The venture capital landscape is shifting faster than most founders realize. Mega-rounds are becoming standard, Series A investments are drying up, and money is flowing to places beyond San Francisco.

At Primum Law Group, we’ve watched these venture capital industry trends reshape how startups get funded. This guide breaks down what’s actually changing and why it matters for your business.

Mega-Rounds Are Reshaping Who Gets Funded

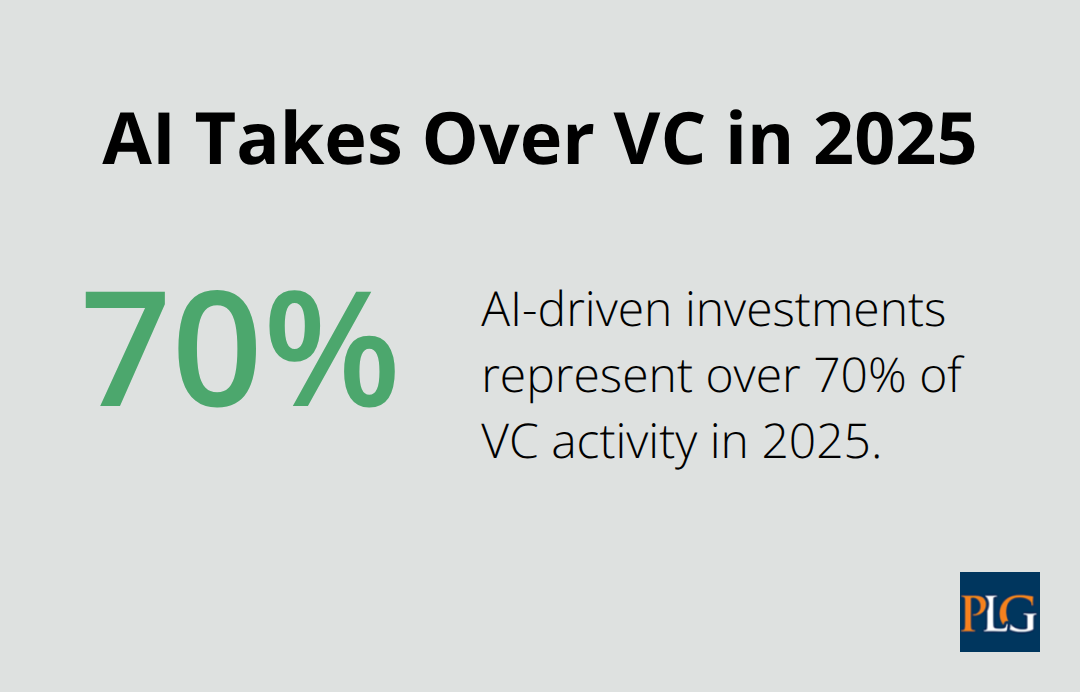

The venture capital market has fundamentally shifted, and founders chasing traditional Series A rounds are running into a wall. In 2025, AI-driven investments now represent over 70% of VC activity, with mega-rounds dominating the landscape. OpenAI’s $40 billion round in 2025 set a new valuation benchmark that rippled across the entire Bay Area funding ecosystem.

This concentration of capital into a handful of AI firms means that non-AI startups face a much tighter fundraising environment. The top 14 Bay Area AI startups by funding illustrate a winner-takes-most dynamic that leaves early-stage founders scrambling for capital. Series A investments have contracted significantly as investors skip early rounds entirely and wait for companies to demonstrate traction before writing larger checks. This shift forces founders to rethink their funding strategy from day one. You need to reach profitability or near-profitability faster than previous generations did, because investors no longer view rapid burn as a badge of honor. The data is clear: founders who build sustainable unit economics and show a clear path to profitability attract capital in this environment. Companies that chase growth at all costs now struggle to raise follow-on rounds, while those with disciplined spending and real revenue traction command investor attention.

What This Means for Your Funding Timeline

The traditional venture funding sequence no longer applies. Many startups that would have raised Series A five years ago now must bootstrap, raise smaller seed rounds, or find alternative capital sources. If you’re building outside the AI sector, try to reach product-market fit and demonstrate meaningful revenue before investors take you seriously for larger rounds. Convertible notes and SAFEs have become the primary tools for early-stage funding because they defer valuation discussions until later rounds when you have stronger metrics. Your burn rate matters more than your growth rate. Investors scrutinize cash runway and unit economics with intensity they rarely applied in previous cycles. Build financial models that show path to profitability within 18 to 24 months, not speculative hockey-stick curves. This shift also means that late-stage companies with proven business models attract capital at unprecedented scales. If you’ve reached Series C or D with strong metrics, you’re positioned to raise massive rounds that would have seemed impossible just three years ago.

The Role of Debt and Alternative Capital

Mega-rounds aren’t the only source of growth capital anymore. Many startups turn to venture debt to extend runway without diluting equity further. Venture debt providers have tightened terms, typically requiring revenue multiples of 1.5x to 3x annual recurring revenue, but the capital remains available for companies with demonstrable traction. This creates a two-tiered market: companies with strong metrics access cheap debt and equity simultaneously, while earlier-stage companies with unproven models face higher hurdle rates. Secondary sales and employee secondary transactions have also become significant liquidity sources. Secondary market activity is rising, providing greater liquidity and exit flexibility for venture portfolios according to the PitchBook-NVCA Venture Monitor. This means earlier employees can diversify their holdings without waiting for an IPO or acquisition, which changes retention dynamics across the industry.

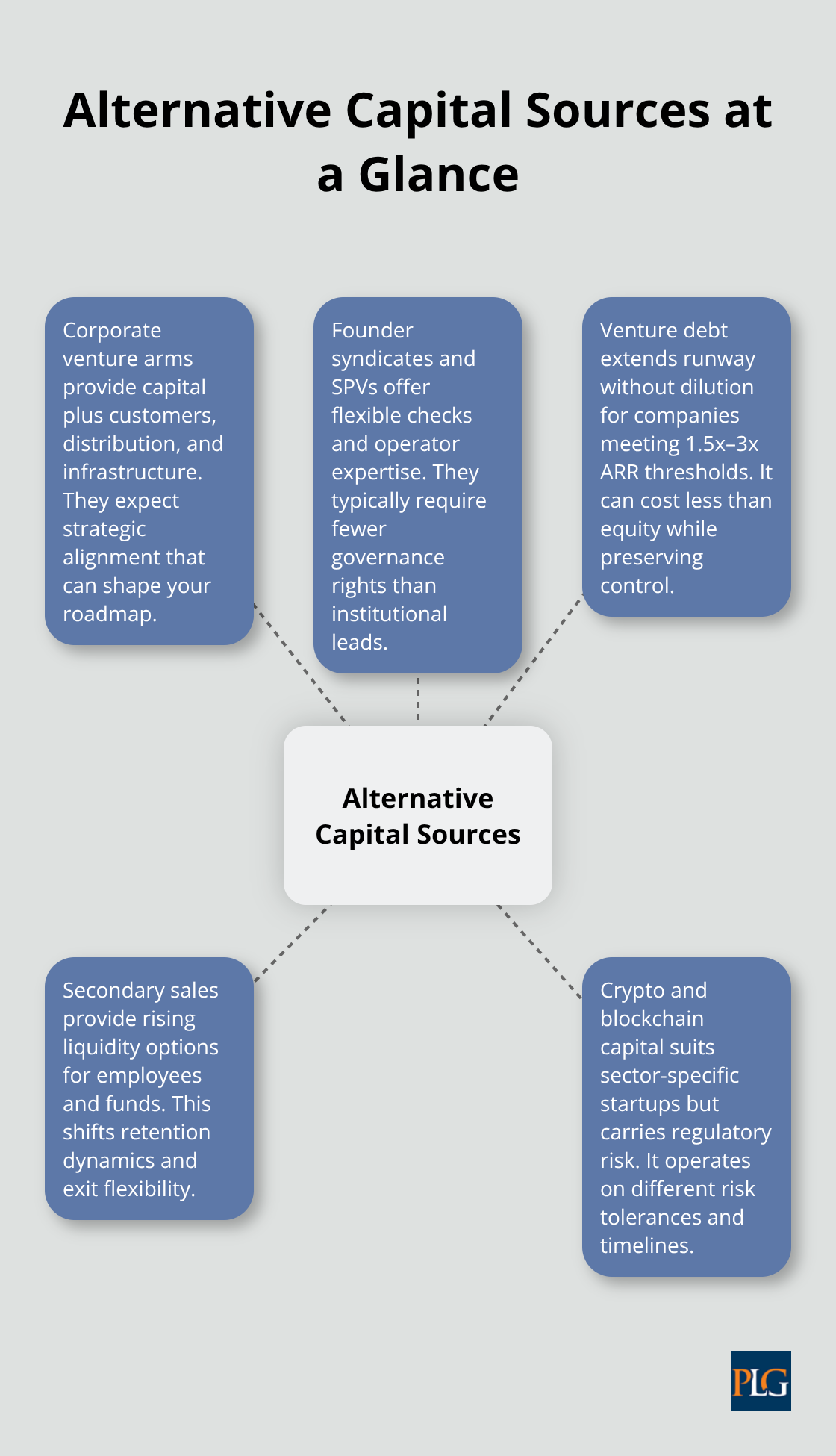

How Alternative Funding Sources Fill the Gap

Corporate venture capital arms have stepped in to fill the void left by traditional VC pullback from early-stage rounds. These corporate investors often bring strategic value beyond capital, including distribution channels, customer access, and technical resources. Founder-led syndicates and special purpose vehicles (SPVs) have also proliferated, allowing successful founders to co-invest alongside institutional funds. These structures democratize access to deal flow and let founders participate in rounds they might otherwise miss. The practical effect is that capital sources have diversified significantly, though the bar for accessing any of them has risen.

Startups that can articulate a clear value proposition and demonstrate early traction now have multiple pathways to funding, even if traditional Series A rounds have contracted. This fragmentation of capital sources means founders must understand which funding mechanism fits their stage and business model.

Where Alternative Capital Sources Actually Help Your Startup

Corporate Venture Arms Offer More Than Money

Corporate venture arms have stopped waiting for Series A rounds to mature. Microsoft, Google, and Amazon now deploy capital directly into early-stage startups that solve specific problems their parent companies face. The advantage extends far beyond the money itself-you gain access to customer relationships, distribution channels, and technical infrastructure that accelerate product development. A startup solving enterprise software problems moves faster with corporate backing because the customer already exists within the parent company. The tradeoff is real: corporate investors expect strategic alignment, which means your product roadmap becomes partially dependent on their business priorities. If you need complete autonomy over your direction, corporate capital carries hidden costs that can constrain your long-term vision.

Founder-Led Syndicates and SPVs Provide Flexible Capital

Successful founders now pool capital alongside institutional VCs, which means you’re not just receiving money-you’re gaining operational insights from people who’ve already built companies. These structures work because they remain flexible. A founder syndicate might invest $50,000 to $500,000 per round without requiring board seats or governance rights, making them ideal for founders who’ve already secured institutional backing but need additional capital to extend runway. The PitchBook-NVCA Venture Monitor shows secondary market activity is rising, which means these founder-led structures now have liquidity mechanisms that didn’t exist five years ago. This shift transforms how founders access capital without surrendering control.

Crypto and Blockchain: High Risk, High Reward

Crypto and blockchain funding remains a high-risk, high-reward channel that most traditional startups should approach cautiously. Unlike corporate venture capital or founder syndicates, crypto investors operate with different risk tolerances and exit timelines. If your startup operates in decentralized finance, blockchain infrastructure, or tokenized assets, crypto capital sources exist-but they come with regulatory uncertainty that can evaporate overnight. The 2025 VC market shows AI capturing the majority of mega-rounds, which means non-AI, non-crypto startups face a genuine capital shortage outside alternative sources.

Venture Debt: The Underutilized Tool

Venture debt remains the most underutilized tool in this environment. Lenders typically require 1.5x to 3x annual recurring revenue, but if you meet that threshold, debt capital costs less than equity and preserves founder control. The shift away from traditional Series A rounds means founders who understand multiple capital sources and pick the right mechanism for their stage will navigate this market far more effectively than those waiting for institutional VCs to return to early-stage investing.

Matching Your Stage to the Right Capital Source

Your practical path forward depends on your stage and metrics. If you’ve hit product-market fit with meaningful revenue, corporate venture arms and founder syndicates are legitimate capital sources that can supplement or replace traditional VC rounds. If you’re pre-revenue or early-stage, focus on reaching traction before approaching any of these sources-they all expect demonstrable progress before deploying capital. Understanding which funding mechanism fits your business model becomes the difference between raising capital efficiently and burning months on dead-end conversations. As geographic diversification reshapes where venture capital actually flows, founders outside San Francisco face entirely different funding dynamics than their Bay Area counterparts.

Where Venture Capital Actually Flows Now

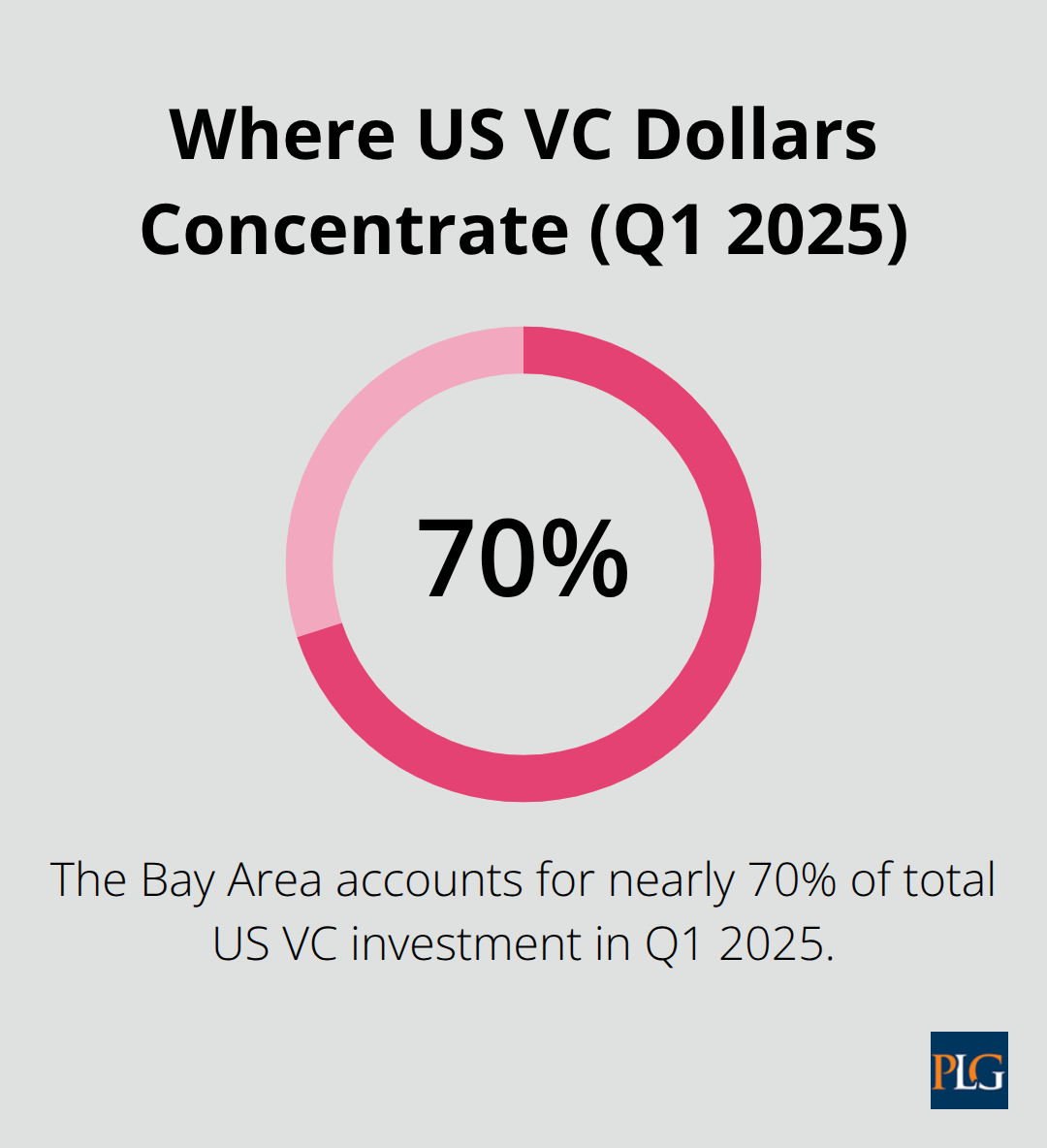

San Francisco still dominates US venture capital, with the Bay Area accounting for nearly 70% of total US VC investment in Q1 2025 according to PitchBook data. This concentration intensifies in AI, where mega-rounds have created a geographic moat around Northern California. However, this dominance masks a critical reality: founders outside San Francisco now access genuine funding pathways that didn’t exist three years ago.

European and Asian tech ecosystems have matured enough to attract institutional capital at scale, and remote work has fundamentally changed how investors evaluate geography. Your location no longer determines your access to capital, but it does determine which capital sources will fund you and on what terms.

Startups in London, Berlin, Singapore, and Toronto now raise institutional rounds without needing a San Francisco presence, though they typically accept lower valuations and longer fundraising timelines than equivalent Bay Area companies. This geographic shift isn’t about equality-it’s about capital efficiency. European investors scrutinize unit economics more rigorously than their American counterparts, which means startups outside the US face higher bars for profitability but access cheaper capital once they clear those hurdles. Asian venture capital, particularly from Singapore and Seoul, has become increasingly focused on deep tech and hardware, sectors where geographic proximity to manufacturing and supply chains matters more than proximity to Sand Hill Road.

Why Remote Investors Now Fund Distributed Teams

Remote work transformed investor behavior more than any regulatory change could have. A venture fund no longer requires quarterly office visits to monitor portfolio companies, which means they can deploy capital into markets where they lack physical presence. This shift enabled emerging fund managers in Austin, Miami, and Toronto to raise institutional capital by proving they could generate returns without relying on Bay Area networks. Your team’s location matters far less than your metrics and market opportunity.

However, this doesn’t mean San Francisco lost its advantage-it means the advantage shifted from location to network. Founders with connections to Sand Hill Road still raise at higher valuations and faster timelines, but founders without those connections can now access capital from regional investors who understand their local markets better than generalist Bay Area VCs. This bifurcation creates a strategic choice: raise from a prestigious Bay Area fund at a lower valuation to gain brand credibility and network access, or raise from a regional investor at a higher valuation but without the same institutional relationships.

For startups in regulated industries like fintech or healthcare, regional investors often bring regulatory relationships and domain knowledge that Bay Area generalists lack entirely. This can accelerate your path to market far more effectively than prestige alone.

Building Your Funding Strategy Across Markets

Your practical approach should match your business model to the capital sources most likely to fund it. If you’re building AI infrastructure or enterprise software, San Francisco capital remains abundant, though you’ll face intense competition and will need either extraordinary metrics or a compelling founder narrative to stand out. If you’re building fintech, biotech, or hardware, regional investors outside San Francisco often move faster and negotiate better terms because they focus on those sectors rather than chasing the next AI mega-round.

Secondary market activity is rising according to the PitchBook-NVCA Venture Monitor, which means earlier employees in distributed startups can now find liquidity without relocating to California. This changes hiring dynamics significantly-you can now recruit senior talent to regional hubs because they know they can eventually exit their equity without waiting for an acquisition or IPO.

Matching Capital Sources to Your Sector

The geographic diversification of venture capital means you should evaluate funding sources by their sector focus rather than their location. A London fintech fund with deep banking relationships will move faster on your Series B than a San Francisco generalist fund, even if the SF fund has more total capital under management. Your fundraising timeline compresses when you target investors who already understand your market and have conviction in your sector.

Founders who match their capital raising strategy to regional investor expertise close rounds faster and on better terms than those chasing prestige alone.

Final Thoughts

The venture capital industry trends reshaping startup funding will not reverse. Mega-rounds concentrate capital into AI companies while Series A rounds contract, forcing founders to reach profitability faster and access alternative funding sources. Geographic diversification means your location matters less than your metrics, but San Francisco still commands premium valuations for companies with the right narrative. Corporate venture arms, founder syndicates, and venture debt now compete alongside traditional VCs, creating multiple pathways to capital for startups that understand which mechanism fits their stage.

This shift demands a fundamental change in how you approach fundraising. Building sustainable unit economics and demonstrating real revenue traction now separates companies that raise capital from those that struggle for months. The two-tiered market is real: companies with strong metrics access cheap debt and equity simultaneously, while earlier-stage companies face higher hurdles. Your practical strategy should match your business model to the capital sources most likely to fund it, whether that’s a San Francisco generalist fund, a regional investor with sector expertise, or a combination of corporate capital and founder syndicates.

Staying informed on these market shifts isn’t optional anymore. Founders who understand current venture capital industry trends close rounds faster and on better terms. At Primum Law Group, we help startups and investors navigate these shifts through tailored legal strategies that align with your funding goals-our team provides venture capital transaction support and startup counseling designed for this new environment.