R&D tax credits for startups can mean the difference between reinvesting thousands back into your business or losing that money to taxes. Most San Francisco founders have no idea how much they’re leaving on the table.

At Primum Law Group, we’ve seen startups claim credits they didn’t know existed-from failed experiments to internal tools built from scratch. The key is knowing what qualifies and documenting it properly from day one.

What the R&D Tax Credit Actually Is

The R&D tax credit is a federal incentive enacted in 1981 and made permanent by the PATH Act in 2015. It lives under IRS Section 41 and works like this: the government reimburses you for qualified research and development expenses through a direct tax credit. This isn’t a deduction that lowers your taxable income-it’s a dollar-for-dollar reduction of what you owe. For San Francisco startups, this distinction matters enormously. A $100,000 deduction might save you $21,000 in taxes. A $100,000 credit saves you the full $100,000.

Federal and State Credit Stacking

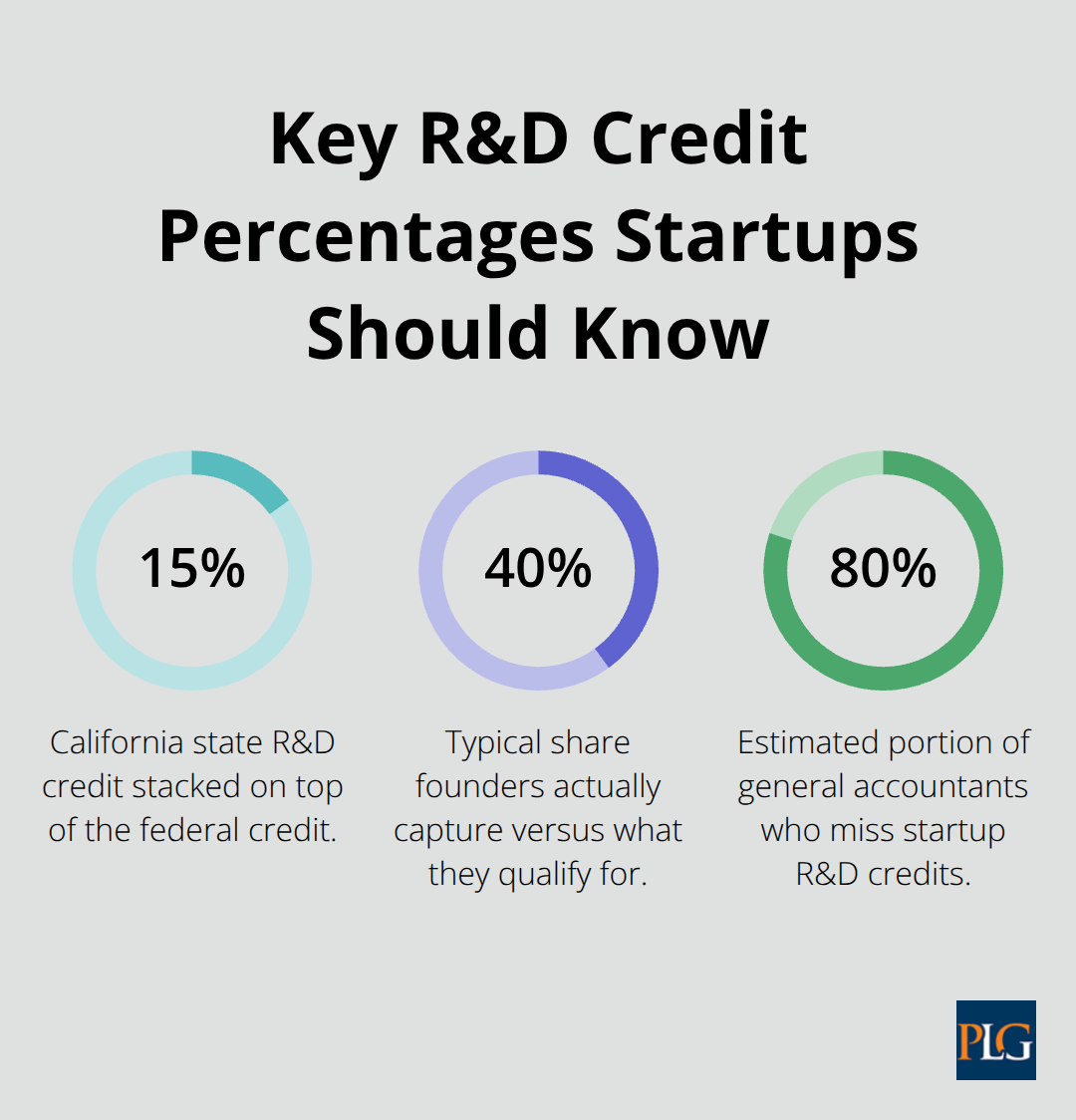

Federal credits typically yield about 5 to 10 cents per dollar of qualified expenses, though California stacks an additional 15% credit on top of the federal credit, pushing combined potential savings higher for qualifying costs. The math gets even better for early-stage companies. If you’re a startup with less than $5 million in gross receipts and you’re within your first five years of operation, you can offset payroll taxes annually through the Qualified Small Business rules. That means instead of waiting to use credits against future income, you get immediate cash back. Pre-revenue startups qualify too-companies burning through development costs before generating revenue can apply credits against payroll taxes immediately, converting research spending into working capital.

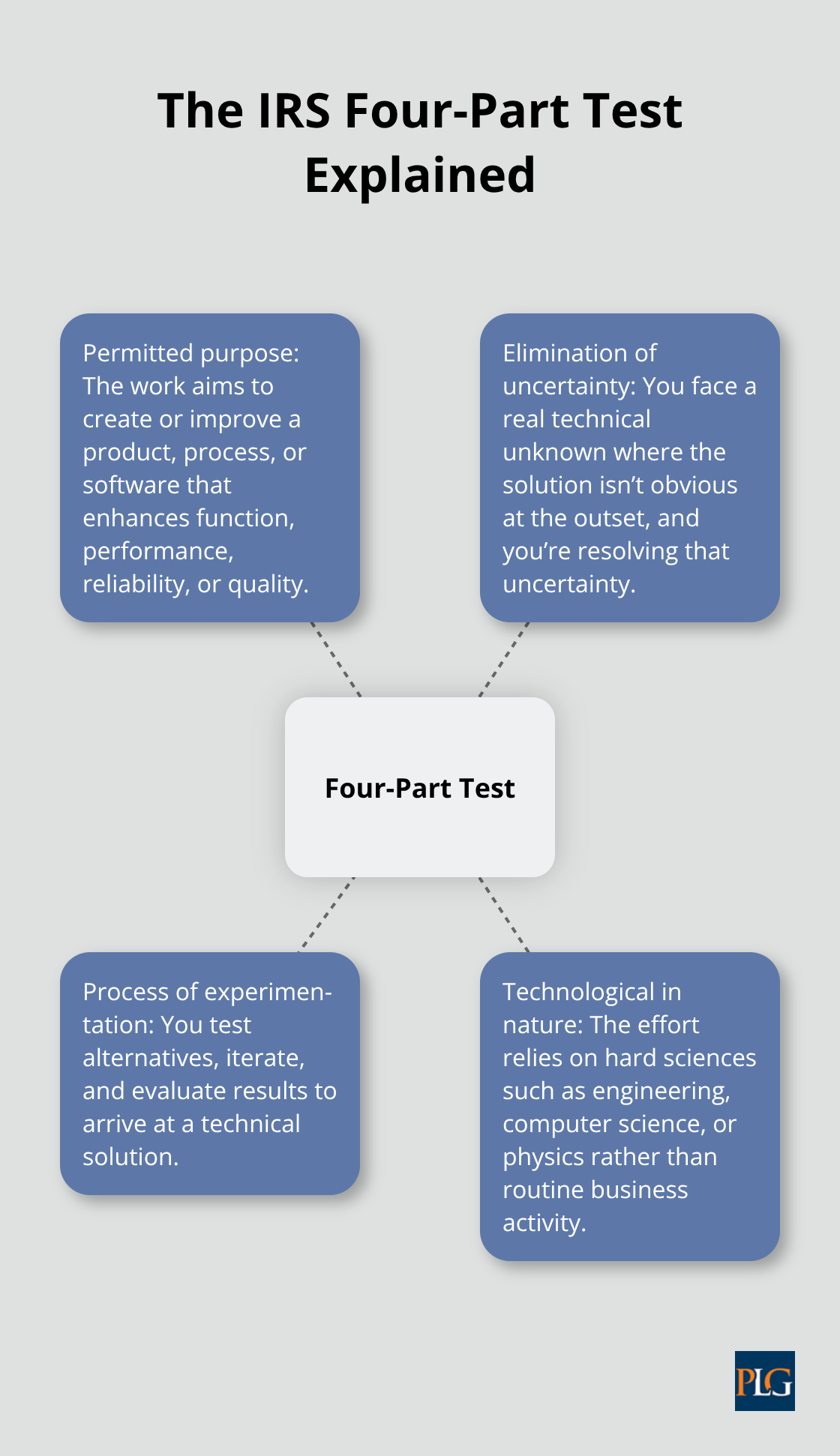

The Four-Part Test for Eligibility

The IRS uses a four-part test to determine eligibility, and the good news is that it applies far more broadly than most founders assume. Your project must have a permitted purpose (creating or improving a product, process, or software), it must eliminate uncertainty (you’re solving a technical problem where the answer isn’t obvious), it must involve a process of experimentation (testing alternatives and iterating), and it must be technological in nature (relying on hard sciences like engineering, computer science, or physics). Software development activities qualify more easily now than ever-interactions with third parties no longer trigger additional qualifying restrictions.

Industries and Activities That Qualify

Hardware startups, biotech companies, manufacturing operations, construction technology firms, and even some fintech companies qualify. Over 60% of eligible small businesses never claim credits because their accountants don’t identify qualifying activities. San Francisco startups typically miss $25,000 to $75,000 per year in pre-Series A stages, jumping to $100,000 to $500,000 annually for Series A and B companies. A digital marketplace startup qualified for over $150,000 in credits-the founders had no idea their innovation efforts qualified until they ran a dedicated analysis.

What Counts as Qualifying Expenses

Wages for technical staff represent 60 to 80% of most R&D credits, but supplies, cloud computing costs, software licenses, and contracted labor count too. The key is that only time spent directly on qualifying activities counts, so a developer spending 70% of their hours on R&D and 30% on maintenance tasks only qualifies for the R&D portion. Understanding how the R&D tax credit works and what qualifies sets the foundation for identifying hidden expenses and strengthening your claim-which is where most startups stumble when they attempt to document their activities.

What Actually Qualifies and What Doesn’t

Software Development and Platform Testing

Software development sits at the heart of most San Francisco startup R&D claims, and the rules have shifted dramatically in your favor. Building new algorithms, developing features that improve functionality or reliability, testing across different platforms like iOS and Android, and automating internal processes all qualify. The National Science Foundation reports that over 60% of eligible small businesses never claim these credits because general accountants miss them entirely. That means your competitor down the street likely leaves $100,000 to $500,000 on the table annually while you could capture it.

Hardware, Manufacturing, and Process Improvements

Hardware startups should track prototyping expenses aggressively-the IRS explicitly recognizes prototyping and iterative testing as qualifying activities. Manufacturing startups can claim process improvements and efficiency upgrades. The mistake most founders make is assuming only moonshot projects count. Failed experiments qualify. Internal tools built from scratch qualify. Code refactoring that improves performance qualifies. The technical uncertainty test is the real gatekeeper: you needed to solve a problem where the answer wasn’t obvious beforehand.

Tracking Experimentation and Research Time

If you spent two weeks researching the best approach before building it, that research period counts. If you tried three different solutions before landing on the right one, all three attempts count as qualifying expenses. This experimentation process-not just the final product-generates the credit.

Documentation Standards That Survive Audits

Documentation failures destroy more R&D claims than ineligible activities ever could. Startups typically lose credits not because they didn’t qualify, but because they can’t prove they qualified. You need contemporaneous records showing what work happened, when it happened, and which employees performed it. Time tracking becomes non-negotiable: developers should log which projects consumed their hours weekly, not retroactively at year-end.

Expense categorization matters enormously. Cloud computing costs, software licenses, contractor payments, and supply expenses only count if you can connect them directly to a specific qualifying project. Create a dedicated R&D folder in your accounting system. Maintain project documentation including technical notes, testing results, design iterations, and even failed prototype versions. One San Francisco hardware startup recovered $340,000 in missed credits simply by correcting their methodology and gathering scattered documentation they’d already created.

The IRS audit process typically reviews three to four years of historical activity, so incomplete records from year one haunt you through year four. Your payroll records and tax filings will be cross-referenced against your project documentation. If a developer’s time records show 80 hours on R&D but your project notes only account for 40 hours, the IRS credits you for 40. Start tracking now, not when you file. Quarterly documentation reviews catch gaps before they become problems. Most general accountants miss startup tax credits entirely-the estimate is around 80%-because they lack the training to identify qualifying activities and lack the rigor to demand proper documentation from clients.

This documentation gap is precisely where working with a firm that understands startup R&D becomes essential.

Turning Hidden Expenses Into Real Savings

Most San Francisco startups leave tens of thousands in unclaimed credits because they only count obvious R&D costs. A developer’s salary gets flagged immediately, but the cloud computing bill buried in your AWS account doesn’t. Contract labor for specific projects gets tracked, but the $15,000 in software licenses purchased to support development work sits invisible. Founders capture 40% of what they actually qualify for because they stop looking too early. The gap between what you claim and what you could claim often runs $50,000 to $200,000 annually, depending on your stage and burn rate. Finding these hidden expenses requires a systematic audit of your spending, not just your payroll records.

Uncovering Invisible R&D Costs

Map every expense category connected to development work. Examine your cloud infrastructure costs monthly-AWS, Google Cloud, Azure, and similar services generate substantial credits when used for qualifying projects. Software licenses for development tools, testing platforms, and infrastructure management count. Contractor payments for technical work qualify if the contractor performed research activities, not just routine implementation. Supplies purchased for prototyping or testing, from electronic components to manufacturing materials, contribute to your base.

One biotech startup recovered $180,000 in manufacturing incentives by reviewing equipment purchases from the prior three years. The expenses already existed in their accounting system; they simply hadn’t connected them to R&D. Review your expense reports from the past four years-the IRS allows you to amend returns and claim retroactive credits within roughly three to four years depending on your situation, meaning missed credits from year one can still reach your bank account today. A Series A company recovered $340,000 in previously unclaimed credits by correcting their methodology and gathering documentation they’d already created but never organized.

Documentation That Withstands IRS Scrutiny

Documentation quality determines whether you keep credits or lose them during an audit. The IRS doesn’t challenge whether your work was innovative or whether it mattered to your business-it challenges whether you can prove it happened and that it qualifies under the four-part test. Weak documentation means the IRS credits you for a fraction of what you actually spent. Strong documentation means you keep everything.

Implement time tracking that happens in real time, not retroactively. A developer should log which project consumed their hours each week, with enough detail to connect hours to specific qualifying activities. When a developer spends four hours on feature development and two hours on maintenance, you document exactly that split. Project management tools like Jira, Asana, or Monday.com create contemporaneous records that auditors respect far more than year-end reconstructions.

Technical notes matter enormously. When your team experiments with different approaches, document that experimentation. Design iterations, failed prototype versions, testing results, and research notes all strengthen your claim by proving the experimentation process happened. One hardware startup’s scattered CAD files, testing photographs, and design iterations recovered $340,000 in missed credits simply because those files proved the work occurred and the methodology was sound.

Year-Round Planning for Maximum Credits

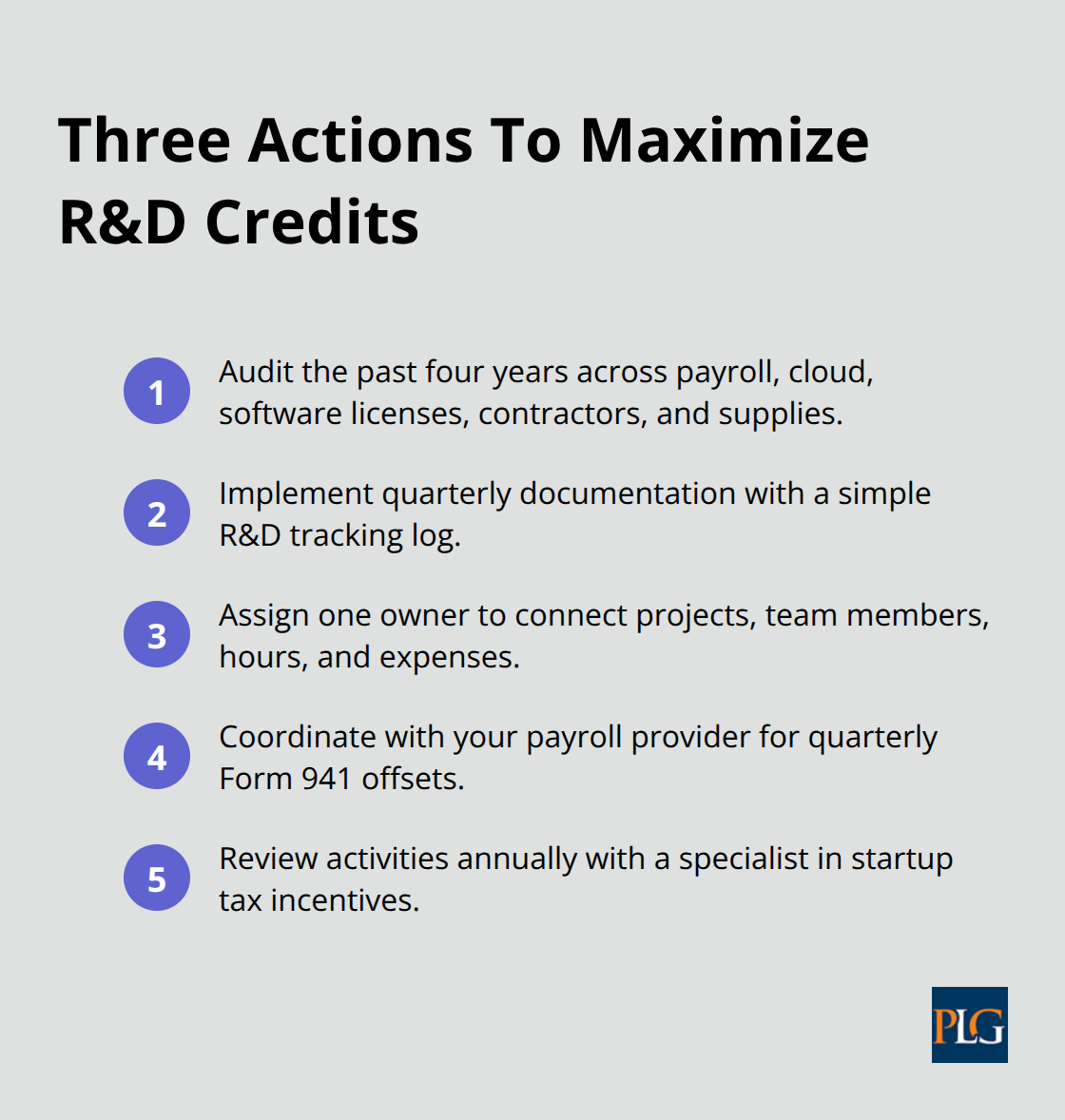

Most startups conduct R&D work consistently but claim credits sporadically, capturing maybe 50% of what they qualify for. Founders who maximize credits treat documentation as an ongoing operational function, not a tax-filing task. Assign one person-often a project manager or operations lead-to maintain a simple R&D tracking log quarterly. This doesn’t require sophisticated software. A spreadsheet documenting which projects qualified, which team members worked on them, how many hours they spent, and which expenses connected to each project creates an audit-ready foundation that takes three hours per quarter to maintain. Without this quarterly discipline, you’ll spend 40 hours reconstructing activity at tax time and still miss pieces.

Coordinate with your payroll provider once you’ve identified your R&D credit opportunity. After the IRS approves your credit, the payroll tax offset applies quarterly to Form 941 filings, meaning you see cash savings throughout the year rather than waiting for a tax refund. This matters enormously for cash flow-a startup with $400,000 in annual R&D credits receives roughly $100,000 in quarterly payroll tax reductions, improving working capital when you need it most. Review your R&D activities annually with someone who understands startup tax incentives, not just general accounting. Most general accountants miss startup credits entirely because they lack the training to identify qualifying activities.

Final Thoughts

R&D tax credits for startups represent real money sitting in your bank account, not theoretical savings. The difference between claiming $50,000 and claiming $300,000 often comes down to whether you tracked expenses systematically or scrambled to reconstruct activity at tax time. San Francisco founders who maximize these credits treat documentation as an operational priority from day one, not an afterthought during tax season.

The path forward requires three concrete actions: audit your spending from the past four years across payroll, cloud infrastructure, software licenses, contractor payments, and supplies (most startups discover $100,000 to $500,000 in previously unclaimed credits simply by reviewing expenses they already recorded), implement quarterly documentation tracking moving forward by assigning one person to maintain a simple log connecting projects, team members, hours, and expenses, and coordinate with your payroll provider once your credits are approved so you receive quarterly cash reductions rather than waiting for a tax refund. The IRS audit process reviews three to four years of historical activity, which means incomplete records from year one compound through year four. Documentation failures destroy more claims than ineligible activities ever could.

We at Primum Law Group help San Francisco startups navigate R&D tax credits alongside broader tax strategy and corporate planning. Contact us to discuss how we can guide you through the documentation requirements, coordinate with your payroll provider, and defend your claims if the IRS questions them. The investment in proper guidance typically returns 200% to 2000% annually when R&D tax credits for startups are captured correctly.