Startup founders who move across borders face a complex web of tax obligations that most don’t anticipate until it’s too late. US tax residency rules determine whether you owe taxes on worldwide income, and getting this wrong can cost thousands in penalties and back taxes.

At Primum Law Group, we help founders navigate these rules before they become problems. This guide covers the tax residency tests that matter, practical strategies to minimize your tax burden, and the compliance steps you need to take when relocating internationally.

How US Tax Residency Tests Actually Work in San Francisco and Beyond

The US tax system uses two separate tests to determine if you owe taxes on worldwide income: the Green Card Test and the Substantial Presence Test. Understanding which one applies to you is the first step toward controlling your tax liability.

The Green Card Test: Binary and Permanent

If you hold a green card, you’re automatically considered a US tax resident regardless of where you live or how many days you spend in the country. This status persists until you formally abandon it through specific procedures with US Citizenship and Immigration Services. The Green Card Test is binary-you either have one or you don’t-which makes it straightforward but also potentially expensive if you’re not planning an exit strategy.

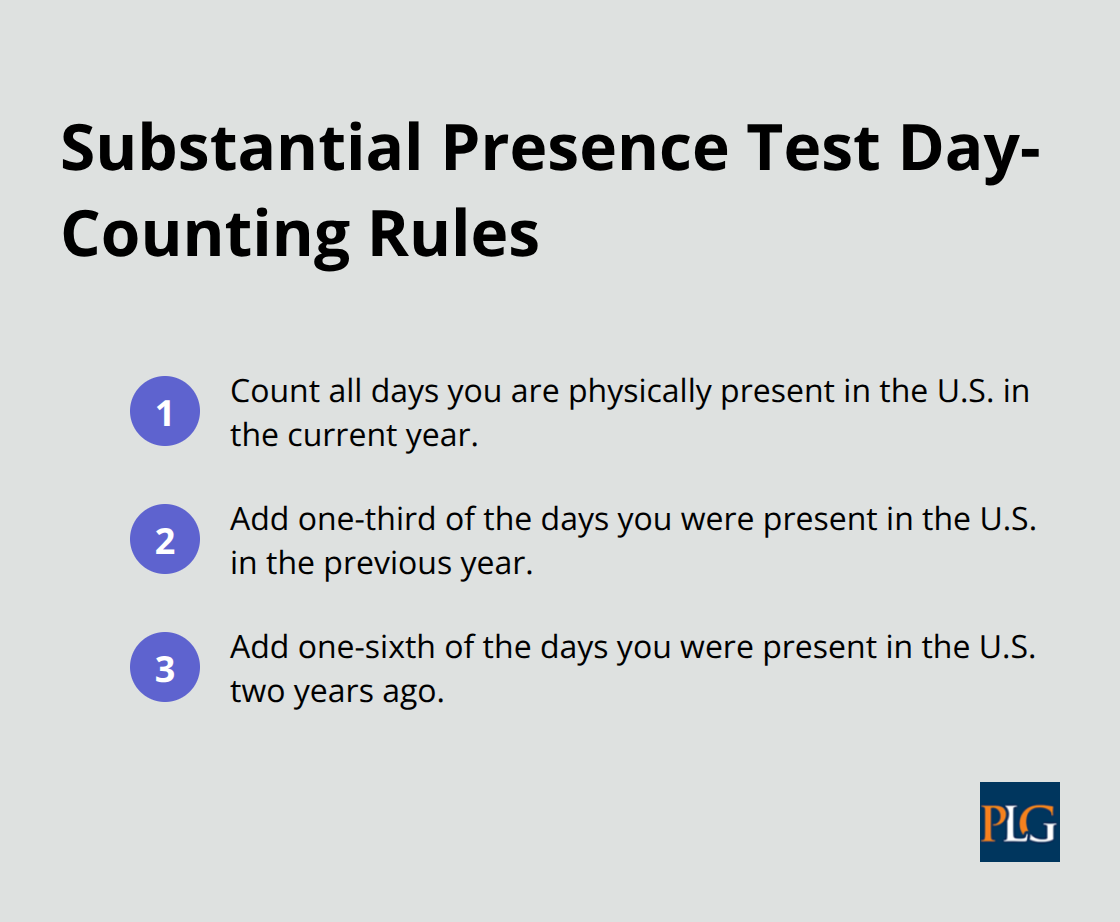

The Substantial Presence Test: A Three-Year Calculation

For founders without a green card, the Substantial Presence Test determines residency based on physical presence in the US over a three-year period using a weighted calculation. According to Treasury Regulations Section 301.7701(b)-3, you count all days in the current year, one-third of days from the previous year, and one-sixth of days from two years ago. If this total reaches 183 days, you’re considered a US tax resident.

The calculation sounds simple until you realize that certain days don’t count at all-brief transit days, medical stays, and days when you lack a US visa all exclude themselves from the count. This means a founder can spend significant time in the US without triggering residency if they structure their travel carefully.

The Closer Connection Exception: Your Escape Route

The Substantial Presence Test has a critical escape valve called the Closer Connection Exception, which allows you to avoid US tax residency even if you meet the 183-day threshold. To qualify, you must maintain a foreign tax home and demonstrate stronger ties to a foreign country than to the US.

Treasury Regulation Section 301.7701(b)-8 requires a three-factor analysis: you must have a permanent home available in the foreign country, your center of vital interests must be there (family, business activities, personal relationships), and your habitual abode must reflect your settled routine in that location. This exception is powerful for founders who maintain genuine foreign residences and can document ongoing ties to another country.

Filing Form 8840 and Proving Your Case

You file Form 8840 with your tax return to claim this exception, and the IRS scrutinizes these filings heavily. Filing the form doesn’t guarantee success-the burden is on you to prove your facts. Founders who claim the exception without proper documentation face audit risk and potential back taxes.

The exception applies only to the Substantial Presence Test, not the Green Card Test, which means it’s worthless if you hold a green card. The IRS examines whether your permanent home is truly available to you, whether family members actually live there, and whether you maintain regular contact with the foreign jurisdiction. A vacation property doesn’t qualify; you need a residence you can actually occupy.

Once you understand which residency test applies to your situation, you can move forward with structuring your compensation and equity to align with your tax status. The next section covers how to minimize your tax burden through strategic planning around equity events and income timing.

How to Structure Equity and Timing to Cut Your Tax Bill

Establish Your Cost Basis Before Any Equity Event

Founders optimizing for tax residency must make two critical moves before any equity event: establish the right cost basis for your shares and time major income recognition around residency changes. The Federal tax code allows you to purchase founder shares at fair market value when you incorporate, which locks in a low basis for Qualified Small Business Stock (QSBS) treatment later. This matters enormously because QSBS under Section 1202 lets you exclude up to the greater of $10 million or 10 times your basis from federal taxation if you hold the stock for five or more years in a C-corporation with gross assets under $50 million. A founder who buys shares at $0.001 per share at formation and sells at $100 per share after five years can exclude the entire gain from federal tax, subject to state law conformity. Compare this to a founder who receives shares as compensation without paying for them: their basis is zero, meaning they cannot use the Section 1202 exclusion as effectively.

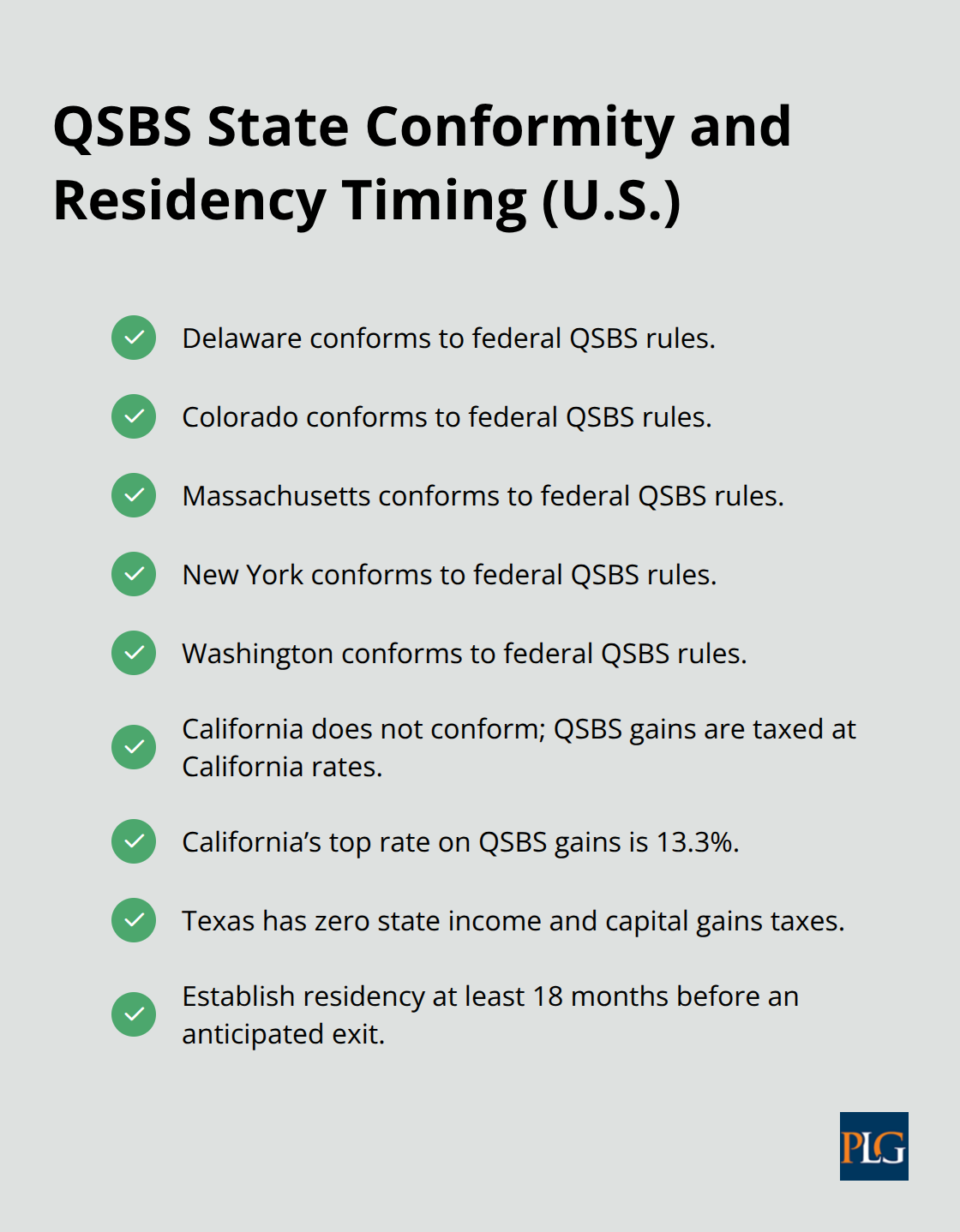

Navigate State-Level QSBS Conformity Rules

State-level QSBS treatment varies dramatically and matters as much as the federal exclusion. Delaware, Colorado, Massachusetts, New York, and Washington currently conform to federal QSBS rules, meaning gains qualify for state-level exclusion. California does not conform, so QSBS gains face California’s top rate of 13.3% even though the federal tax is zero. A California resident with a $10 million QSBS gain owes roughly $1.33 million in state tax alone, while relocating to Texas before the exit eliminates this entirely since Texas has zero state income tax and zero capital gains tax.

The timing window matters: you should establish residency in a tax-friendly state at least 18 months before an anticipated exit to prevent the state from claiming you as a resident at the time of sale.

Leverage the Foreign Earned Income Exclusion for Salary

The Foreign Earned Income Exclusion applies only to wages and self-employment income, not investment gains, so it does not help with equity exits. However, if you draw a salary as a founder and live abroad, you can exclude up to $120,000 of earned income from US federal taxation for 2023 if you meet the Physical Presence Test or the Bona Fide Residence Test under IRC Section 911. This exclusion only applies to US citizens and residents, and state tax treatment varies: some states like California tax worldwide income regardless of the exclusion, while Texas and Florida impose no state income tax at all.

Time Compensation Recognition Around Residency Status

The practical move is to time your salary recognition, bonus payments, and equity vesting around your residency status so that compensation is recognized in years when you qualify for the exclusion or when you are a non-resident. If you anticipate an exit, work backward: identify the target exit date, determine which state offers the best tax outcome, and move your residency there well before the transaction closes. Once you lock in your residency and cost basis strategy, the next step involves understanding how state and federal reporting requirements interact with your new location and what documentation you need to support your tax positions.

Compliance Obligations When Moving Internationally in San Francisco and Beyond

Federal Reporting Requirements for Residency Changes

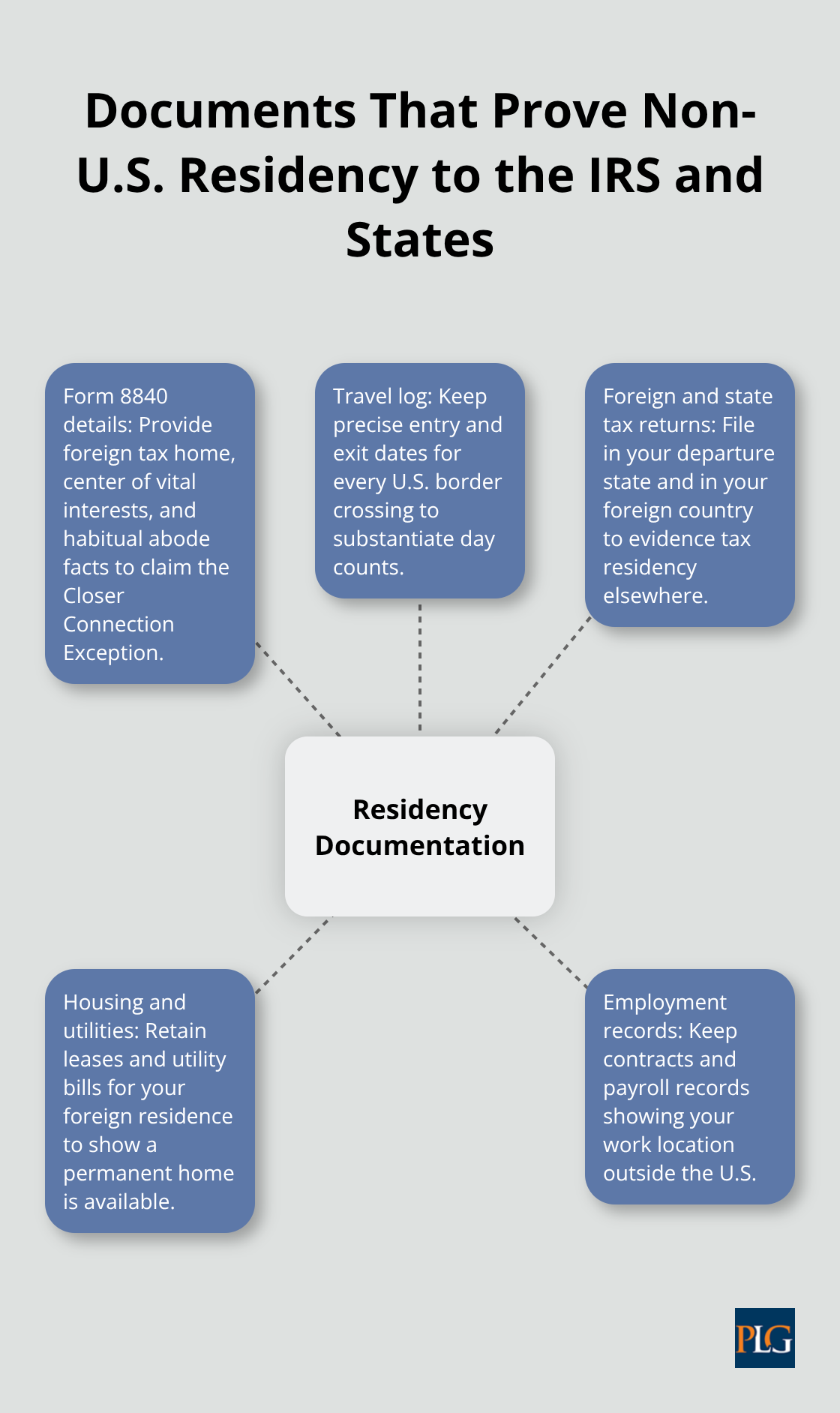

Moving internationally triggers immediate federal filing obligations that most founders underestimate until the IRS or a state tax authority flags them. The moment you change residency, you must file Form 8840 if you claim the Closer Connection Exception, and this form demands detailed documentation of your foreign tax home, your center of vital interests, and your habitual abode. You must attach statements showing where you lived, where your family resides, where your business activities occur, and how you spent your time during the year. The IRS examines these filings at high rates because founders frequently overstate their foreign ties or understate their US connections. If you claim the exception without proper documentation, the IRS will assess back taxes, interest, and accuracy-related penalties of 20 percent on underpaid taxes.

State-Level Reporting and Residency Documentation

State-level reporting obligations multiply the burden significantly. California requires you to file a Residency Questionnaire if you claim non-residency status after previously being a resident, and you must prove your departure with specific evidence: a lease in another country, utility bills, voter registration, and employment records showing you worked outside California. New York applies a convenience-of-employer rule that taxes wages earned anywhere if your employer maintains an office in New York, which means remote work from abroad does not automatically eliminate state tax liability. Texas and Florida impose no state income tax, but you must still file a final return in your departure state claiming non-residency status and supporting it with documentation.

Travel Records and Foreign Tax Documentation

The documentation burden is substantial and requires meticulous record-keeping. You must maintain a detailed travel log showing entry and exit dates for every US border crossing, preserve lease agreements and utility bills from your foreign residence, and keep employment contracts showing your work location. File tax returns in both your US departure state and your foreign country of residence to demonstrate tax residency elsewhere.

The IRS uses these foreign tax returns as proof that you maintained genuine foreign ties and paid taxes there, so filing them strengthens your position if audited.

Coordinating with Tax and Legal Advisors

Working with tax advisors who understand startup-specific residency rules is not optional if you want to avoid costly mistakes. A CPA who understands the Substantial Presence Test calculation can review your travel records before year-end and tell you whether you are at risk of triggering residency, while a tax attorney can help you structure the Closer Connection Exception claim to withstand audit scrutiny. Your advisors should also monitor state tax law changes in real time because states like Washington, Oregon, and California have enacted new capital gains taxes in recent years that affect QSBS planning. Washington imposed a 9.9 percent capital gains tax starting in 2028, and Oregon enacted a 5 percent capital gains tax on gains exceeding $1 million per year effective in 2026, according to state legislative records. These changes alter the calculus of where you should establish residency before an exit, and delaying your planning until after these laws take effect costs you significantly.

Protective Returns and Audit Defense

Your tax CPA should also file protective returns if your residency status remains uncertain, which preserves your right to claim deductions and credits if the IRS later challenges your position. This proactive approach costs less than defending an audit after the fact. Your advisors can coordinate your legal residency planning with your tax positions, ensuring that your equity structure, your compensation timing, and your state residency all align (many founders attempt this coordination alone and end up with conflicting tax positions that invite IRS examination).

Final Thoughts

US tax residency startups face a fundamental choice: plan your residency, equity structure, and compensation timing years in advance, or watch your exit proceeds disappear to state taxes. The founders who retain the most wealth establish their cost basis at incorporation, monitor state tax law changes continuously, and relocate to a tax-friendly state at least 18 months before an anticipated exit. A $10 million QSBS gain costs a California resident roughly $1.33 million in state taxes, while that same founder living in Texas keeps the entire amount-a difference that funds your next venture or leaves you starting over.

The Substantial Presence Test gives you control over your residency if you track your travel carefully and maintain detailed records, and the Closer Connection Exception provides an escape route if you document genuine foreign ties properly. Waiting until you have a term sheet in hand to address these issues is too late; the tax damage is already locked in by that point. Your legal structure, your compensation timing, your equity grants, and your physical location must all align before you approach an exit.

Reach out to Primum Law Group if you’re planning global mobility or anticipating an exit, and we’ll coordinate your strategy across entity structure, tax residency, and compliance obligations. Most founders tackle these moving pieces alone and make costly mistakes that could have been prevented with proper planning.