Seed financing can feel overwhelming when you’re evaluating convertible note options for the first time. The good news is that convertible notes are often the fastest way to raise capital without getting bogged down in valuation negotiations.

At Primum Law Group, we’ve guided countless founders through this decision. This guide breaks down how convertible notes work, compares them to other financing paths, and helps you determine if they’re right for your startup.

How Convertible Notes Actually Work

A convertible note is a debt instrument that converts into equity at a future financing event, typically a Series Seed or Series A round. Unlike a traditional loan, the note holder does not expect repayment in cash; instead, they receive shares in the company when conversion happens. The structure solves a real problem: founders need capital immediately, but setting a valuation too early can undervalue the company or create friction with future investors. Convertible notes delay that valuation conversation until the next priced round, when market conditions and traction provide clearer signals. The note accrues interest (usually 5–10% annually) and has a maturity date (often 18–24 months), creating a built-in incentive for both parties to move toward an equity round rather than let the note sit indefinitely. If no qualifying financing occurs by maturity, the note either converts at a predetermined valuation, gets extended, or requires repayment-a scenario founders must plan for seriously.

The Valuation Cap: Your Most Powerful Lever

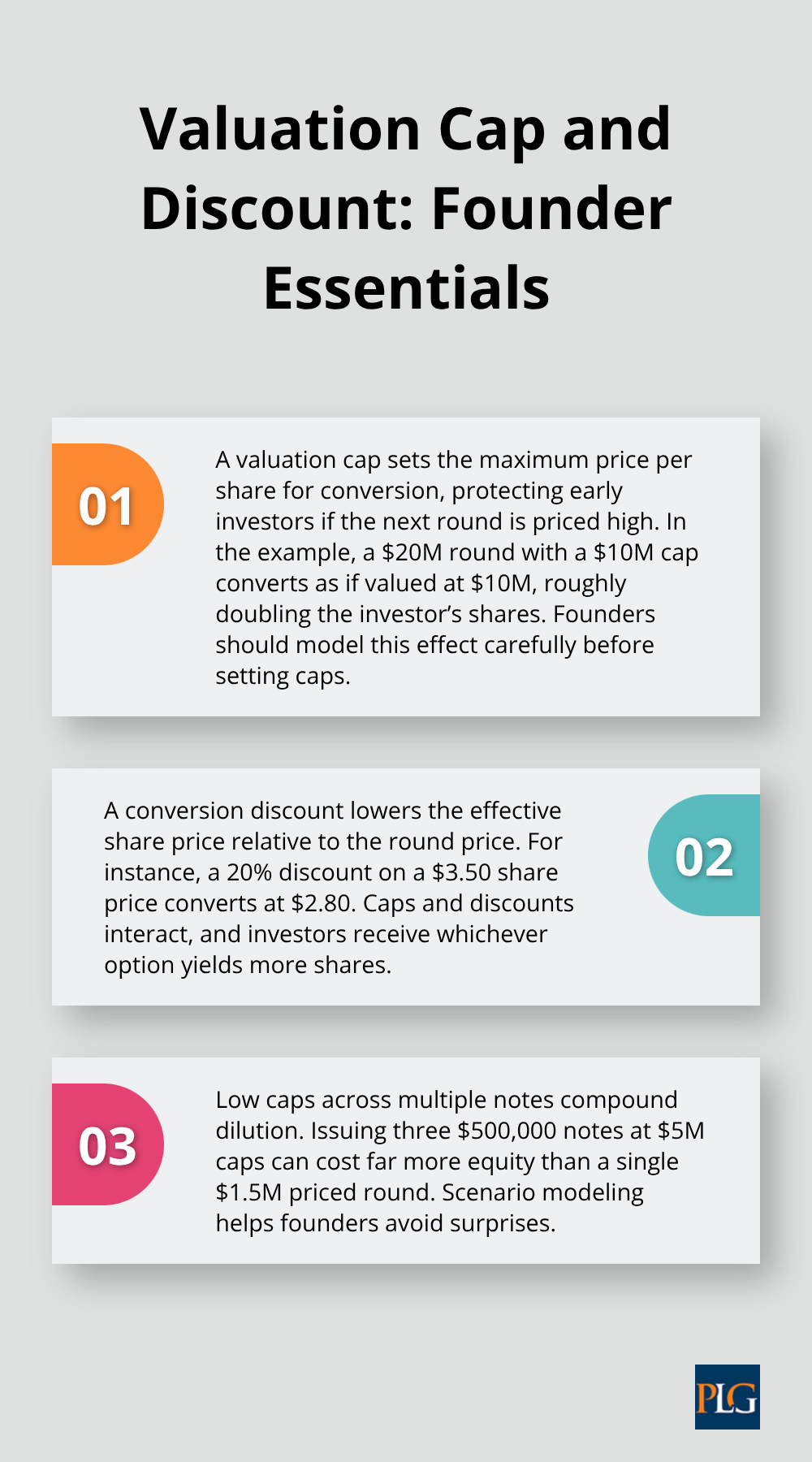

The valuation cap sets a ceiling on the price per share at which the note converts, protecting early investors from dilution if your next round is priced aggressively. If you raise a Series A at a $20 million pre-money valuation but your note has a $10 million cap, the investor converts as if your company was valued at $10 million, receiving roughly double the shares they would at the higher valuation. This sounds great for investors, but founders must model this carefully because a low cap compounds across multiple notes. If you issue three $500,000 notes each with a $5 million cap, you give away far more equity than a single $1.5 million priced round would cost.

The conversion discount (typically 10–30%) works alongside the cap; if your Series A is priced at $3.50 per share, a 20% discount lets the note holder convert at $2.80. The note holder receives whichever option yields more shares-cap or discount-so a $1 million note with both terms can end up dramatically more valuable than the cash invested suggests.

Maturity Dates and Repayment Risk

The maturity date creates urgency and shapes your fundraising timeline. If your note matures in 18 months and you have not closed a Series A, you face a choice: extend the note (which requires investor consent), convert at a predetermined valuation, or repay the principal plus accrued interest. Repayment can devastate a cash-constrained startup, so treat the maturity date as a genuine deadline, not a formality. Many founders underestimate how quickly 18 months passes when early traction is slow or market conditions shift. Plan your Series A timeline conservatively and build in buffer months to avoid a maturity crisis.

How Conversion Actually Happens

Conversion occurs automatically when you close a qualifying financing-typically a priced equity round of at least $500,000 to $1 million. At closing, the note converts into the same class of shares the new investors receive, usually preferred stock with liquidation preferences and other protections. The conversion price is calculated as the lowest of three options: the round price discounted by the discount rate, the valuation cap divided by the fully diluted share count, or (if applicable) an interest-adjusted price. In practice, the cap usually wins when your company’s valuation jumps significantly between the note issuance and the Series A.

Acquisition Scenarios and Unexpected Outcomes

If your company is acquired before conversion, outcomes vary by note terms. Many notes specify that the acquirer pays the greater of the invested amount or a small multiple (1x to 2x), converting to ordinary shares only if the deal value exceeds a threshold. This protects founders from unexpected dilution in a small exit but can disappoint note holders if the acquisition price is modest. Review your note terms upfront so there are no surprises when an acquisition offer arrives.

Stacking Multiple Notes and Cap Table Dilution

Founders often underestimate how multiple convertible notes stack and dilute ownership. If you raise $500,000 from three different angels on similar terms, each note’s cap and discount interact in ways that compound dilution at conversion. Run a cap table projection with realistic Series A pricing; use spreadsheet templates or cap table software to model scenarios where your Series A is priced at $10 million, $20 million, or $30 million pre-money. This exercise reveals whether your note terms are sustainable or whether you need to renegotiate caps with existing investors before they convert. Understanding these stacking effects now prevents painful dilution surprises later and positions you to negotiate better terms with your next round of investors.

Why Convertible Notes Close Faster Than Priced Rounds

Speed Advantage: Skipping the Valuation Debate

Convertible notes move faster because they sidestep the valuation negotiation that stalls most early-stage rounds. When you raise on a priced round, investors and founders spend weeks debating what the company is worth. With a convertible note, you skip that conversation entirely. The note holder accepts that valuation will be set later, at the Series A, when better data exists. This structural simplicity cuts legal complexity dramatically.

Standardized Templates Accelerate Closings

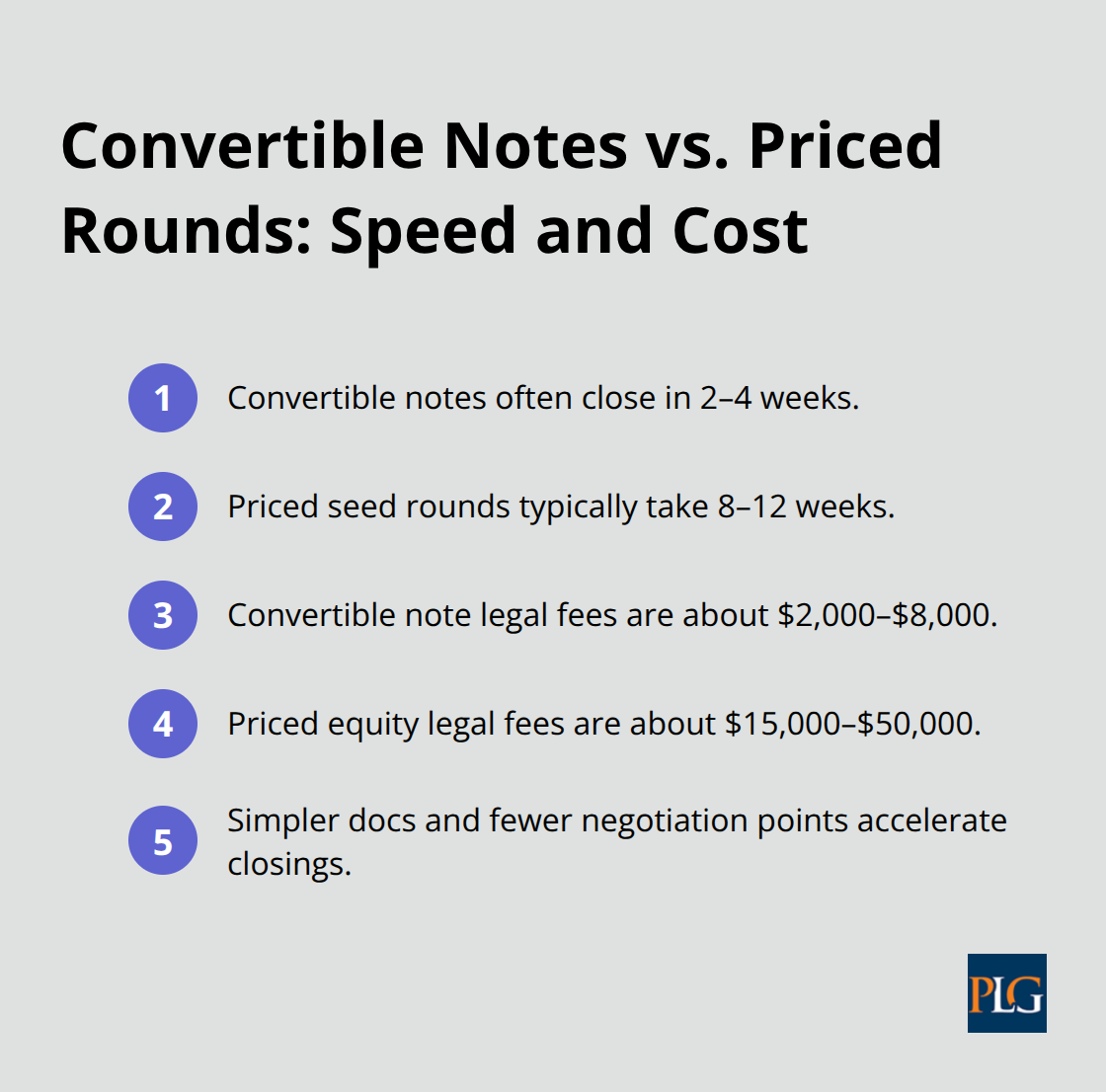

A typical convertible note uses a standardized template-Y Combinator’s SAFE or 500 Startups’ KISS document-that most investors recognize and trust. Closing a $500,000 convertible note round takes 2–4 weeks from first conversation to wire transfer. A priced seed round of the same size typically takes 8–12 weeks because you negotiate terms like liquidation preferences, board seats, and anti-dilution rights. The cost difference is equally stark.

A priced equity round costs $15,000 to $50,000 in legal fees depending on complexity. A convertible note costs $2,000 to $8,000 because the documentation is simpler and fewer negotiation points exist. For founders running lean, this difference matters. You save money and time, freeing up bandwidth to focus on product and customer acquisition instead of endless term sheets.

Hidden Complexity: Cap Table and Debt Liabilities

The speed advantage has real limits. Multiple convertible notes create cap table complexity that eventually catches up with you. If you raise five separate $200,000 notes from different angels, each with slightly different caps and discount rates, your cap table becomes a management headache. When the Series A arrives, your lead investor will demand clean cap table documentation and may push back on terms if the note stack is messy.

Convertible notes also create a hidden liability that founders often underestimate: debt on your balance sheet. Each note is technically a liability until it converts. Banks and institutional investors see this debt and may view it negatively when assessing your financial health. If your Series A falls through and notes mature, you face immediate repayment obligations. One founder we worked with raised $1.2 million across six convertible notes with an 18-month maturity. When Series A discussions stalled at month 16, she had to scramble to either extend all six notes (requiring unanimous consent) or face repayment demands. She eventually extended them, but the stress could have been avoided with clearer planning.

Dilution Risk Compounds Across Multiple Notes

The dilution risk is real. A $500,000 note with a $5 million cap in a Series A priced at $25 million pre-money converts into roughly 11% of the company on a fully diluted basis. Stack three such notes and you have given away 33% before your Series A investors even write a check. Convertible notes work best when you have a clear path to a Series A within 12–18 months and you are raising from investors comfortable with the uncertainty. They work poorly if you are building a bootstrapped company or targeting a slow fundraising timeline.

Understanding these trade-offs positions you to evaluate whether convertible notes truly fit your fundraising strategy or whether other seed financing options better match your timeline and capital needs.

Other Seed Financing Paths and When They Beat Convertible Notes

SAFEs: Speed Over Creditor Protection

SAFEs have become the default choice for founders who want even faster closings than convertible notes. A SAFE (Simple Agreement for Future Equity) strips away the debt mechanics entirely-no maturity date, no interest accrual, no repayment obligation if conversion never happens. This sounds founder-friendly, and in some ways it is, but the trade-off is real. SAFE investors have zero creditor protections. If your company fails before a priced round closes, they own nothing and recover nothing. Convertible note holders, by contrast, have debt priority in a liquidation scenario and can theoretically demand repayment. In practice, this rarely matters because most startups fail with no assets to recover, but institutional angels and some early VCs still prefer the debt status that notes provide.

SAFEs close in 1–2 weeks because almost nothing requires negotiation. Y Combinator standardized the SAFE template, and most founders and investors accept it without modification. The real danger with SAFEs emerges when you stack multiple post-money SAFEs without modeling the dilution carefully. A post-money SAFE sets ownership based on the company’s valuation after that investor’s money arrives, which means each successive SAFE dilutes earlier investors and founders differently. If you raise $250,000 from investor A on a post-money SAFE, then $250,000 from investor B on a post-money SAFE with a different valuation cap, the cap table math becomes slippery. Model post-money SAFE scenarios with cap table software before accepting investor commitments. Convertible notes, despite their complexity, actually provide clearer ownership mathematics because the conversion happens all at once at a qualifying financing, not piecemeal across rolling closings.

Priced Equity Rounds: Clarity at a Cost

Traditional priced equity rounds demand upfront valuation negotiation but deliver investor protections and founder clarity that convertible notes cannot match. When you raise a priced seed round, investors buy preferred shares with liquidation preferences, anti-dilution rights, and sometimes board representation. This costs $20,000 to $50,000 in legal fees and takes 10–14 weeks to close, but the resulting cap table is clean and transparent. Every shareholder knows exactly what they own and what happens in various exit scenarios. The time and expense create friction, but the outcome eliminates ambiguity about future dilution and investor rights.

Grants and Revenue-Based Financing: Non-Dilutive Alternatives

Grants and revenue-based financing occupy a different universe entirely. Grants from organizations like SBIR or state economic development programs provide non-dilutive capital, but they typically target specific industries (biotech, cleantech, hardware) and come with reporting requirements and timeline constraints. Revenue-based financing lets you repay investors from a percentage of monthly revenue rather than equity, which preserves founder control but only works if your business generates predictable recurring revenue within 12–24 months. A SaaS startup doing $10,000 monthly recurring revenue might refinance via revenue-based financing at a cost of $150,000 to $200,000 in total repayment, avoiding equity dilution entirely. But a pre-revenue hardware startup or marketplace cannot access this option.

Matching Your Financing Choice to Your Situation

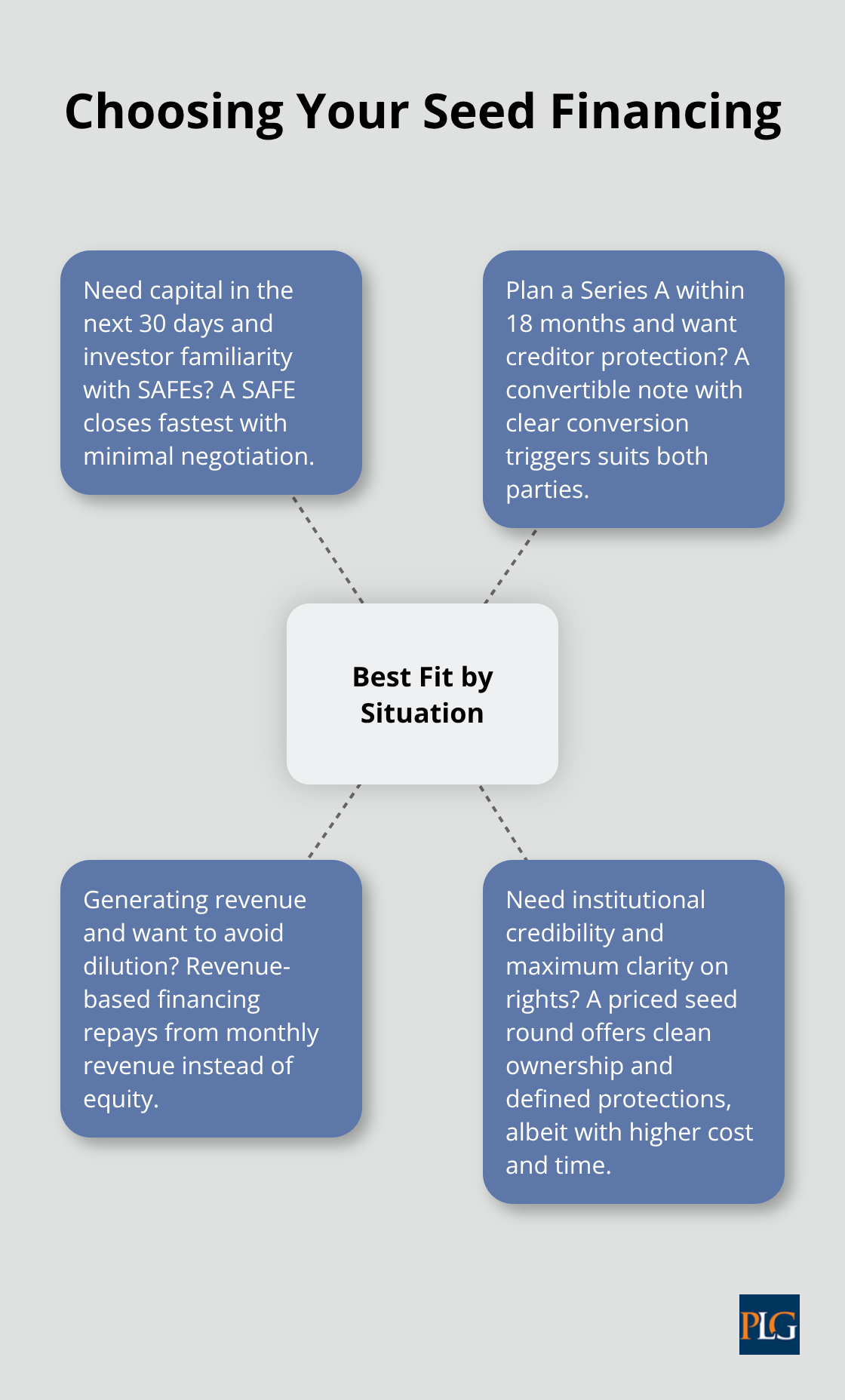

The choice between convertible notes, SAFEs, priced rounds, and alternatives depends entirely on your timeline, investor base, and path to profitability. If you need capital in the next 30 days and your investors understand SAFEs, a SAFE closes fastest. If you need institutional credibility and plan a Series A within 18 months, a convertible note with clear conversion triggers protects both parties. If your business generates revenue and you want to avoid dilution, revenue-based financing deserves serious evaluation.

No universally superior option exists-only the right fit for your specific situation.

Final Thoughts

Convertible note options work best when you need capital quickly and can reach a Series A within 18 months. If your startup shows early traction, clear product-market fit signals, and investors who understand convertible mechanics, this path accelerates your runway without valuation friction. The speed and lower legal costs preserve capital for product development and customer acquisition instead of legal fees.

Model your cap table across realistic Series A scenarios before you commit to any terms. Run projections assuming your next round prices at $10 million, $20 million, and $30 million pre-money to reveal whether your valuation caps and discount rates create acceptable dilution (or whether you need to renegotiate with existing investors). Treat your maturity date as a genuine deadline, not a formality, and plan your Series A timeline conservatively to avoid a crisis when month 16 arrives.

Evaluate your investor base and capital needs honestly to determine which financing path truly fits your situation. We at Primum Law Group help founders navigate convertible note options by modeling scenarios, reviewing term sheets, and structuring financing in ways that support long-term cap table health. Contact our team for guidance on structuring your seed round.