Picking the right law firm corporate structure shapes everything from your tax bill to your liability exposure. At Primum Law Group, we’ve seen how the wrong choice can cost firms thousands annually, while the right one protects assets and streamlines operations.

San Francisco law firms face unique pressures-high operating costs, strict regulatory requirements, and intense competition for talent. This guide walks you through the structures that work, the trade-offs you’ll face, and how to make the decision that fits your firm’s goals.

California’s Two Structural Choices for Law Firms

The Limited Liability Partnership Structure

California law restricts law firms to just two entity types: the Limited Liability Partnership (LLP) and the Professional Corporation (PC). This constraint eliminates theoretical debate and forces a practical comparison based on liability, cost, and governance. The choice between these two structures determines who bears financial risk, how much you pay annually to the state, and who holds decision-making authority.

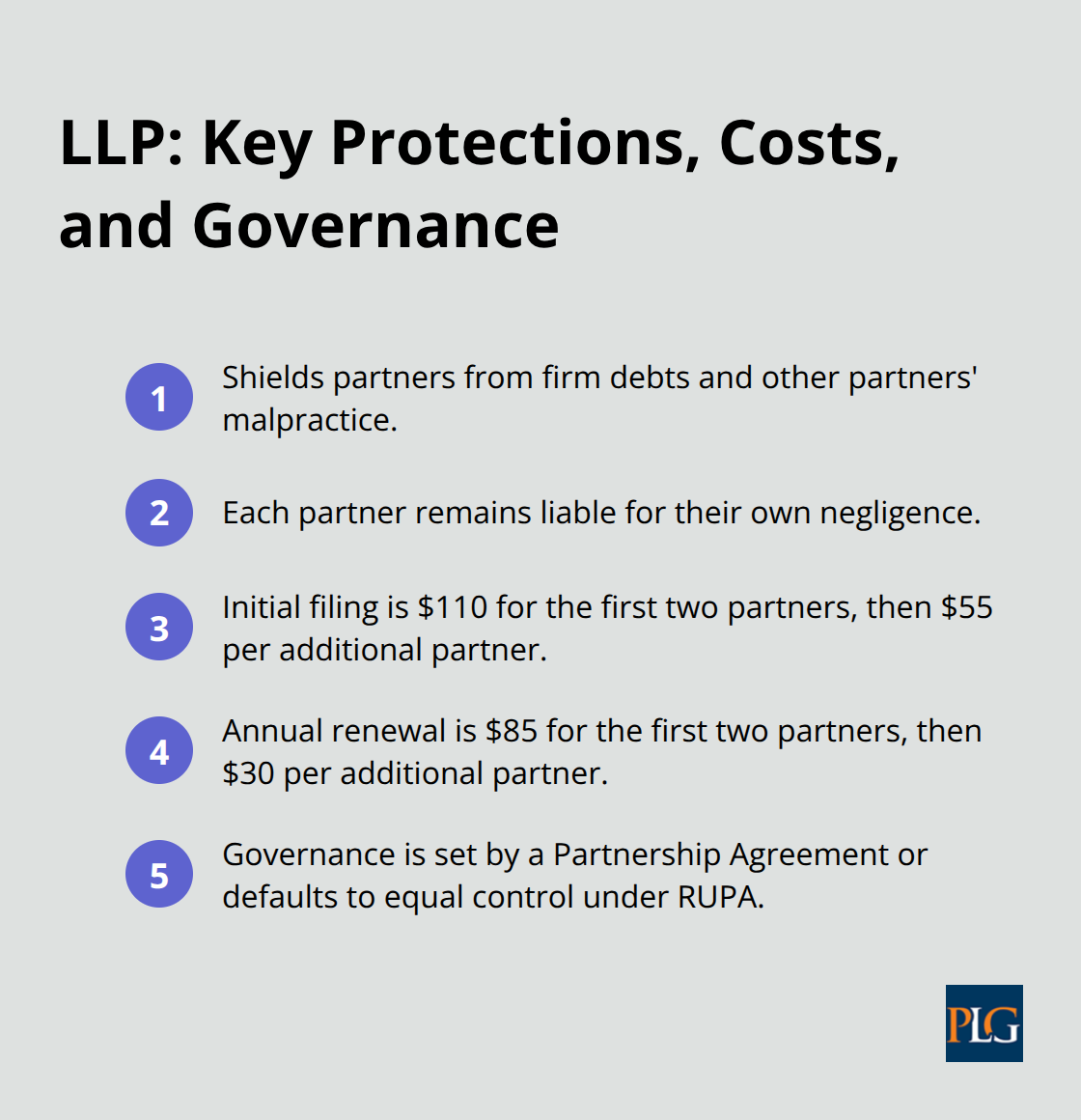

The Limited Liability Partnership shields partners from personal liability for firm debts and other partners’ malpractice, though partners remain personally liable for their own negligence. Formation costs $110 for the first two partners and $55 for each additional partner, with annual renewal fees of $85 for the first two and $30 per additional partner. Governance flows through a Partnership Agreement that defines rights, profit splits, and management roles; without one, California’s Revised Uniform Partnership Act grants equal control to all partners regardless of seniority or contribution.

Cost Advantages as Your Firm Grows

An LLP scales affordably as your firm grows. A ten-partner LLP pays roughly $340 annually in state fees compared to a Professional Corporation’s fixed $100 renewal. This structure works well for established practices with stable partner groups because the per-partner fee structure rewards growth and the partnership agreement provides flexibility to adjust voting rights and profit distribution without triggering corporate formalities.

The Professional Corporation Model

The Professional Corporation operates like a traditional business corporation with a Board of Directors appointing officers to manage operations. Initial application costs $250 with a $100 annual renewal fee, making it cheaper than an LLP for firms with two or three lawyers but increasingly expensive relative to LLP costs as headcount rises. The PC shields shareholders from corporate debts but exposes the corporation itself to malpractice liability, potentially affecting share value if a lawyer commits negligence.

Governance requires formal board meetings and minutes, which creates administrative overhead but also enforces structured decision-making. Solo practitioners often choose the PC for simplicity and lower ongoing costs, while growing partnerships gravitate toward LLPs because the per-partner fee structure remains manageable and the partnership agreement provides the flexibility that scaling practices demand.

Ownership Restrictions and Outside Capital

Neither structure allows non-lawyer ownership-California’s Rules of Professional Conduct prohibit this entirely, a stricter position than states like Washington and Arizona that permit non-lawyer investment. This restriction protects lawyer independence and client confidentiality but means outside capital must come through debt financing or equity arrangements that preserve lawyer control. Understanding these ownership limits shapes how you fund growth and structure future partnerships.

What Actually Moves the Needle When Choosing Your Structure

Tax Treatment Creates Long-Term Financial Consequences

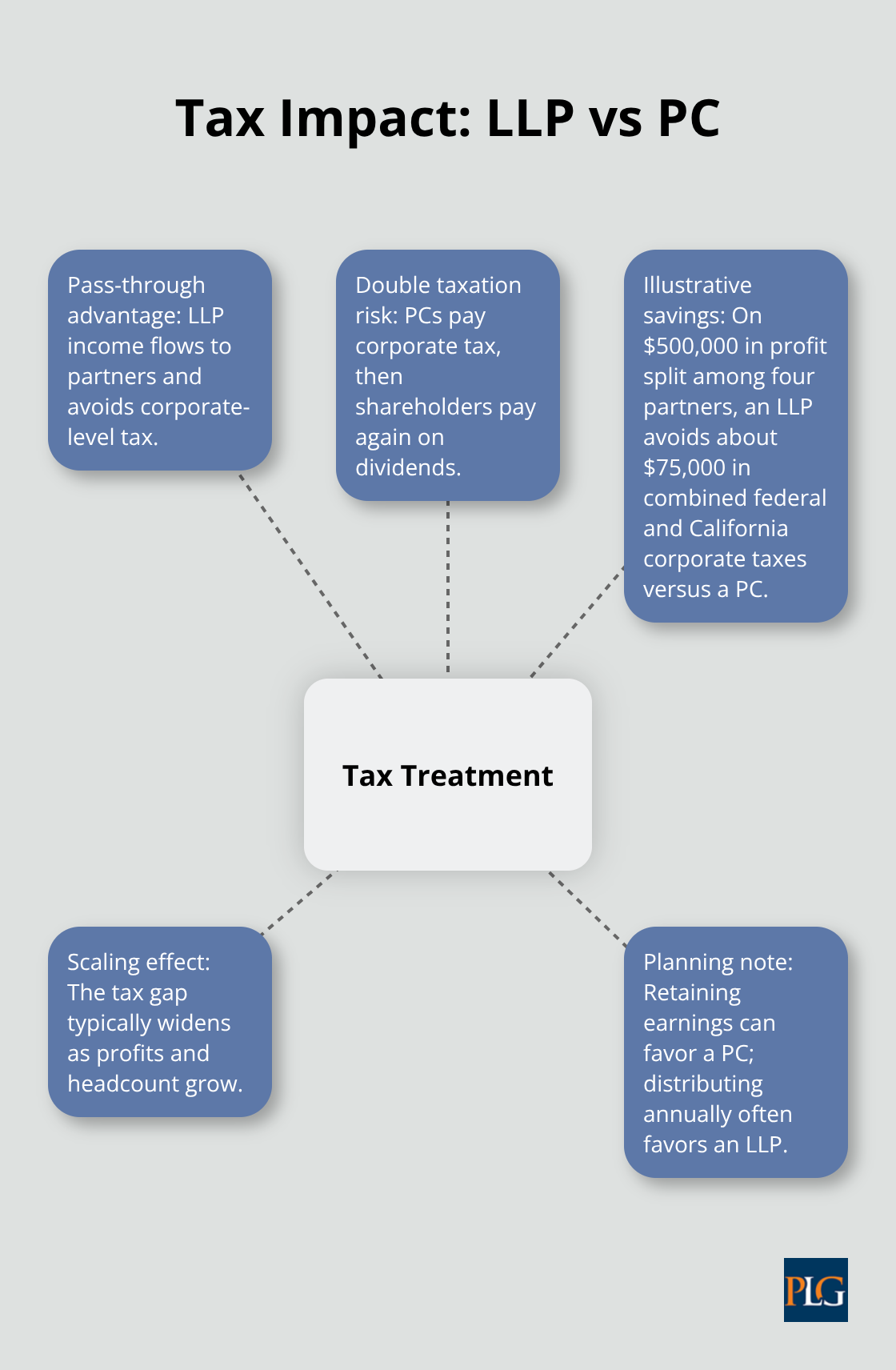

Tax treatment differs sharply between an LLP and a PC, and this difference compounds over years. An LLP operates as a partnership by default, meaning partners report their share of firm income on individual returns and avoid the double taxation that corporations face. A PC, structured as a corporation, pays corporate income tax on profits, then shareholders pay again when dividends are distributed. For a San Francisco firm generating $500,000 in annual profit split among four partners, the LLP structure avoids roughly $75,000 in combined federal and California corporate taxes compared to a PC. This advantage widens as the firm scales.

However, a PC offers more flexibility for retained earnings and can be taxed as an S-corporation under certain conditions, which some solo practitioners use to reduce self-employment taxes. The right choice hinges on whether your firm reinvests profits or distributes them immediately. If you retain earnings to build reserves or fund technology, the PC’s ability to hold cash at the corporate level appeals to some practices. If you distribute profits annually, the LLP’s pass-through structure saves money. Work with a tax accountant familiar with law firm economics before deciding, because the wrong choice locks you into annual compliance costs and limits your flexibility later.

Liability Exposure and Personal Protection Differ Fundamentally

Liability exposure and governance authority pull in opposite directions. An LLP partner protects personal assets from firm debts and malpractice claims from other partners, though that partner remains personally liable if their own work causes injury. A PC shareholder enjoys the same shield, but the corporation itself absorbs malpractice liability, which can erode share value if a claim depletes firm assets. The operational difference matters more than most firms realize.

An LLP requires a Partnership Agreement that must be negotiated and updated as partners join or leave, creating friction during growth but enforcing clarity about who decides what. A PC operates under bylaws and board resolutions, which feel formal but allow the board to delegate day-to-day authority to officers without renegotiating ownership terms. For a firm planning rapid growth from three to eight attorneys, the PC’s governance structure prevents constant partner meetings and renegotiation.

Governance Structure Shapes Growth and Talent Retention

For a stable, smaller practice, the LLP’s flexibility in profit distribution and partner exit terms often outweighs the administrative burden. San Francisco firms competing for talent increasingly need to offer equity to junior lawyers, and both structures support this through partnership tracks or stock options, but the mechanics differ. An LLP requires amending the Partnership Agreement; a PC simply issues new shares.

The governance choice cascades into hiring, retention, and succession planning, so choose based on your growth trajectory, not just current state. A firm that plans to add partners within two years faces different pressures than one that remains stable at five attorneys. The structure you select today determines how easily you can bring in new equity holders, how quickly you can adjust profit splits, and whether governance changes require full partner consensus or board approval alone. These operational realities shape your ability to attract and retain the lawyers who drive your firm’s growth and reputation in a competitive market like San Francisco.

San Francisco’s Structural Reality for Growing Firms

Client Trust Accounts and Regulatory Compliance

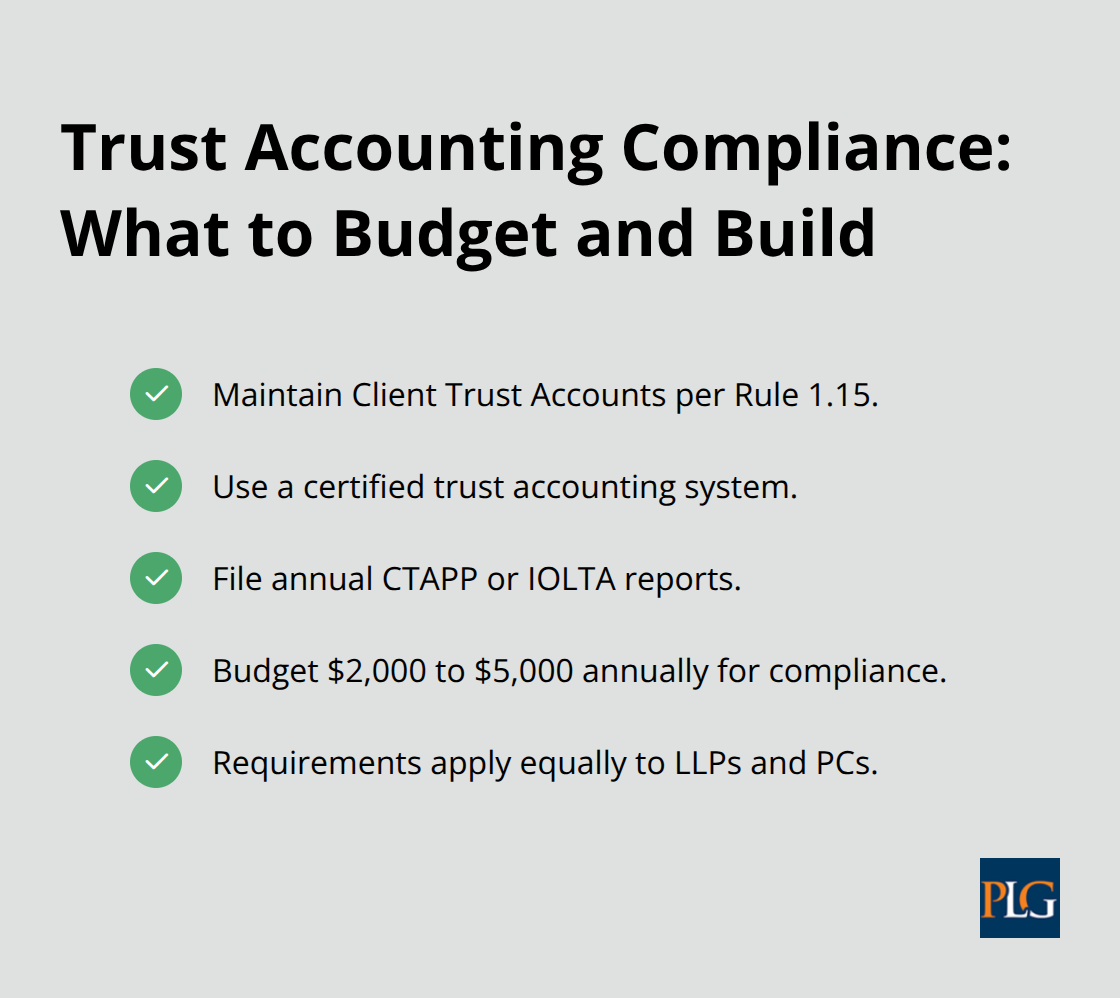

San Francisco law firms operate under California’s strict regulatory framework, which eliminates the flexibility that firms in other states enjoy. The State Bar requires all firms to maintain Client Trust Accounts under Rule 1.15, meaning your chosen structure must accommodate dedicated fund segregation and audit compliance from day one. An LLP or PC that handles client money needs a certified trust accounting system and annual reporting through CTAPP or IOLTA, adding roughly $2,000 to $5,000 annually in compliance costs.

This regulatory overhead applies equally to both structures, so the choice between LLP and PC doesn’t reduce compliance burden-it only shifts who bears liability when trust account violations occur. Firms that underestimate this cost during structure selection often scramble to retrofit their accounting systems later, wasting thousands on remedial work.

Growth Trajectories and Partnership Flexibility

The Bay Area legal market pressures firms toward rapid growth, which tilts the decision toward LLPs for any practice planning to add partners within three years. Thomson Reuters research on legal department structures found that firms growing from five to twelve attorneys face scaling challenges around governance and decision-making authority. An LLP’s partnership agreement allows you to adjust profit splits and voting rights without shareholder consent, while a PC requires board approval and stock issuance paperwork. For San Francisco firms competing for junior talent in a market where salaries exceed $200,000 for mid-level associates, the ability to offer equity quickly matters. A firm that can onboard a new partner with a partnership agreement amendment in two weeks beats one that needs board meetings and stock certificates. Cost efficiency compounds this advantage-a ten-attorney LLP pays $340 annually in state fees versus a PC’s $100, but the flexibility to add partners without renegotiating corporate structure saves thousands in administrative time and legal drafting.

Client Service Models and Compensation Structures

Client service models in San Francisco increasingly demand flat fees and alternative billing arrangements, which both structures support equally. However, the governance speed of an LLP lets you adjust fee arrangements and partner compensation faster when client demands shift, a critical advantage in a market where client expectations change quarterly. Firms that remain rigid on compensation structures lose talent to competitors offering faster adjustments. The practical reality is this: San Francisco’s regulatory requirements, competitive talent market, and fast-moving client base favor structures that prioritize speed and flexibility over administrative simplicity.

Final Thoughts

The law firm corporate structure you select today determines your tax burden, liability exposure, and operational flexibility for years to come. California’s restriction to LLPs and Professional Corporations eliminates guesswork, but the choice between them hinges on factors unique to your practice. An LLP favors growing firms that need governance speed and per-partner cost efficiency; a PC suits solo practitioners or stable small practices seeking administrative simplicity.

San Francisco’s competitive market, regulatory demands, and rapid growth expectations push most expanding firms toward the LLP structure. The ability to adjust partner compensation and profit splits without board approval matters when you compete for talent against larger firms offering equity quickly. Tax treatment compounds this advantage over time-a partnership structure avoids double taxation that erodes PC profits annually, while the right law firm corporate structure supports your vision rather than constraining it.

Consult with a tax accountant familiar with law firm economics and review your growth projections with a lawyer who understands California’s regulatory framework before finalizing your decision. These conversations cost far less than correcting a misaligned structure later. We at Primum Law Group work with startups and growing practices to navigate these structural decisions as part of our broader corporate governance and compliance services.