Founders often treat equity vesting as an afterthought, then face costly disputes when milestones aren’t clearly defined. Getting equity vesting milestones right from the start protects both your company and your team’s long-term commitment.

At Primum Law Group, we’ve seen how the right vesting structure keeps founders aligned through growth phases and funding rounds. This guide walks you through the mechanics that actually work.

Why Vesting Actually Stops Founders From Walking Away

Equity vesting is not just a legal box to check. It’s the mechanism that keeps founders committed when the company hits rough patches, funding rounds stretch timelines, and pivots demand sacrifice. Without proper vesting structure, you risk losing key people exactly when you need them most, or worse, watching unvested equity create resentment that poisons your team’s culture.

The Four-Year Standard Works Because It Demands Real Commitment

The market standard four-year vesting schedule with a one-year cliff works because it forces real commitment. During year one, founders earn nothing if they leave, which filters out those who aren’t serious. After the cliff, monthly vesting over the next three years means roughly 2.08% of shares unlock each month. This structure protects your company from the free rider problem: someone who joins, takes a paycheck, and vanishes after six months shouldn’t walk away with substantial equity. At the same time, it rewards founders who stay through the hard early years when salaries are low and outcomes are uncertain.

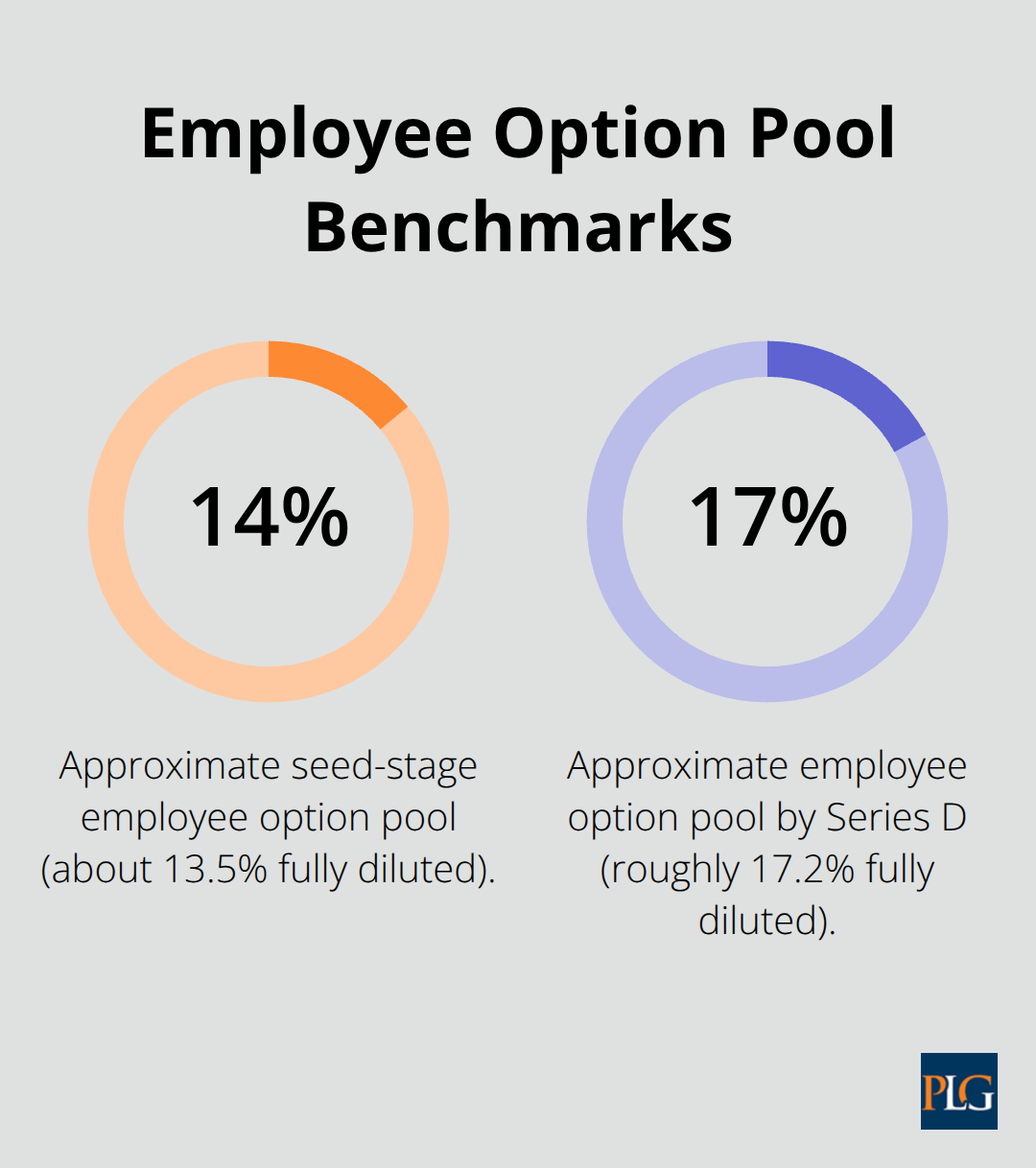

Seed-stage startups typically reserve about 13.5% of fully diluted shares in the employee option pool, which grows to roughly 17.2% by Series D. This growing pool reflects the reality that your ability to attract talent depends on competitive equity grants, but those grants must vest over time to maintain alignment.

How Termination Events Protect Your Cap Table

Termination without cause stops future vesting immediately. Vested shares stay with the founder, but unvested shares return to the company or are repurchased at a price typically set at the lower of cost or fair market value. This matters enormously during transitions. If a co-founder leaves mid-way through a funding round or just before acquisition, the company retains control of that unvested equity, preventing disputes and keeping your cap table clean for investors.

Double-trigger acceleration, where unvested equity vests only if both an acquisition occurs and the founder is terminated without cause within a set period, became standard practice precisely because single-trigger acceleration created perverse incentives. Under single-trigger terms, founders could negotiate their own exit right after a deal closes, taking full equity payouts regardless of whether they stayed to execute the integration. Double-trigger aligns incentives: if you stick around post-acquisition, you keep earning your equity.

The Section 83(b) Election Window You Cannot Miss

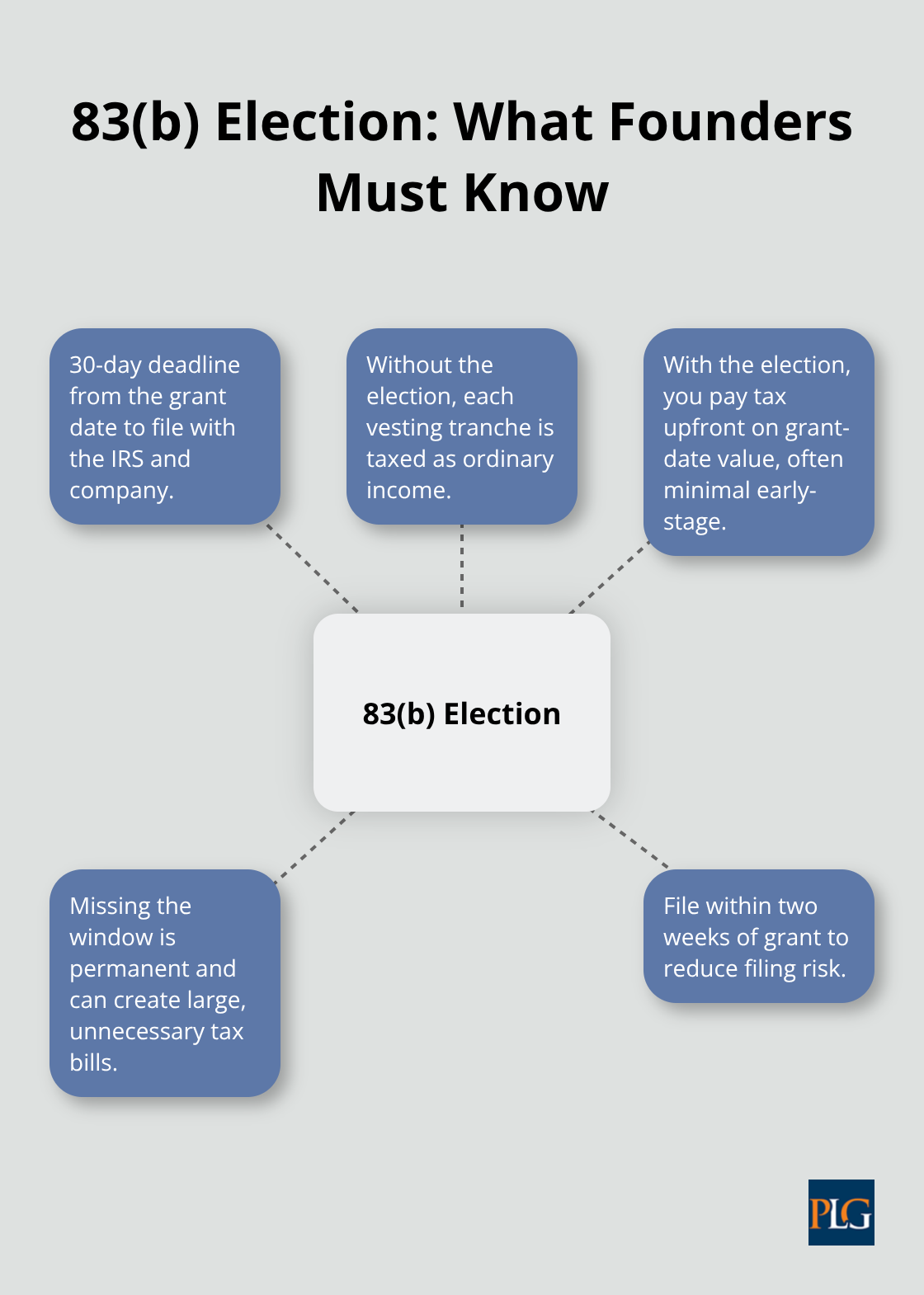

Filing a Section 83(b) election within 30 days of receiving restricted stock fundamentally changes your tax burden. Without it, you pay ordinary income tax as shares vest each month or quarter, potentially locking you into substantial tax bills in years when your company hasn’t generated liquidity. With the election, you pay tax upfront on the grant-date value, which for early-stage companies is minimal. Missing the 30-day window closes this option permanently and can cost you tens of thousands of dollars in unnecessary taxes.

Additionally, Qualified Small Business Stock under Section 1202 offers substantial capital gains tax advantages if you hold shares long enough and meet specific requirements. Vesting terms and separation agreements directly impact QSBS eligibility, so preserving this benefit during funding rounds or founder transitions is non-negotiable. Your vesting structure and tax strategy must work together, not against each other-which is why the next section covers how to avoid the most common mistakes that derail both.

Building Vesting Schedules That Protect Founders and Companies

The Four-Year Standard and When to Break It

The four-year vesting schedule with a one-year cliff dominates startup equity for good reason: it works. Under this structure, 25% of your equity vests at the one-year mark, then the remaining 75% vests monthly over the next three years, roughly 2.08% per month. This isn’t arbitrary. The one-year cliff filters out founders who lack genuine commitment, while monthly vesting after the cliff creates steady alignment as your company moves through growth phases.

Life sciences and biotech companies often extend this to five or six years because their development cycles demand different incentives. FDA milestones and long clinical timelines mean that a standard four-year schedule creates misalignment: founders could fully vest before the company reaches critical inflection points. If your startup operates in biotech or faces similar long-cycle development, negotiate vesting that mirrors your actual business milestones rather than forcing founders into a template that doesn’t fit.

Acceleration Triggers: Single vs. Double

The real protection emerges when you pair time-based vesting with acceleration triggers that respond to company events. Double-trigger acceleration-where unvested equity vests only if an acquisition closes and you’re terminated without cause within a specified period afterward-prevents founders from leaving the moment a deal closes and abandoning execution. Single-trigger acceleration, where all equity vests immediately upon acquisition, creates the opposite problem: founders have no incentive to stay through integration, and buyers often demand founder lockup agreements to compensate.

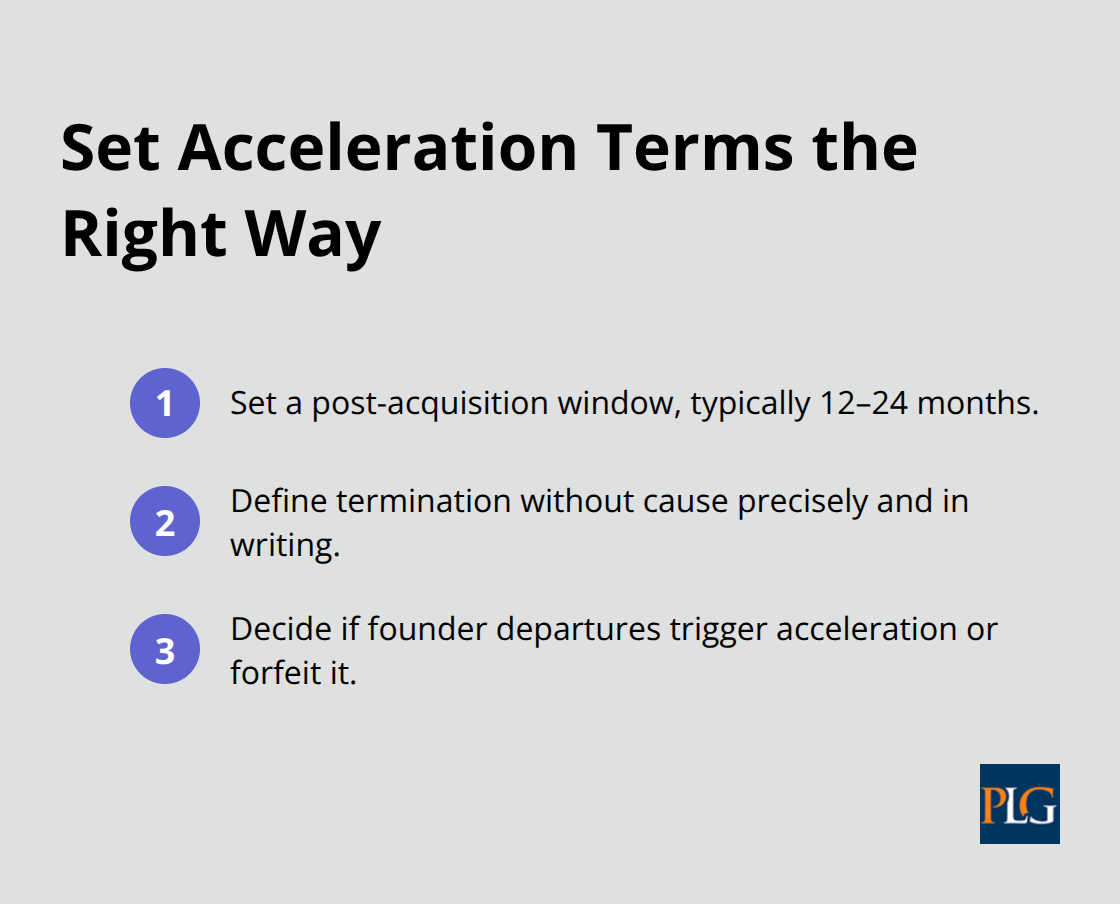

Define your acceleration carefully now: specify the post-acquisition window (typically 12 to 24 months), clarify what termination without cause means, and decide whether departing founders trigger acceleration or lose it. These decisions shape founder behavior during your company’s most critical transitions.

Custom Schedules for Different Roles

Your Chief Technology Officer who wrote foundational code may deserve retroactive vesting credit for pre-incorporation work under a four-year schedule, while a VP of Sales hired later might vest over two years as their role becomes less existential to the company’s survival. Advisors typically vest over two years, reflecting shorter engagement windows.

The mistake founders make is assuming everyone vests identically. Tie vesting length to actual role tenure and impact, not uniformity, and your cap table stays clean through multiple funding rounds. This flexibility in structuring vesting across your team sets the stage for how you’ll handle the inevitable disputes that arise when milestones aren’t clearly defined-which is exactly what the next section addresses.

Common Vesting Pitfalls and How to Avoid Them

Milestone Definitions That Actually Mean Something

Vesting disputes rarely emerge from the legal documents themselves. They emerge from the gap between what was written and what founders actually understood would happen. The most destructive disputes involve milestone-based vesting with no clear definition of what “milestone achieved” means. A founder believes hitting product-market fit triggers acceleration; the board interprets it as reaching $1 million ARR. Neither party acted in bad faith, but the company now faces litigation over equity worth millions.

The solution is ruthless specificity. If your vesting depends on milestones, define them in measurable, objective terms: FDA approval for a specific indication, not clinical progress; $2 million in annual recurring revenue verified by audited financials, not revenue growth; completion of Series B funding at a specific valuation, not successful fundraising. Document these definitions in your restricted stock agreement or vesting schedule addendum, and have all founders sign off before equity grants are issued. Vague milestone language costs founders tens of thousands in legal fees to litigate and costs companies years of distraction when founders should be building.

The Section 83(b) Election Deadline You Cannot Miss

Tax implications create a second category of expensive mistakes that founders ignore until the IRS arrives. Missing your Section 83(b) election deadline is permanent and catastrophic. You have exactly 30 days from grant to file with the IRS and your company; missing this window means you’ll owe ordinary income tax on each vesting tranche as it vests, potentially creating six-figure tax bills in years when your company has zero liquidity.

File your 83(b) election within two weeks of receiving your equity grant, treating the deadline as non-negotiable. Beyond the 83(b) window, founders regularly overlook how vesting changes interact with Qualified Small Business Stock eligibility under Section 1202. If your separation agreement or funding round restructures your vesting schedule, it can disqualify QSBS benefits worth millions in capital gains tax savings on exit. Before signing any amendment to your vesting terms during a funding round, have a tax attorney verify QSBS implications.

Investor Demands That Strip Your Protections

Failing to update vesting terms during funding rounds creates the third major pitfall. Investors regularly demand changes to acceleration clauses, cause definitions, or cliff periods as a condition of investment. Founders who don’t negotiate these changes upfront often discover mid-Series A that their acceleration protections have vanished or that cause now includes vague language like poor performance (which gives the board room to manufacture termination).

The time to lock in founder protections is before you take investor money, not after. Specify double-trigger acceleration, define cause narrowly with cure rights and formal process requirements, and clarify post-termination exercise windows for stock options. Longer post-termination exercise periods have trended longer recently, with about 20% of terminated options now offering windows longer than 90 days. Try for at least 90 days, preferably 180 days or longer, so you’re not forced to exercise options immediately after departure when you have no income from the company to cover the purchase price.

Final Thoughts

Equity vesting milestones separate founders who build lasting companies from those who face costly disputes and team departures at critical moments. The four-year vesting schedule with a one-year cliff works because it filters out uncommitted founders while rewarding those who stay through the hard years. Double-trigger acceleration protects you during acquisitions, milestone definitions must be specific and measurable, the Section 83(b) election window closes in 30 days and cannot be reopened, and investor demands during funding rounds can strip your protections if you don’t negotiate them upfront.

We at Primum Law Group help founders structure vesting plans that align incentives across your team while protecting your interests through growth phases and funding rounds. We review acceleration clauses, tighten cause definitions, verify QSBS eligibility, and ensure your vesting terms survive investor scrutiny. We’ve seen founders lose millions in equity because they treated vesting as a legal checkbox rather than a strategic tool.

If you haven’t documented your vesting schedule in a formal restricted stock agreement or shareholders agreement, do it now. If you’re approaching a funding round, have your vesting terms reviewed before you sign investor documents. Primum Law Group offers startup counseling and corporate governance services designed to address exactly these situations.