Choosing between venture capital, private equity, and hedge funds shapes your financial future. Each funding source operates differently, with distinct timelines, risk levels, and return expectations that matter for your specific situation.

At Primum Law Group, we’ve guided countless founders and investors through this decision in San Francisco’s competitive funding landscape. This guide breaks down what separates these three options so you can pick the right partner for your goals.

What Sets Venture Capital, Private Equity, and Hedge Funds Apart

Venture capital funds companies at the earliest stages, betting on founders with an idea and a prototype. Private equity buys established businesses with proven cash flows, then applies operational improvements to boost value. Hedge funds trade publicly listed securities and derivatives, moving capital in and out of positions within days or weeks. The three operate in completely different worlds, and mixing them up costs money.

Where the Money Goes and How Fast

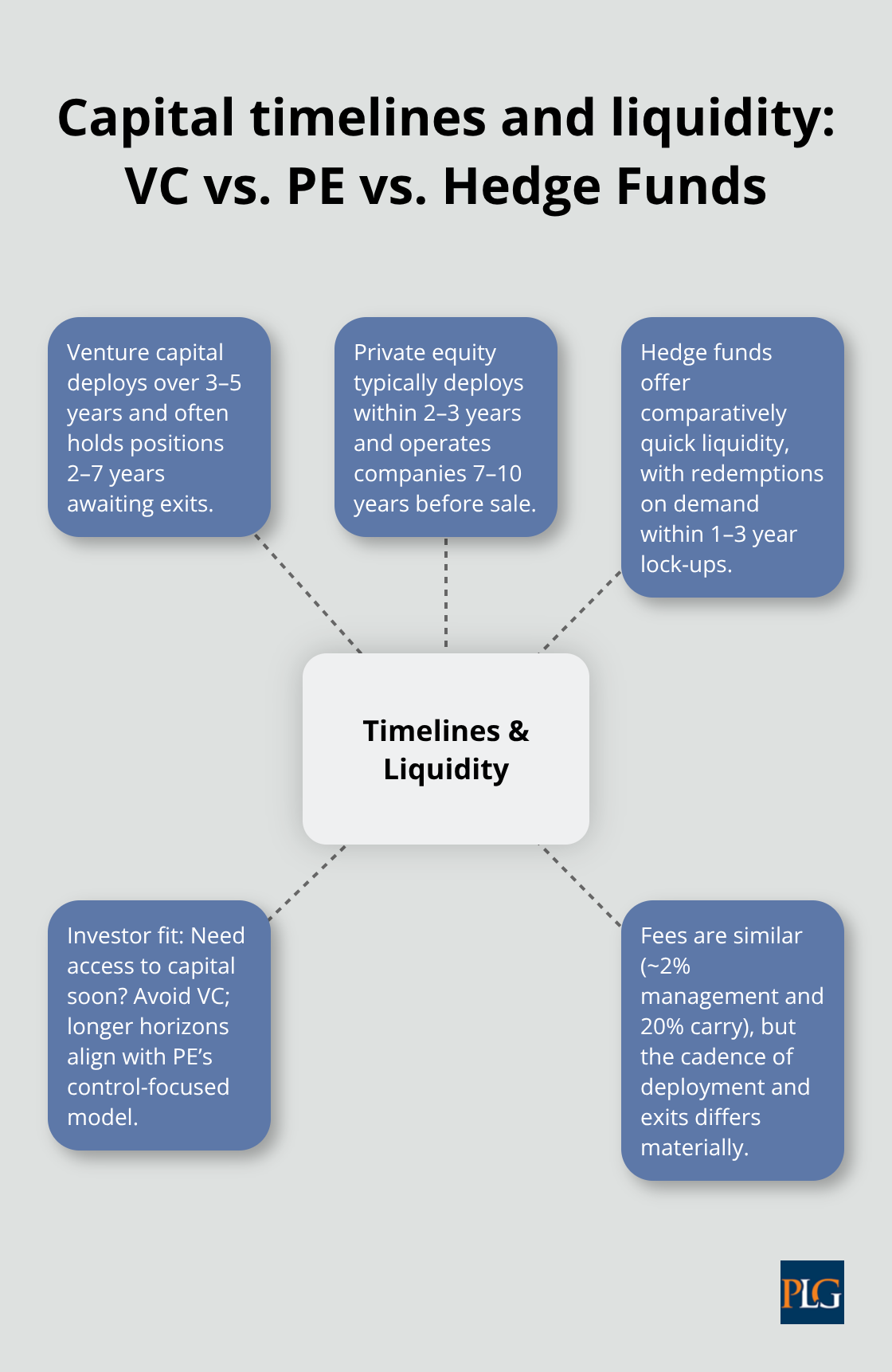

A venture capital firm in the Bay Area typically invests between 5 million and 20 million dollars per round in early-stage startups. The goal is aggressive growth, not immediate profit. According to data from the San Francisco Standard, AI startups captured more than half of all venture capital funding in 2025, with 133 AI company leases signed in San Francisco alone that year-85 of them by early-stage firms. This concentration reflects VC’s willingness to chase transformative technology regardless of current profitability. A private equity firm, by contrast, targets companies generating 10 million to 100 million dollars in annual revenue. PE acquisitions often range from 50 million to several billion dollars, financed partly with debt. Where venture capital accepts 90 percent failure rates for occasional massive wins, private equity demands predictable returns through cost cuts, revenue expansion, and working capital management. Hedge funds operate on a completely different clock. They deploy capital upfront into liquid securities, adjusting positions daily based on market conditions. A hedge fund manager can exit a stock position in hours; a venture capitalist waits five to seven years for a startup exit through acquisition or IPO.

Deployment Speed and Capital Lock-Up

Venture capital and private equity both charge roughly two percent in annual management fees and twenty percent carried interest on profits, but the timing differs radically. A VC fund deploys capital over three to five years, then holds positions for another two to seven years waiting for exits. Private equity deploys faster, often within two to three years, then operates portfolio companies for seven to ten years before selling. Hedge funds collect management fees quarterly or annually and return capital on demand, typically with lock-up periods of one to three years. This matters for your wallet.

If you need capital next month, venture capital is worthless. If you have a ten-year horizon and want operational control, hedge funds waste your time.

Return Targets and Failure Rates

Venture capital targets returns of three to ten times invested capital over five to seven years. That sounds spectacular until you remember most startups fail. Private equity targets two to five times returns over a seven to ten year holding period, with far lower failure rates because the companies already generate cash. Hedge funds try to make money whether markets rise or fall, pursuing what they call absolute returns. Top hedge funds deliver eight to fifteen percent annually; many underperform stock indices. The risk profile separates them cleanly. Venture capital is binary: you win big or lose everything. Private equity is surgical: you buy a company, cut costs, grow revenue, and sell at a premium. Hedge funds are tactical: you exploit market inefficiencies and manage downside through hedging and diversification.

San Francisco’s Current Funding Dynamics

In San Francisco’s market right now, venture capital faces compressed valuations after the 2022 correction, pushing early-stage founders to prove traction before raising Series A. Private equity is quietly acquiring undervalued software and services companies as larger PE firms hunt for platforms to roll up smaller operations. Hedge funds are positioning for anticipated 2026 IPOs from companies like Databricks and Anthropic, which could unlock exits for VC portfolios and create merger opportunities. None of these three strategies work for every investor or every business. The fee structures alone-both charge roughly the same percentage, but hedge funds demand liquidity and quick capital deployment while VC and PE lock your money away-make them fundamentally incompatible for investors with different time horizons. Understanding which vehicle matches your timeline and risk tolerance determines whether you capture value or leave it on the table. The next section walks through how to match your specific situation to the right funding source.

Which Funding Source Matches Your Current Situation

Venture capital is the only choice if your company burns cash to grow and you have no revenue yet. You’re building a product, finding product-market fit, and need capital to hire engineers and designers. VC investors in the Bay Area understand this reality. According to the San Francisco Standard, AI startups received more than half of all venture funding in 2025, and early-stage firms signed 85 of the 133 AI company leases in San Francisco that year. This concentration exists because venture capitalists accept massive failure rates in exchange for occasional 10x or 100x returns.

When Venture Capital Works

If you have a Series A-ready startup with traction-say, 50,000 to 100,000 monthly recurring revenue-venture capital still works. You need 5 to 20 million dollars to scale, and VC firms will back you. But if your company generates 10 million dollars in annual revenue with 30 percent margins and you want to accelerate growth without diluting founders heavily, private equity becomes attractive. PE firms buy profitable companies and apply operational improvements over seven to ten years. They finance deals partly with debt, meaning you put in less equity and keep more ownership.

Private equity rejects unprofitable businesses. If your startup burns 500,000 dollars monthly with no clear path to profitability within 18 months, no PE firm will touch you. Hedge funds are irrelevant for founders and operating company executives. They invest in public securities and derivatives, not private companies. They matter only if you’re an investor with capital already deployed elsewhere and you want liquid, tradeable positions that you can adjust monthly or quarterly.

Revenue and Profitability Determine Your Path

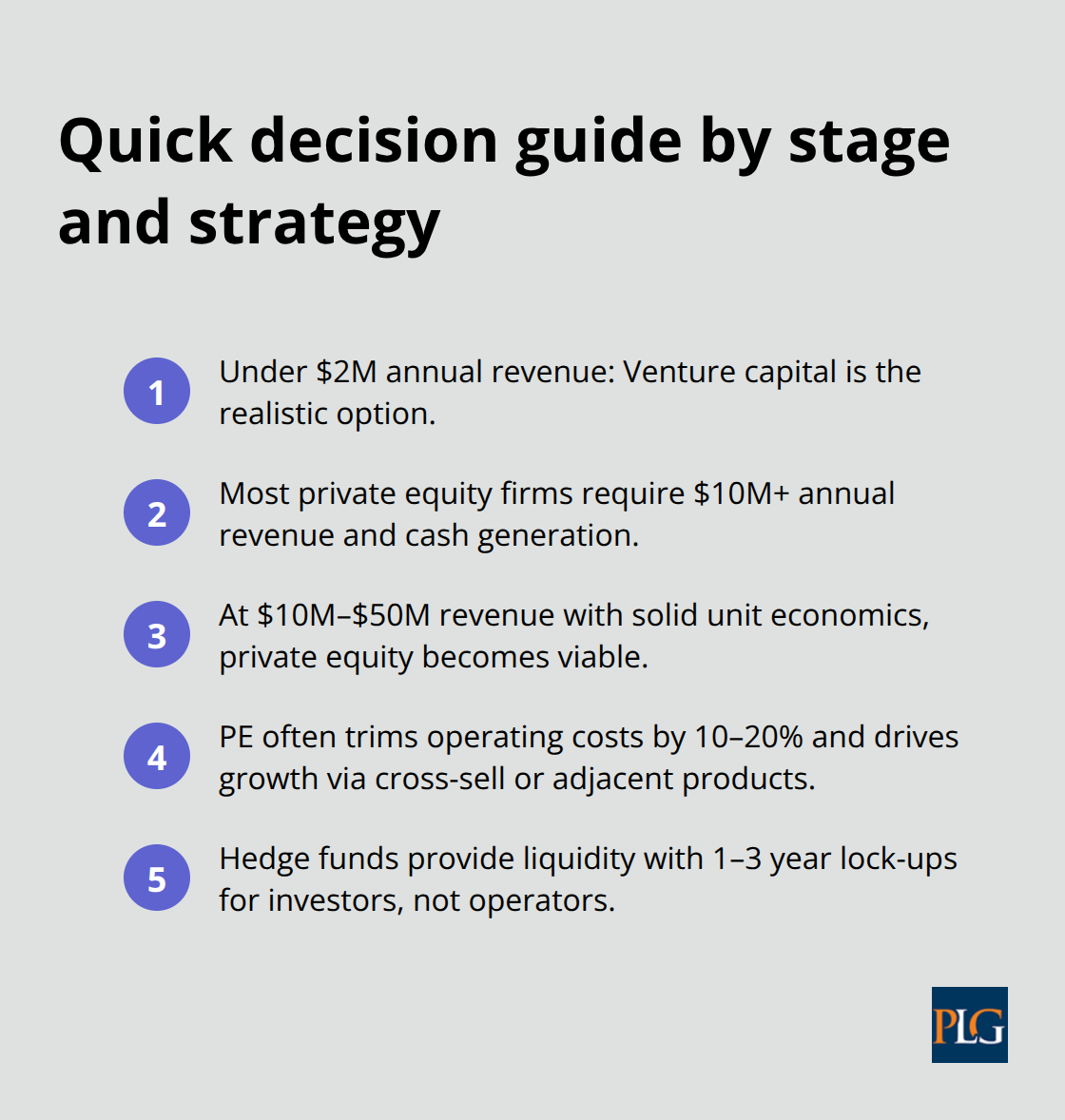

The decision tree is straightforward. If you have less than 2 million dollars in annual revenue, venture capital is your only realistic option. Private equity firms require proven cash generation and most won’t consider companies below 10 million dollars in revenue. If you have 10 to 50 million dollars in annual revenue with positive or near-positive unit economics, private equity becomes viable. PE firms acquire these companies, trim operating costs by 10 to 20 percent through shared services or technology upgrades, and grow revenue through cross-selling or adjacent products.

The San Francisco Standard reported that SF retail vacancy fell to 6.5 percent in 2025 and retail space sales rose 25 percent year-over-year, signaling demand that PE roll-up strategies can exploit in consumer and retail-enabled businesses. If you’re an investor or a fund manager evaluating where to deploy capital, hedge funds offer liquidity and daily pricing that venture capital and private equity cannot match.

Hedge funds don’t require seven to ten year commitments. You can move money in or out within lock-up periods (typically one to three years). But hedge fund returns vary wildly.

Hedge Funds for Investors, Not Operators

Top managers deliver eight to fifteen percent annually; many underperform the stock market. The fee structure-roughly two percent annually plus twenty percent of profits-eats into returns quickly if performance lags. Venture capital and private equity charge similar fees but deliver them over longer periods, so the math works differently. In San Francisco’s current environment, venture capital is compressed. Early-stage founders face higher bars for Series A funding because valuations corrected after 2022. Private equity is actively hunting for platform acquisitions in software and services.

Hedge funds are positioning for 2026 IPOs from companies like Databricks and Anthropic, which will unlock exits for VC portfolios and create merger opportunities. None of these three vehicles fit every situation. Revenue, profitability, and your time horizon determine which one works for you. The next section walks through San Francisco’s funding landscape and shows you where to find capital sources that match your profile.

Finding Capital in San Francisco Right Now

San Francisco’s funding market operates in three distinct geographic and strategic clusters, each with different entry points and decision-making speed. Venture capital concentrates in Menlo Park, Palo Alto, and Mountain View, where firms like Andreessen Horowitz and Sequoia Capital manage thousands of pitch meetings annually. According to the San Francisco Standard, AI startups received more than half of all venture funding in 2025, meaning any founder pitching a non-AI company faces skepticism unless revenue or user growth is exceptional.

The practical reality is brutal: if your startup doesn’t involve artificial intelligence, machine learning, or a clear AI application, you’ll struggle to raise Series A funding from top-tier Bay Area VCs. This concentration exists because venture firms chase the highest potential returns, and AI companies command the largest exit multiples. Early-stage founders should target micro-VCs and sector-focused funds if your company falls outside AI. Flourish Ventures focuses on climate and sustainable investing. 11.2 Capital targets specific verticals. These firms move faster than mega-funds and make decisions in weeks rather than months.

Where Venture Capital Concentrates

The geographic advantage matters significantly. Venture job postings cluster around San Francisco, Menlo Park, Palo Alto, and Mountain View, indicating where capital partners spend time. If you’re raising, schedule meetings in these neighborhoods and plan for multiple trips. Remote pitches work for follow-up meetings, not initial conversations. The concentration reflects how venture firms operate-they build networks in specific geographic hubs and invest heavily in companies within those regions.

How Private Equity Hunts in the Bay Area

Private equity operates differently in the Bay Area. PE firms hunt for software-as-a-service platforms, managed service providers, and business services companies that generate 10 million to 50 million dollars in annual revenue. San Francisco’s office vacancy sits at 34.4 percent overall, but Mission Bay shows strength at under 9 percent vacancy, indicating where established companies still cluster and where PE firms source acquisition targets. Institutional capital rebounded San Francisco real estate in 2025, signaling that PE firms with real estate strategies found opportunities after years of uncertainty.

If you own a profitable services business, PE firms will contact you within months of noticing consistent cash generation. The acquisition process moves faster than venture fundraising because PE firms evaluate companies based on financial metrics rather than growth potential alone. They want predictable cash flows and clear operational improvements they can implement.

Hedge Funds and Secondary Markets

Hedge funds in the Bay Area position for liquidity events. The anticipated 2026 IPOs from Databricks and Anthropic will unlock exits for VC portfolios and create merger opportunities that hedge funds can trade around. Hedge fund managers monitor VC portfolio developments closely because secondary markets for VC stakes have grown liquid. If you hold shares in a VC-backed company approaching Series D or E, hedge funds become acquisition targets for your stake.

The practical move is straightforward: founders should focus entirely on venture capital or private equity depending on revenue stage. Hedge funds matter only after your company reaches significant scale or if you’re an investor with capital to deploy. For legal guidance on structuring your fundraising approach or negotiating term sheets, Primum Law Group provides counsel tailored to San Francisco’s funding landscape.

Final Thoughts

Choosing between venture capital vs private equity vs hedge funds comes down to three concrete factors: your revenue stage, profitability, and time horizon. Founders with minimal revenue should pursue venture capital, while operators running profitable businesses generating 10 million dollars or more annually find private equity more attractive because PE firms finance deals with debt and preserve your ownership. Investors seeking liquid positions that you can adjust quarterly or monthly turn to hedge funds for flexibility that venture and private equity cannot offer.

San Francisco’s funding landscape rewards founders and investors who know their numbers. Venture firms concentrate in Menlo Park, Palo Alto, and Mountain View, hunting for AI-driven startups and high-growth companies, while private equity quietly acquires profitable software and services businesses by moving faster than venture because financial metrics drive decisions. Hedge funds position for liquidity events and secondary market opportunities as VC portfolios mature toward exits, creating additional pathways for capital deployment.

Your next step depends on where you sit in this landscape. Founders should prepare pitch materials and financial projections tailored to your revenue stage, then target the appropriate capital source, while investors should clarify your time horizon and risk tolerance before committing capital to any vehicle. For legal guidance structuring your fundraising approach, negotiating term sheets, or understanding the implications of different capital sources, Primum Law Group provides counsel tailored to San Francisco’s funding landscape and handles the transactions that matter to your success.