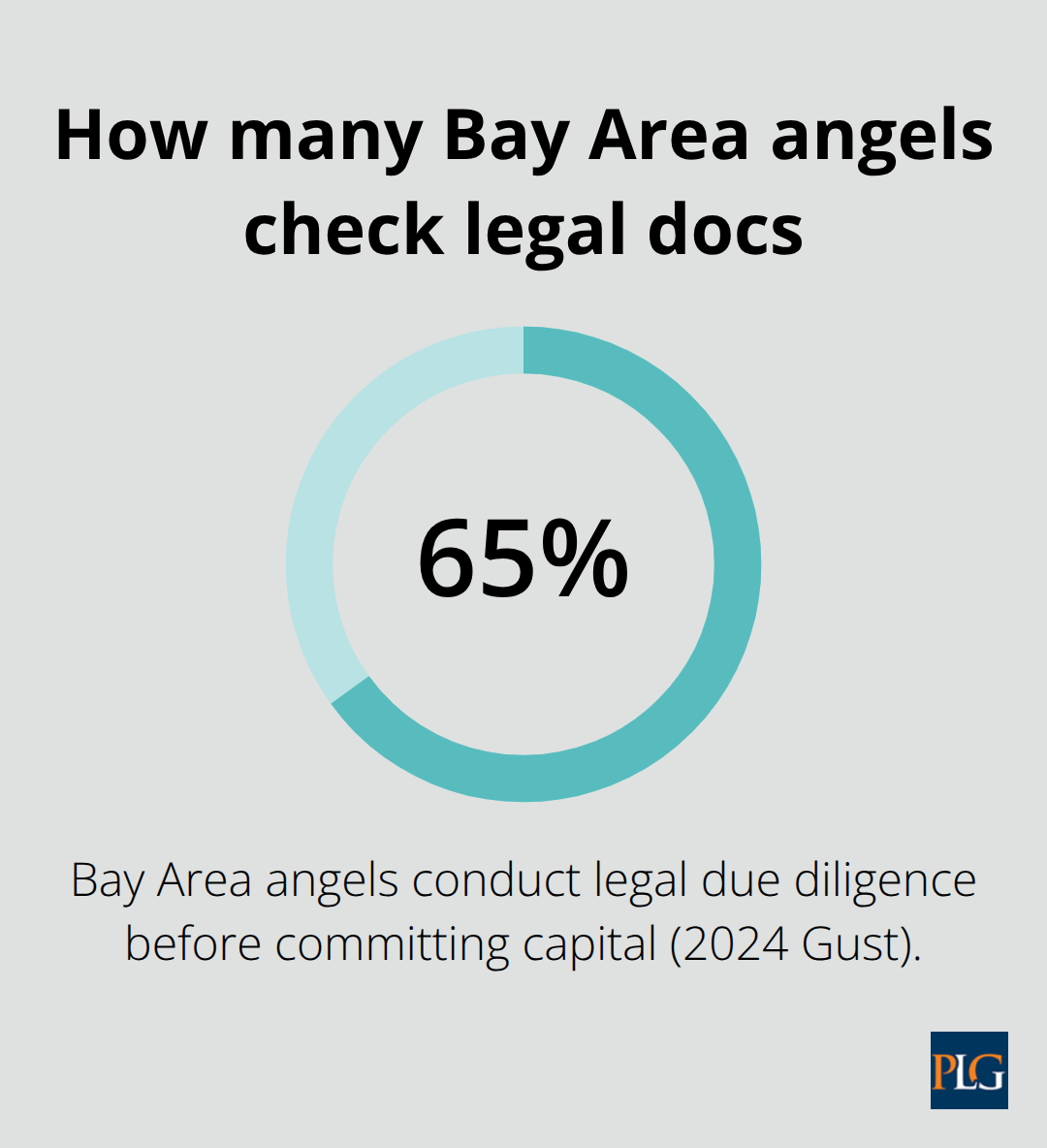

San Francisco investors scrutinize legal documentation at a depth that reflects decades of deal-making in this market. Term sheets, equity plans, and cap tables become non-negotiable checkpoints before capital flows. Investors expect your incorporation documents to be clean, your founder equity vesting schedules locked in place, and your intellectual property assignments documented-not as a nice-to-have, but as a prerequisite. A 2024 Gust report noted that 65% of angel investors in the Bay Area conduct legal due diligence before committing capital, and they will walk if your documentation is incomplete. The standard four-year vesting schedule with a one-year cliff represents market practice here, not a suggestion, and deviations require articulate justification backed by your legal team.

The 83(b) election matters equally; you must file it with the IRS within 30 days of receiving equity, or you face significant tax consequences at exit. Missing that window creates substantial tax differences that compound at liquidity events. Local counsel connected to San Francisco’s investor networks understands which provisions matter most to which players and helps you negotiate terms that work for both sides without unnecessary friction.

Networks Open When Your Legal House Is in Order

The Bay Area’s startup ecosystem rewards founders who move decisively through partnerships, vendor relationships, and investor introductions. Credibility compounds when your legal documents are tight. Venture firms, accelerators, and strategic partners evaluate whether you operate with enough maturity to execute at scale; a half-baked operating agreement or missing IP assignments signal dysfunction and slow down deal progress. Contract templates for NDAs, service agreements, and employment arrangements need to reflect California law specifically-generic templates often miss state-level requirements and create gaps that surface during due diligence. Building genuine relationships with other founders, investors, and service providers in this region means they see you as trustworthy and professional, and that trust starts with legal documentation that stands up to scrutiny. The density of startup activity in San Francisco makes founder equity disputes and cap table conflicts surprisingly common; counsel who understands local practice resolves these issues quickly and protects your reputation while keeping momentum intact.

How Equity Structure Shapes Your Fundraising Path

Your equity documentation directly influences how investors evaluate your company and how quickly they move forward. Vesting schedules, acceleration terms, and post-termination exercise windows all affect investor confidence and your ability to retain talent. Performance-based vesting can create ambiguity in early-stage startups unless you define metrics clearly; disputes over vesting terms have derailed partnerships and delayed funding rounds. The distinction between vested and exercisable equity matters more than most founders realize-post-termination exercise windows should be negotiated early to protect liquidity and planned exits. Single-trigger acceleration vests upon a change of control, while double-trigger acceleration requires both a change of control and a qualifying termination; investors typically prefer double-trigger terms because they preserve unvested equity during exits. Precisely defining what constitutes a change of control (asset sale, 50%+ ownership shift, or other triggers) determines when acceleration applies, and that scope requires careful negotiation. Small changes in acceleration, exercise windows, or repurchase rights can materially affect your payout at exit, making professional review of equity grants a high-return investment.

Building a Clean Cap Table Before You Pitch

Investors scrutinize capitalization tables during due diligence, and inconsistencies or gaps create friction that delays funding. A clean cap table reflects every equity issuance, vesting schedule, and outstanding option grant in a format that investors recognize immediately. Equity documents interconnect across plans, awards, and employment agreements; a holistic review across all related documents identifies gaps and inconsistencies before they surface during fundraising. Fundraising rounds often trigger amendments to equity plans or new terms affecting acceleration rights, and alignment across all related documents becomes critical. Before major rounds (Series A and beyond), tailor acceleration protections and definitions (such as “good reason” terminations) and consider adjusting post-termination exercise windows to align with company incentives. M&A readiness benefits from consistent equity documentation; buyers scrutinize acceleration terms during due diligence and move faster when your cap table is clean and your equity history is transparent. Effective equity strategy starts with a full review of the entire history of equity issuances and governing plan documents to identify gaps and inconsistencies that could slow down your next funding round or exit.

Legal Structures That Fuel Startup Growth

Founders often spend weeks debating between an LLC and a C-corporation without understanding how that choice compounds over time. The reality is sharp: a C-corporation is the only structure that works if you plan to raise institutional capital in San Francisco. Venture investors will not commit to LLCs or S-corporations because they cannot hold preferred equity or implement standard liquidation preferences. The Delaware C-corporation has become market standard for this reason, and any deviation requires articulate justification that most investors will reject outright. Formation costs around $500 to $1,500 with counsel, but the downstream friction of restructuring later costs exponentially more. Some founders use a holding company structure to isolate specific assets (IP, real estate) from operating company liability, which works when you have multiple revenue streams or significant real estate holdings, but adds complexity and annual compliance costs that only justify themselves at scale. Incorporate before you issue any equity, not after. Founders who hand out equity before incorporation create cap table chaos because those early grants sit outside your official equity plan and become nearly impossible to reconcile during due diligence.

Why Timing Your Incorporation Matters

The moment you incorporate shapes your entire cap table history. Founders who wait until after they’ve promised equity to cofounders or advisors face reconstruction nightmares that investors scrutinize heavily during due diligence. Your incorporation documents establish the baseline from which all future equity flows, so getting this right from day one prevents months of friction later. A clean incorporation record shows investors that you operated with discipline from the start.

Building a Cap Table That Investors Accept

Your cap table reflects every equity grant, option, warrant, and convertible note ever issued, and investors will walk if the history is incomplete or contradictory. Founders often discover that early cofounders never signed proper vesting schedules, that advisor equity was issued informally without documentation, or that option grants reference an outdated plan document. A 2024 analysis of startup due diligence found that cap table inconsistencies delay funding by an average of six weeks and sometimes kill deals entirely. You need a single source of truth that shows every security, every holder, fully diluted ownership percentages, and vesting status. Tools like Pulley or Carta help track this, but they only work if your underlying equity documents are clean and consistent.

Vesting Schedules and Equity Terms That Align with Market Practice

The four-year vesting schedule with one-year cliff has become market standard in San Francisco, but the terms inside that schedule matter enormously. Define precisely what constitutes good reason for termination, what happens to unvested equity if the company is acquired, and what exercise window employees have after departure. Performance-based vesting introduces risk if you do not define metrics in advance; disputes over vesting milestones have derailed partnerships and delayed funding rounds. Small changes in acceleration, exercise windows, or repurchase rights can materially affect your payout at exit, making professional review of equity grants a high-return investment.

Founder Agreements That Prevent Costly Disputes

A single-page handshake between cofounders creates disputes that consume months and capital. Your founder agreement should address ownership percentages, decision-making authority, what happens if a cofounder leaves, and how equity vests. These conversations feel awkward early on, but they prevent the legal and emotional damage that surfaces when cofounders disagree about control or exit strategy. A well-drafted founder agreement protects all parties and keeps focus on building the company rather than fighting over governance.

Intellectual Property Assignment as a Non-Negotiable Foundation

Intellectual property assignment demands explicit attention because California courts will not automatically assign inventions to the company unless your employment agreement contains a clear assignment clause. Every employee and contractor must sign an agreement that assigns all work product to the company, or you risk disputes over ownership of core innovations. A single technology platform or algorithm that remains in dispute can block funding, partnerships, and exits entirely. Missing or ambiguous IP assignments have stopped founders from scaling their own companies, and fixing this problem retroactively costs far more than getting it right from the start.

These structural and equity decisions set the stage for how investors evaluate your company and how quickly they move forward. The next section addresses the legal mistakes that slow down growth even when your structure is sound.

Common Legal Mistakes That Slow Down Growth

Contracts That Leave Your Company Exposed

Founders often treat contracts as a formality to complete quickly, then shift focus to product and sales. This approach costs companies tens of thousands in disputes, lost partnerships, and delayed funding. Vendor agreements that lack clear payment terms and dispute resolution procedures create friction when deliverables miss expectations. Employment contracts missing California-specific wage and hour language expose you to Department of Industrial Relations investigations. Service agreements that fail to address liability caps or indemnification leave both parties vulnerable to unexpected costs.

A 2023 study by the American Bar Association found that startups without properly documented contracts face an average of $47,000 in dispute costs when disagreements arise. The damage extends beyond money; a vendor dispute over deliverables can derail a critical product launch, and an employee misclassification can trigger investigations that consume months of management attention. Generic contract templates downloaded from the internet rarely account for California’s employee-friendly statutes, San Francisco’s local ordinances, or your startup’s operational realities.

Your NDA must address how confidential information flows between parties and include survival periods that extend beyond the agreement term. Service agreements need explicit liability caps, indemnification clauses that protect both sides, and clear termination provisions specifying notice periods and wind-down obligations. Employment agreements must include California-compliant non-solicitation language because non-competes are unenforceable in California unless they meet strict statutory requirements. Contractor agreements require explicit language confirming independent contractor status to avoid misclassification audits; the IRS applies a three-part test based on behavioral control, financial control, and relationship type, and ambiguous language invites scrutiny. Founders who invest two or three hours upfront with counsel to customize templates for their specific circumstances avoid months of friction later.

Compliance Obligations That Arrive Faster Than Expected

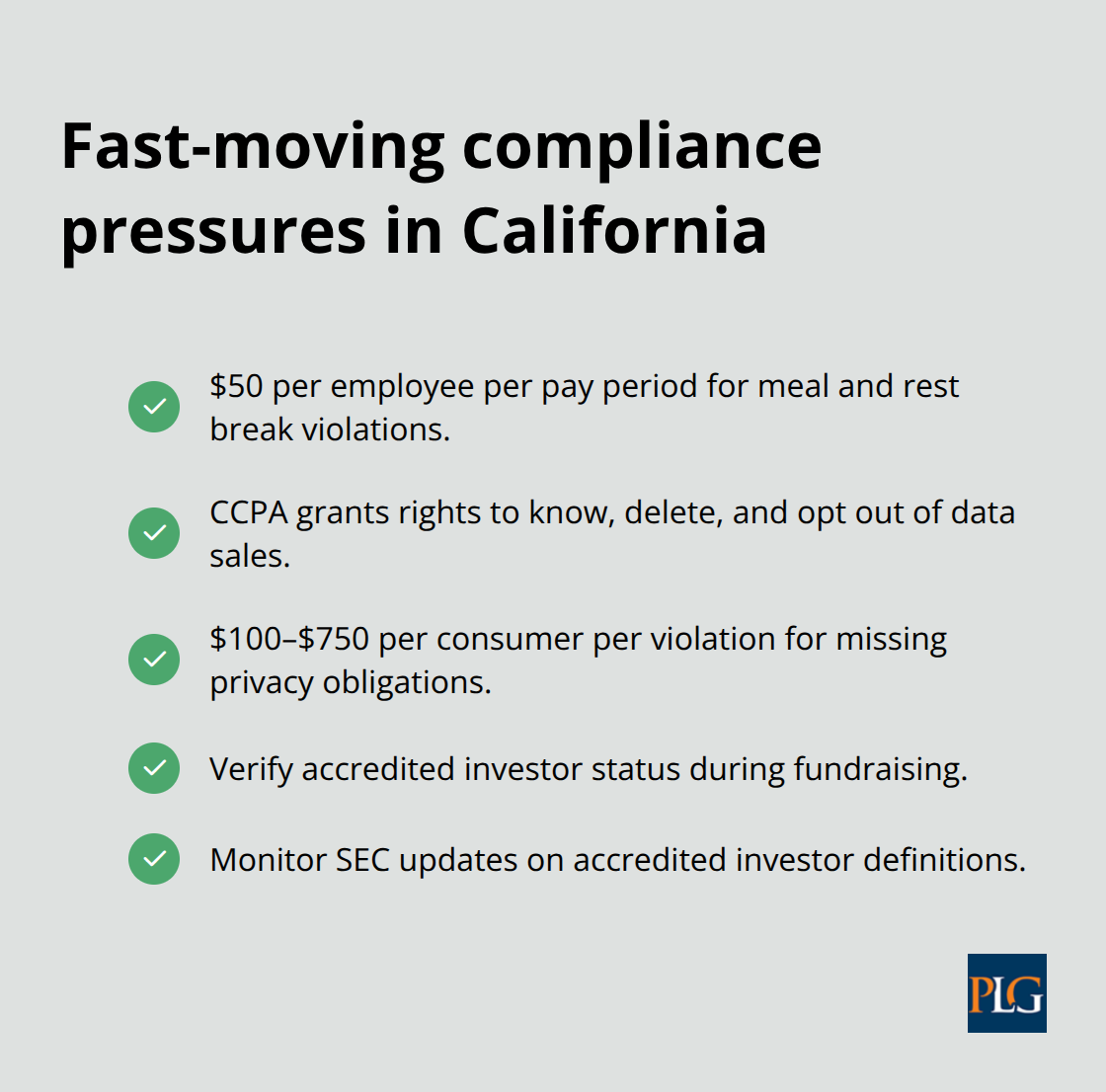

Compliance requirements surface faster than most founders anticipate, and missing early obligations creates cascading penalties that compound. California requires all employers to provide paid sick leave at a minimum of one hour per 30 hours worked, which differs from federal law and catches companies relocating from other states off guard. San Francisco adds its own Paid Sick Leave Ordinance with distinct accrual and payout rules that supersede state minimums. The California Department of Fair Employment and Housing enforces anti-discrimination and anti-retaliation standards stricter than Title VII, and a single improper termination can trigger lawsuits exceeding $100,000 in damages and attorney fees.

Wage and hour violations carry penalties of $50 per employee per pay period for improper breaks or meal periods, and those penalties accumulate quickly across a growing team. Data privacy obligations kick in immediately if you collect customer information; California’s Consumer Privacy Act grants consumers rights to know what data you collect, delete it on request, and opt out of sales. Missing privacy notices or failing to implement data deletion procedures exposes you to statutory penalties of $100 to $750 per consumer per violation.

Fundraising introduces additional compliance layers: if you accept investment from accredited investors, you must verify their accreditation status or face liability for securities law violations. The SEC recently invited comments on accredited investor definitions, signaling potential changes to what qualifies, so staying current on investor verification standards matters.

Founders who establish compliance checklists from day one, assign clear ownership of each obligation, and conduct quarterly reviews catch gaps before regulators or investors do. Tools like Ironclad or Atheneum help track compliance deadlines, but they only work if you know which obligations apply to your business.

Fundraising Agreements That Create Disputes at Exit

Fundraising agreements that lack precision create disputes between founders and investors that damage relationships and delay exits. Term sheets often include provisions around liquidation preferences, anti-dilution protection, and board rights that founders negotiate hastily without fully understanding downstream consequences. A 1x non-participating preferred stock means investors receive either their preference amount or their pro-rata share of proceeds, whichever is greater; a 1x participating preference means they receive their preference amount plus their pro-rata share, creating situations where investors recover more than common shareholders in lower-exit scenarios.

The distinction matters enormously. At a $20 million exit with $5 million in preferred equity, a participating preference generates $7.5 million to investors while common shareholders receive $12.5 million, but a non-participating preference distributes proceeds pro-rata. SAFEs and convertible notes require explicit language around valuation caps, discount rates, and pro-rata participation rights; ambiguous terms create disputes when conversion triggers at Series A pricing. The post-termination exercise window determines how long founders have to purchase vested equity after departure, and windows shorter than 90 days force founders to choose between expensive stock purchases or forfeiture within weeks of leaving.

A standard 10-year exercise window aligns with market practice, but many startups impose 30 or 60-day windows that strip founders of liquidity and create resentment. Double-trigger acceleration requires both a change of control and a qualifying termination to vest remaining equity, while single-trigger acceleration vests upon acquisition alone; investors prefer double-trigger because it preserves unvested equity during exits, but founders should negotiate what constitutes a qualifying termination to protect themselves. A change-of-control definition must specify whether asset sales, stock sales, mergers, or ownership shifts above a certain threshold (typically 50%) trigger acceleration; vague definitions create disputes when exits occur through non-standard structures. Founders who negotiate these terms with clarity upfront, document them consistently across all equity documents, and align them with investor expectations avoid disputes that surface during due diligence or at liquidity events.

Final Thoughts

San Francisco startups operate in a market where legal missteps compound faster than anywhere else. The regulatory complexity, investor scrutiny, and competitive pace demand startup counsel San Francisco that understands your specific market and removes friction at every stage. A clean cap table, properly documented equity agreements, and compliant employment contracts signal maturity to investors and accelerate their decision-making.

The legal decisions you make today shape your fundraising trajectory, your ability to retain talent, and your exit value. Missing IP assignments, ambiguous vesting terms, or incomplete compliance checklists create delays that compound into months of lost momentum. Fixing these problems retroactively costs far more than getting them right from the start.

Local counsel connected to San Francisco’s investor networks understands which provisions matter most to which players and helps you negotiate terms that work for both sides. Schedule a conversation with Primum Law Group to review your current legal foundation and identify where tightening your structure creates the most value.