Picking the right venture capital investment funds can make or break your startup’s future. The difference between a fund that actively supports your growth and one that simply writes checks is substantial.

At Primum Law Group, we’ve seen founders waste months evaluating the wrong funds or missing critical red flags in fund structures. This guide walks you through the exact criteria that matter.

Understanding Venture Capital Fund Structure in San Francisco

Fund structure determines how a venture capital firm operates, who benefits from returns, and what incentives drive their investment decisions. Most founders focus on the check size and brand name, but the mechanics beneath the surface directly impact how much support you’ll receive and whether the fund’s goals align with yours. In San Francisco, where competition for capital is fierce, understanding these mechanics separates founders who negotiate from those who simply accept terms.

Matching Your Stage to Fund Size

Venture funds come in distinct flavors based on their size and stage focus. A fund managing $50 million operates entirely differently from one with $500 million. Smaller funds back pre-seed and seed companies, writing checks between $250,000 and $2 million, because larger check sizes would consume too much of their portfolio. San Francisco venture capital firms target companies at seed through Series B stages, with investments between $1 million and $15 million per round. Y Combinator deploys roughly $500,000 per company, reflecting its batch model and early-stage focus. Benchmark and similar mid-sized funds often start with $3–5 million and reserve capacity to invest $10–15 million over a company’s lifetime, signaling they expect significant follow-on investment and growth.

Most founders chase the largest fund name without asking whether that fund actually invests at their stage. A $1 billion fund may have zero interest in a $100,000 pre-seed round because it won’t meaningfully impact their returns. You must match your funding need to a fund’s actual check size range, not their total assets under management.

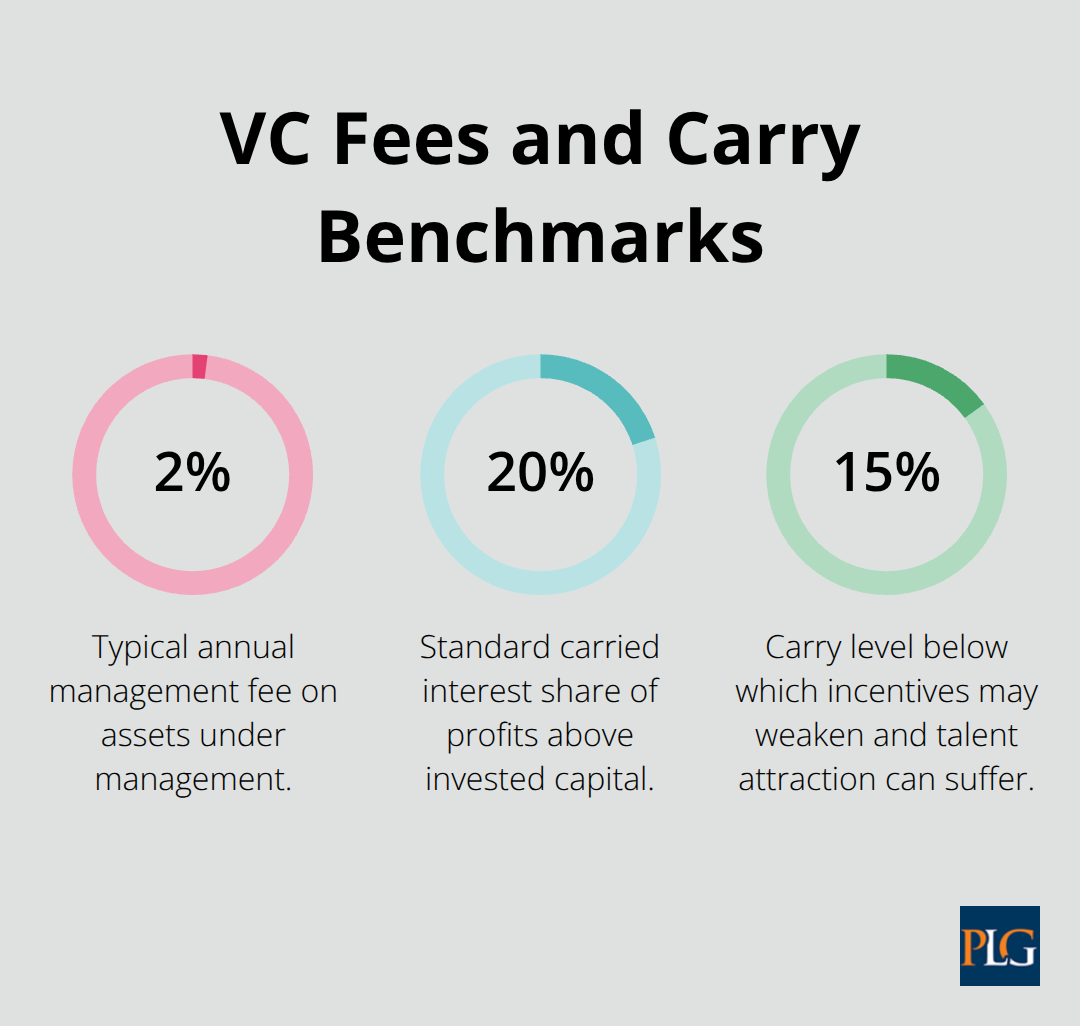

How Fees and Carry Shape Fund Behavior

Management fees and carried interest determine whether a fund prioritizes your success or simply needs exits to cover operating costs. Standard venture funds charge 2% annually on assets under management, though this varies. A $100 million fund paying 2% management fees generates $2 million yearly for operations, salaries, and due diligence. Carried interest, typically 20%, means the fund takes one-fifth of all profits above the initial investment.

Some funds negotiate lower carry (17–18%) in exchange for higher management fees.

This matters because a fund burning through management fees without strong exits faces pressure to deploy capital quickly, sometimes into weaker opportunities. The best funds have sufficient management fees to operate independently while carry incentivizes genuine returns. Watch for funds with management fees above 2.5% on smaller funds-they may be charging founders for operational inefficiency. Conversely, funds with carry below 15% may not attract top talent or take enough risk. The healthiest structure aligns the fund’s survival with your success, not against the clock.

Geographic Presence and Network Strength

Location matters less than it did ten years ago, but network depth still correlates directly with value. San Francisco funds like Accel, Greylock, and Spark Capital operate globally but maintain deep roots in the Bay Area, giving their portfolio companies access to engineering talent, customer networks, and follow-on investors concentrated there. Greylock focuses on enterprise, consumer, and crypto software from pre-seed through Series A and beyond, with hands-on founder support. Spark Capital has backed Twitter, Slack, Discord, and Wayfair, signaling both breadth and sustained conviction in scaling companies.

A fund’s geographic footprint reveals where it can actually help. If your market is enterprise software sold to European companies, a fund with offices in London and Berlin adds tangible value beyond capital. If you’re building consumer hardware, proximity to manufacturing networks in Asia matters. The San Francisco fundraising landscape includes numerous angel and VC firms, creating density that cuts both ways: more capital available but also more competition for attention.

Ask potential investors specifically which three portfolio companies they’ve connected you to, and whether those introductions happened before or after you signed the term sheet. A fund claiming strong networks but unable to name recent introductions is selling a myth. The next section examines how to evaluate whether a fund’s track record actually supports its claims about value-add and returns.

Evaluating Fund Performance and Track Record in San Francisco

IRR, DPI, and TVPI: Understanding What Numbers Actually Mean

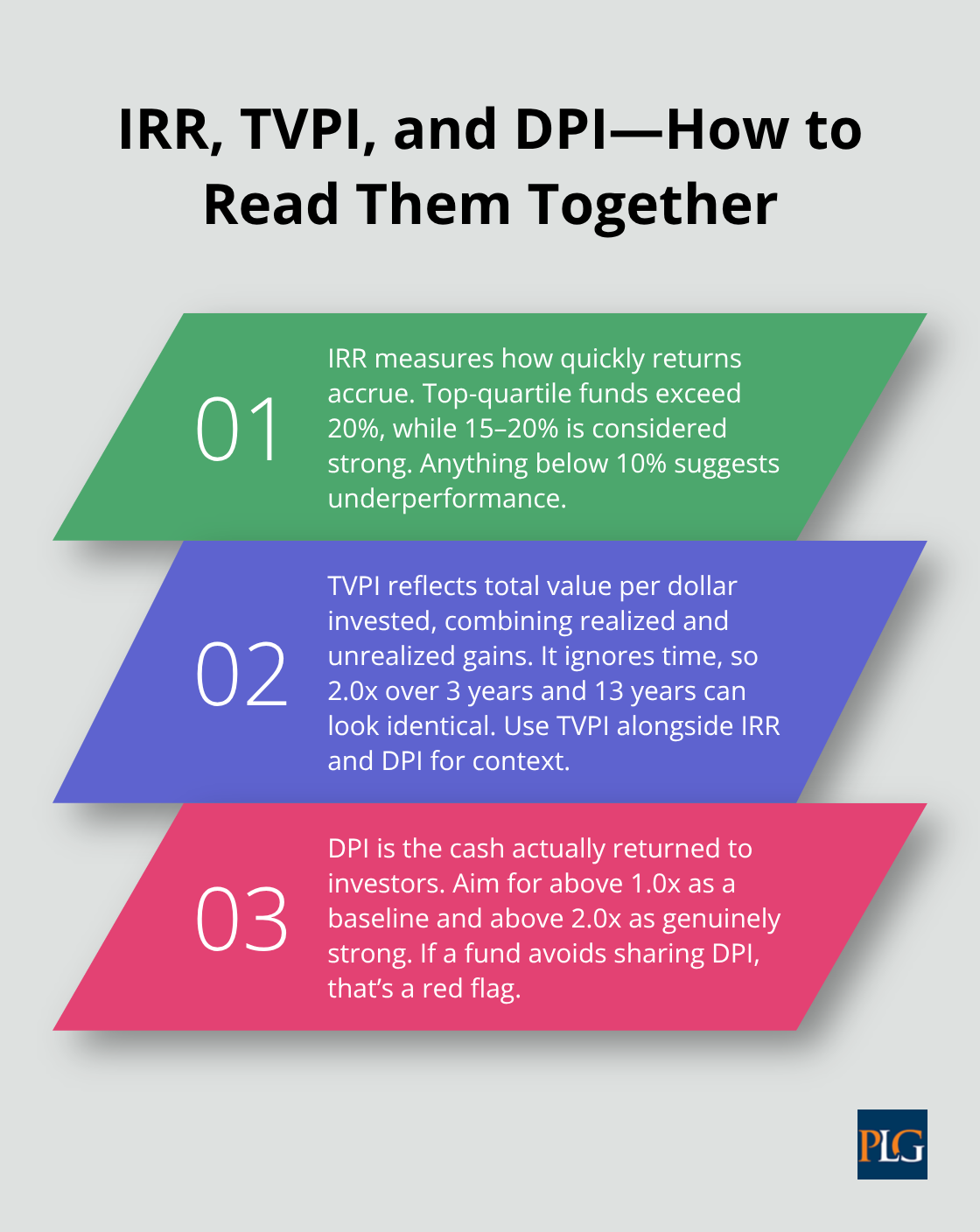

Fund performance metrics tell wildly different stories depending on which number you examine. IRR, or internal rate of return, measures the speed of returns and separates genuinely strong performers from mediocre ones. Top-quartile venture funds achieve IRR above 20%, while 15–20% counts as strong. Anything below 10% suggests the fund has struggled to generate real value. However, IRR alone misleads because a fund could hit 25% IRR on a single massive win while losing money on 90% of its portfolio.

TVPI, or total value to paid-in capital, combines realized and unrealized returns to show total value per dollar invested, but it ignores time entirely. A fund returning 2.0x TVPI over 3 years versus 13 years appears identical on paper despite vastly different performance. DPI, distributions to paid-in capital, measures actual cash returned to investors and anchors confidence in real outcomes. Try for funds with DPI above 1.0x at minimum and above 2.0x as genuinely strong.

When you speak with a fund, request their IRR, DPI, and TVPI together. If they cite only one metric or avoid discussing DPI, that signals they’re hiding weak realized returns. San Francisco funds publish these figures inconsistently, so request audited performance data directly and cross-reference with portfolio founder interviews.

Portfolio Success Rates Reveal True Performance

Portfolio success rates matter more than raw fund size. A $500 million fund backing 80 companies with only 3 meaningful exits operates at a 3.75% hit rate, while a $100 million fund with 15 companies and 5 strong exits operates at 33%. The difference between these two funds is stark: one fund deployed massive capital with minimal returns, while the other generated superior outcomes with disciplined deployment.

The fund manager’s background determines whether they can actually support companies through scaling. Look for partners who founded companies themselves or held operating roles before investing. Greylock’s team includes founders and operators who understand the grinding reality of building software at scale. Benchmark partners typically spend 40+ hours monthly per portfolio company during critical periods.

Vetting Fund Managers and Their Track Records

Ask specific questions about each partner’s background: How many board seats does each partner hold? What was their last operational role? How long did they spend at their previous company before investing? Managers who never ran a business often make naive decisions about unit economics or market timing.

Request introductions to three portfolio founders who exited in the last three years and three who failed or shut down. Successful funds welcome this scrutiny because strong returns speak for themselves. Weak performers dodge these conversations. The founders who exited successfully will tell you whether the fund actually helped or simply collected carry. Their candid feedback reveals whether the fund’s network, operational guidance, and follow-on capital actually accelerated growth or merely provided initial funding. To deepen your investment knowledge, explore venture capital podcasts for aspiring investors based in San Francisco for additional insights and advice.

Key Criteria for Selecting the Right VC Fund in San Francisco

Match Your Stage to Fund Investment Thesis

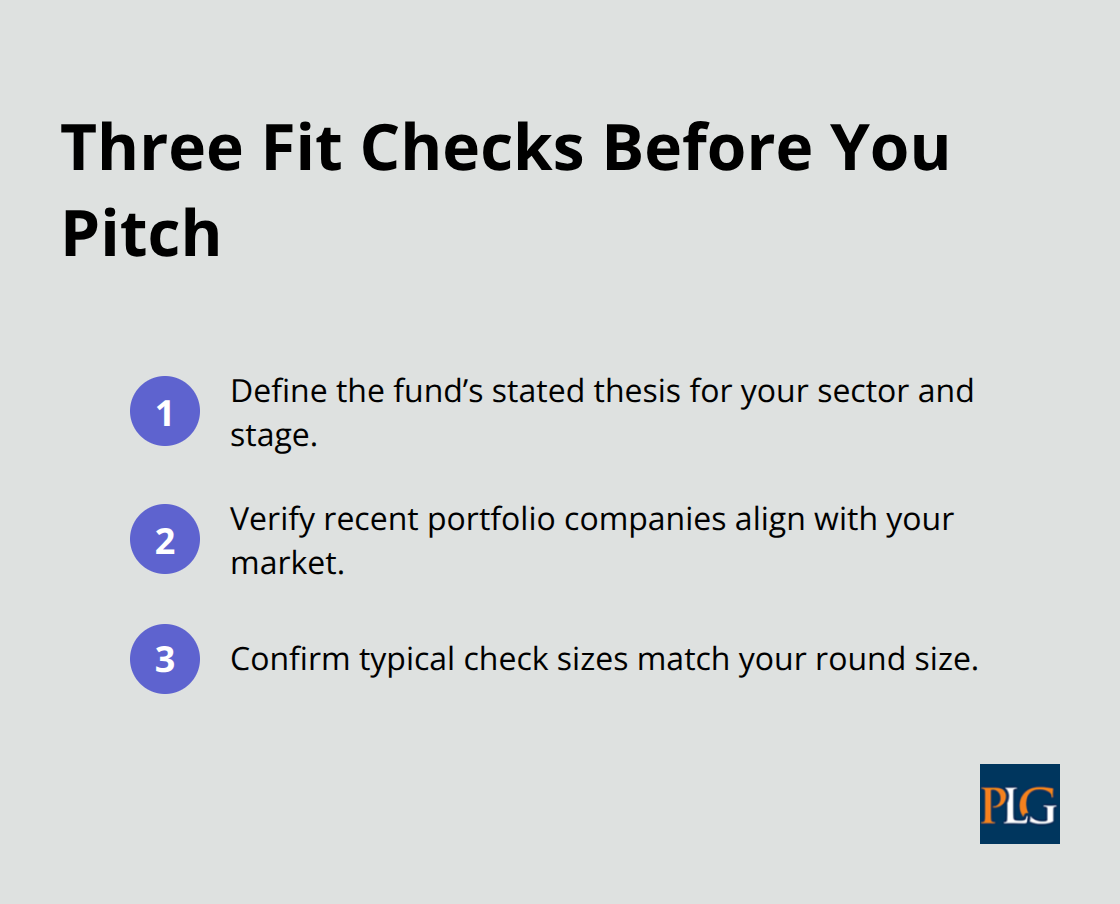

The most common mistake founders make is treating all venture capital as interchangeable. A $500 million fund backing enterprise software has nothing to offer a consumer mobile app, yet founders pitch both indiscriminately. Your task is narrowing to funds whose actual portfolio proves they understand your market, stage, and growth trajectory. Start by mapping three attributes: the fund’s stated investment thesis, the companies they’ve backed in your sector, and the check sizes they deploy at your stage. If a fund claims to back seed-stage fintech but their portfolio shows only Series B and later companies, they’re either lying about their focus or have abandoned early-stage investing.

Accel funds across pre-seed through growth stages globally, which means founders at any stage might fit, but Accel’s enterprise software focus means consumer hardware founders waste time pitching there. Greylock explicitly targets enterprise, consumer, and crypto software, so if you’re building in one of those sectors, the fit is clearer. Cross-reference the fund’s website claims against their actual recent checks using Crunchbase or PitchBook-the data reveals whether stated thesis matches reality.

Evaluate Network Depth and Geographic Advantage

Geography and network depth determine whether a fund can actually move your needle beyond capital deployment. San Francisco funds maintain concentrated networks of engineering talent, customer relationships, and follow-on investors that genuinely accelerate growth for companies in their backyard, but this advantage evaporates if your business operates in a different geography or customer base. Ask each fund manager to name five specific introductions they’ve made to their portfolio companies in the last twelve months-introductions to customers, hires, or partners, not follow-on investors. A fund unable to list concrete examples is admitting their network claims are marketing.

The strongest funds operate hands-on support structures: Unusual Ventures assigns operating advisors to portfolio companies; Greylock’s partners spend dedicated time on portfolio success beyond board meetings. Request introductions to two portfolio founders at companies similar to yours and ask directly whether the fund’s network or operational guidance accelerated growth. Founders tell the truth about whether a fund actually helped them hire a VP of Sales or land their first enterprise customer.

Assess Value-Add Beyond Capital Deployment

Value-add beyond capital separates funds worth your time from those simply deploying capital on a schedule. A fund writing checks quarterly regardless of company progress optimizes for deployment, not outcomes. The funds that matter most provide concrete support: introductions to customers and talent, operational guidance during scaling phases, and strategic advice tailored to your market. When you speak with potential investors, ask them to describe their involvement with three portfolio companies over the past year (not just board meetings, but active problem-solving). Vague answers signal that the fund treats portfolio companies as passive investments rather than active partnerships.

Final Thoughts

Building a focused list of 15–20 venture capital investment funds whose portfolios match your sector and stage prevents months of wasted effort with misaligned investors. Cross-reference their stated thesis against recent investments using Crunchbase or PitchBook, then request audited performance data showing IRR, DPI, and TVPI together rather than isolated metrics. Contact three portfolio founders from each fund-two successful exits and one failure-and ask directly whether the fund’s network and operational guidance accelerated growth or simply provided capital.

Fund structures, carry arrangements, and investor rights require careful review to protect your equity and control as you negotiate terms. The difference between a fund that actively supports your growth and one that simply writes checks compounds over years, making legal clarity essential before you commit to any partnership. Misaligned incentives or poorly structured terms can undermine your long-term control and dilute your ownership far beyond what the initial check size suggests.

We at Primum Law Group work with founders throughout San Francisco and Silicon Valley to structure fundraising rounds, review term sheets, and navigate investor agreements that protect your interests. Our team handles venture capital transactions, startup counseling, and corporate governance to align your fundraising with your long-term goals. Contact Primum Law Group to discuss your specific situation and receive tailored guidance on fund selection and negotiation.