Venture financing agreements shape the future of startups, yet many founders sign term sheets without fully understanding what they’re agreeing to. The gap between investor expectations and founder protection often determines whether a deal strengthens or weakens your company’s position.

At Primum Law Group, we’ve seen how the right negotiation strategy and compliance framework can make the difference between a deal that fuels growth and one that creates long-term friction. This guide walks you through the critical components you need to know.

What Actually Matters in a Term Sheet

The Liquidation Preference Trap

The numbers on a term sheet determine ownership stakes and investor returns, but most founders focus on the wrong metrics. Valuation gets all the attention, yet the liquidation preference buried on page three often has more impact on your exit outcome. In 2025, San Francisco startups closed deals with increasingly complex structures, especially as mega-rounds like OpenAI’s $40 billion and Anthropic’s $15 billion set new market expectations. These massive rounds concentrated investor power among a small set of Bay Area firms, which means standard terms shifted toward investor protection mechanisms.

Your pre-money valuation matters less than understanding what happens when you sell. A 1X non-participating liquidation preference means investors get their money back first, then remaining proceeds go to common shareholders. A 2X preference doubles that threshold before founders see anything. Model both scenarios: if you raise $10 million on a $30 million pre-money valuation and sell for $50 million, a 1X preference lets investors take $10 million and split the remaining $40 million with you proportionally. With 2X, investors take $20 million first, leaving only $30 million to split. That’s a $5 million swing in founder proceeds.

Anti-Dilution Mechanics and Board Control

Anti-dilution provisions protect investors if future rounds price down, but broad-based weighted average anti-dilution can significantly reduce founder ownership in down rounds without triggering a full ratchet. The difference between broad-based and full ratchet matters: full ratchet resets investor shares as if they bought at the new, lower price, while broad-based weighted average dilutes everyone proportionally.

Board representation directly controls your decision-making authority. A 2-1 board (two founder seats, one investor seat) keeps founder control. A 2-2-1 structure (two founders, two investors, one independent) creates balance but means you need investor support for major decisions. Anything investor-heavy hands control to your investors.

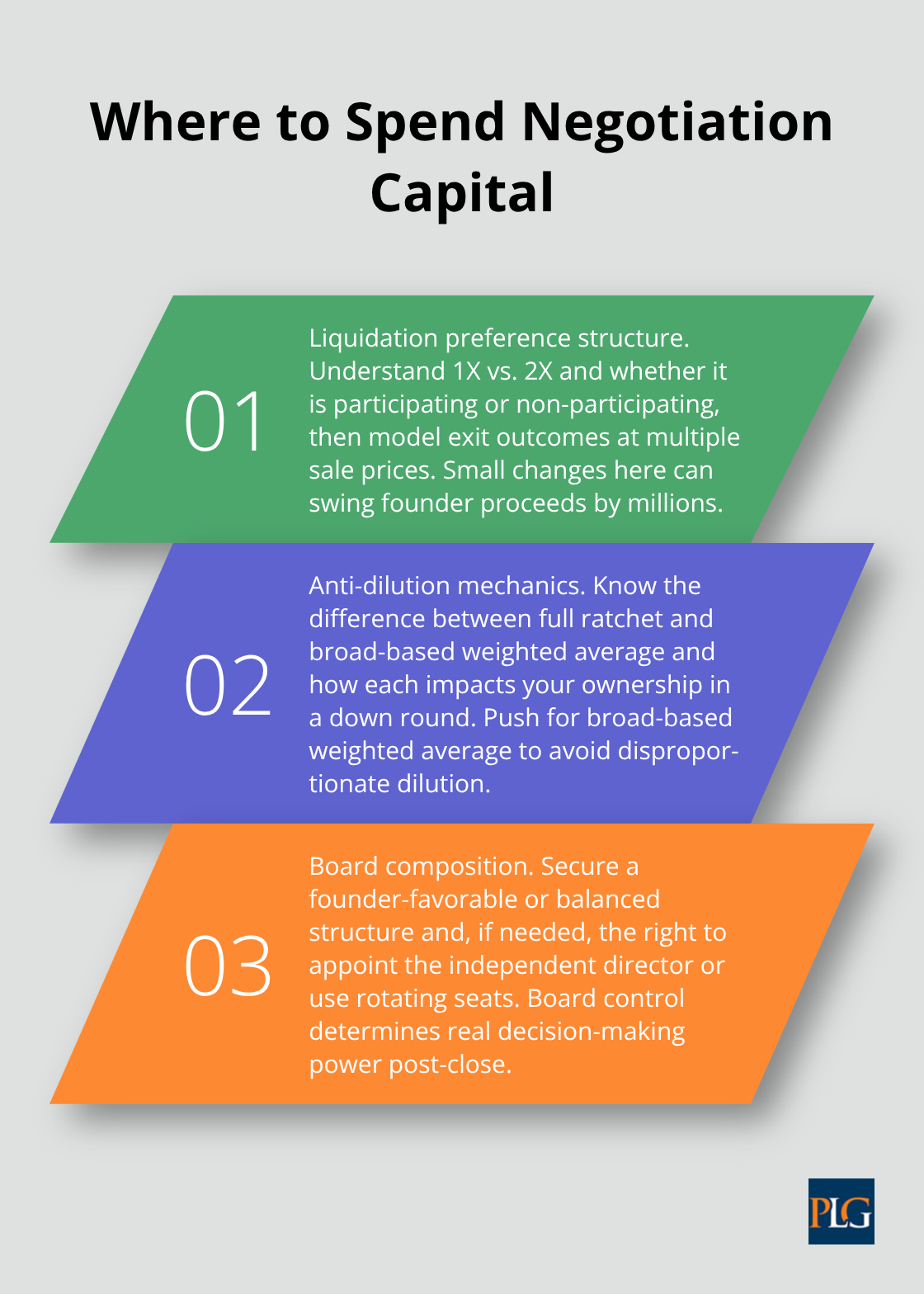

Where to Spend Your Negotiation Capital

Focus your negotiation energy on the three items that shape your company’s future: the liquidation preference structure, anti-dilution mechanics, and board composition. Lower valuation from a strong investor often beats higher valuation from a weaker one, especially in concentrated markets where investor reputation and follow-on capacity matter more than the valuation number itself. This reality shapes how you approach the next phase of your fundraising strategy.

How to Negotiate Without Losing Leverage in San Francisco Venture Deals

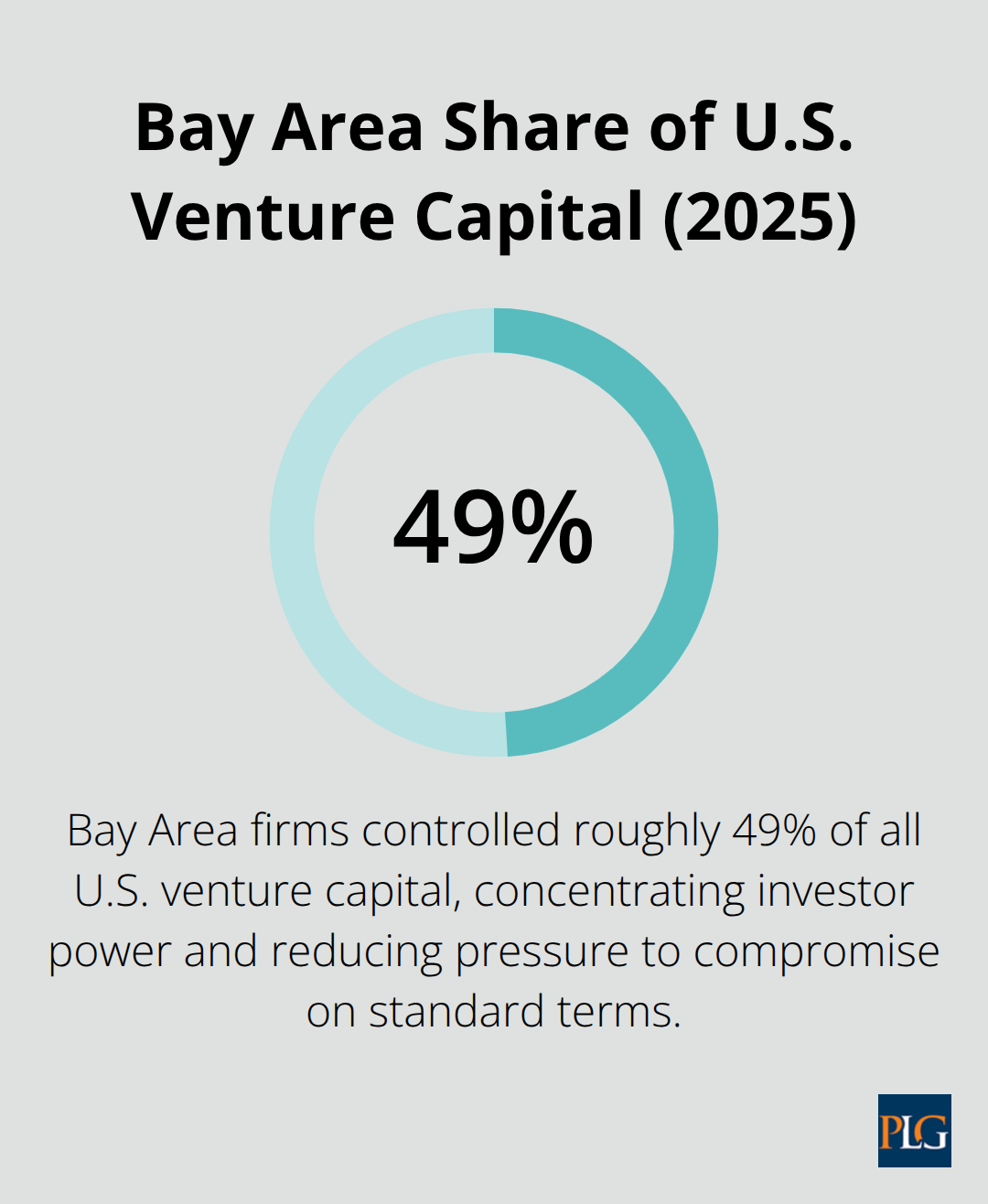

Negotiating a term sheet means understanding what investors actually need versus what they’re asking for. Most founders treat every line item as equally important and exhaust themselves fighting over provisions that barely move the needle. The 2025 San Francisco fundraising environment shows this clearly: with Bay Area firms controlling roughly 49% of all U.S. venture capital and seven of the top ten largest rounds belonging to San Francisco startups, investor power has concentrated significantly. This concentration means investors have less need to compromise on standard terms. Your job is to identify which terms genuinely protect your company and where you have real leverage to negotiate.

Investor expectations have shifted based on market dominance. When Anthropic closed its $15 billion round and OpenAI raised $40 billion, both in 2025, those mega-rounds reset expectations for protective provisions across the entire market. Investors now expect robust information rights, including quarterly financial statements, annual audited financials, and board observer rights. They also expect drag-along rights that let a majority shareholder force a sale, preventing you from blocking exits that other shareholders support. These provisions rarely yield to negotiation. Instead, focus on the provisions that directly impact founder control: board composition, protective provisions that require investor consent for specific actions, and vesting acceleration clauses tied to termination without cause.

Board Composition Determines Your Real Power

Your board controls major decisions, so its composition directly determines how much control you retain. A founder-heavy board like 2-1 gives you clear advantage: two founder votes versus one investor vote means you win most decisions. A balanced 2-2-1 structure introduces an independent director who breaks ties, which sounds neutral but often favors investor interests because that independent director typically comes from the investor’s network. Investor-heavy boards like 1-2-1 or 1-3 essentially hand control to your investors. In concentrated markets where a small number of Bay Area firms lead most rounds, expect investors to push for 2-2-1 minimum. This is where you should spend negotiation capital. If you can’t get 2-1, lock in the right to appoint the independent director yourself, or negotiate for rotating board seats that shift control back to founders in future rounds. Also negotiate for board observer rights for any major shareholders who don’t get seats, giving them visibility without voting power. This prevents surprise opposition from shareholders you thought were passive.

Protective Provisions and Operational Freedom

Investors will demand detailed information rights: monthly financial statements, annual budgets, quarterly cap table updates, and board materials. These are standard and reasonable. What matters is the timing and format. Negotiate for reasonable deadlines (45 days for annual audited statements is standard, not 30 days) and define what qualifies as material information that triggers special disclosure. On protective provisions, every investor will want consent rights over major decisions. The real negotiation is defining what counts as major. A $100,000 contract shouldn’t require investor consent, but a $5 million annual spend on a new product line should. Set dollar thresholds that give you operational freedom while protecting investor interests. Also push back on provisions requiring consent for ordinary course hiring, software purchases, and vendor agreements. These create operational friction without meaningful investor protection.

Vesting Acceleration and Founder Protection

Vesting acceleration clauses matter enormously: ensure that if the company fires you without cause, your unvested equity accelerates so you retain meaningful ownership. Double-trigger acceleration (acceleration only if fired after an acquisition) is standard but weaker than single-trigger acceleration tied to termination alone. Negotiate for at least partial single-trigger acceleration, especially if you’re in an early round where your equity represents substantial founder value. A typical protective provision list includes raising new capital, issuing equity beyond reserved pools, mergers or acquisitions, and dissolution. Negotiate hard on which actions require investor approval versus which ones you can execute independently. You should retain authority to hire and fire employees, approve annual budgets within a defined range, and make ordinary course business decisions without investor sign-off. These operational decisions determine whether your company can move quickly or gets bogged down in approval cycles.

The concentration of venture capital among Bay Area investors means your next negotiation will likely involve firms that have already closed mega-rounds and set their standard terms accordingly. Understanding which provisions actually protect investor interests versus which ones simply entrench their control determines whether you walk away with a deal that fuels growth or one that constrains your decision-making for years to come.

What You Must Handle After Closing Your Round

Closing a venture round feels like the finish line, but it marks the start of a compliance marathon that most founders underestimate. The moment you accept investor money, you enter a regulated environment with specific filing deadlines, tax obligations, and reporting requirements that vary based on where your investors operate and where your company is incorporated. Miss these deadlines and you face penalties ranging from administrative fines to loss of good standing status that blocks future fundraising. Founders who nail the negotiation often stumble on the mechanics that follow.

Delaware Franchise Tax and State Compliance

If your company is Delaware-incorporated, the Franchise Tax deadline is non-negotiable. Delaware requires an annual report and franchise tax payment by March 1st each year, based on your authorized shares and capitalization. The penalty for missing this deadline starts at $200, then increases by $10 per day of continued non-compliance, and you can lose good standing status that prevents you from raising future capital or closing acquisitions. Most founders don’t realize their accountant or CFO might miss this deadline because it sits separate from federal tax filing.

Set a calendar reminder for January and confirm your Delaware registered agent has the current cap table. If you’re pre-revenue or early-stage, the minimum annual tax is $75, but significant capitalization scales the tax upward. Plan this filing in advance rather than scrambling in February.

The California Fair Investment Practices by Venture Capital Companies Law adds another layer if your investors have California operations. If your lead investor is a California-based venture capital firm, they must register with the California Department of Financial Protection and Innovation by March 1, 2026 and file an annual founder survey report by April 1, 2026. This law requires anonymized demographic data collection about your founding team, including gender, race, ethnicity, disability status, veteran status, and LGBTQ+ identity. The survey is technically voluntary for founders, but investors face regulatory enforcement if they don’t attempt collection. The reported data becomes public in a searchable format, so expect LP scrutiny and media coverage. This transparency regime shifts how investors evaluate portfolio diversity and may influence future funding rounds based on founder demographics.

Securities Law Filings and Cap Table Documentation

Federal securities law requires you to file Form D with the SEC within 15 days of your first sale of securities if you rely on Regulation D exemptions. Most venture rounds use Regulation D, which exempts offerings from registration but still requires this minimal filing. State blue sky laws add complexity: some states require additional filings or approvals. Delaware imposes no significant additional burden, but if you have investors in New York, Texas, or California, check state-specific requirements. Your securities counsel should handle Form D, but you remain responsible for accuracy. Incorrect filings can trigger SEC inquiries or state enforcement actions.

After closing, your cap table must be precisely documented in your stock ledgers and corporate records. Every share issuance needs a board resolution, stock certificate, and investment agreement. Sloppy documentation creates massive problems during due diligence for future rounds or acquisitions. Founders lose weeks of time cleaning up cap table errors that prevention at closing would have avoided. Your stock option plan and grant agreements also require careful documentation. If you promised employees options, the plan must be properly adopted by the board and each grant must include a vesting schedule with acceleration terms. The IRS scrutinizes option pricing: if you grant options at below fair market value, it can trigger adverse tax consequences for both you and your employees.

Tax Structuring and Valuation Requirements

Section 409A of the tax code governs option valuation and vesting. If your option strike price falls below the fair market value of your common stock, employees face immediate tax liability on the spread between the strike price and FMV. This creates cash flow problems because employees owe taxes on gains they haven’t realized yet. Your board should obtain a Section 409A valuation from a qualified valuation firm annually to document fair market value. This valuation costs $2,000 to $5,000 but protects you from IRS challenges.

For healthcare startups and multi-location service organizations using MSO or PC structures, tax compliance becomes significantly more complex. Different states impose different requirements on how you structure medical practices, which affects your tax liability and regulatory standing. If you operate across multiple states, consult a tax advisor on whether you should file separate returns or consolidated returns. State income tax nexus rules mean you may owe tax in states where you have no physical office but serve patients or clients.

Post-Investment Reporting and Financial Close Processes

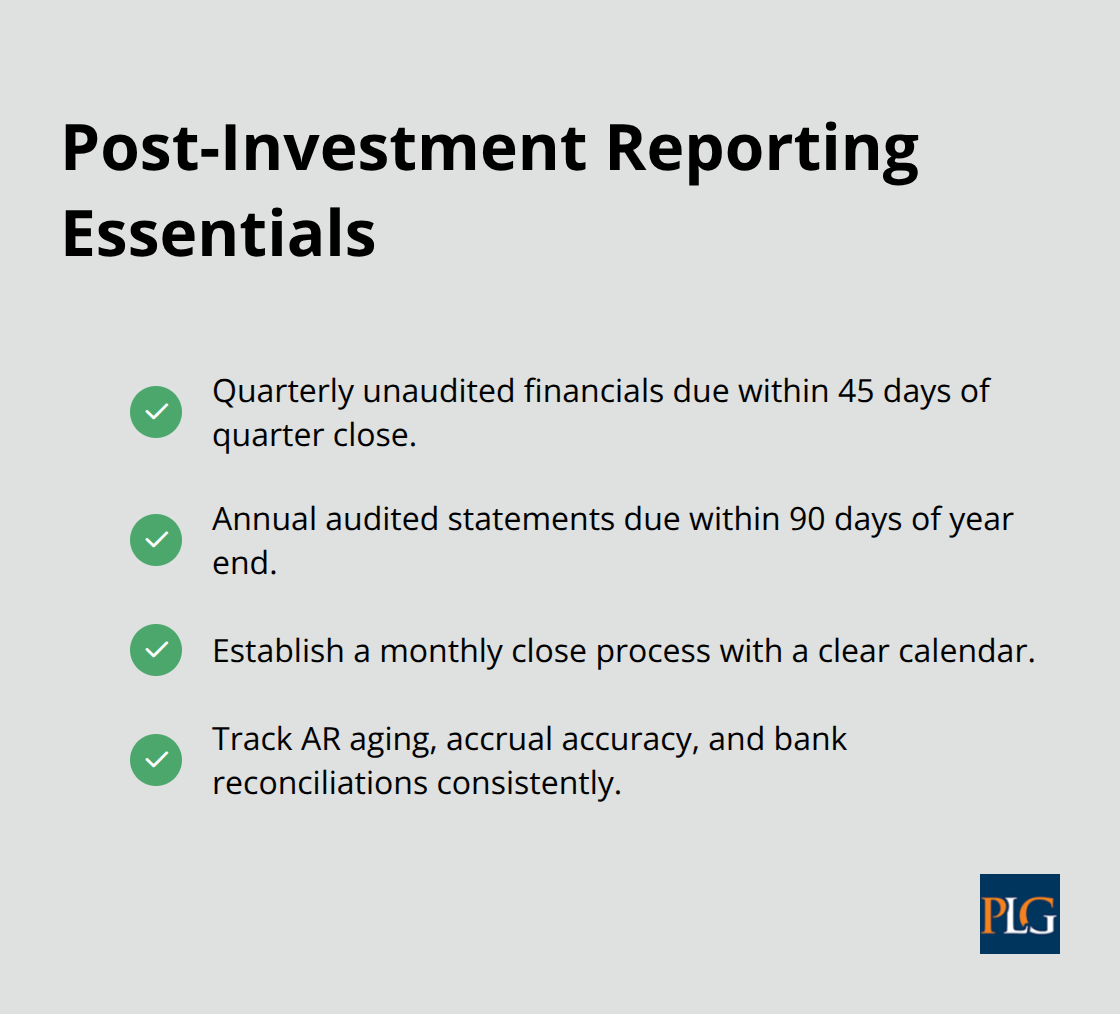

Post-investment reporting to your investors requires quarterly financial statements and annual audited or reviewed financials depending on investor requirements. Most Series A rounds expect quarterly unaudited statements within 45 days of quarter close and annual audited statements within 90 days of year end. If you miss these deadlines, you violate your investor rights agreement and can trigger default provisions.

Set up a monthly close process with a clear calendar.

Automated close checklists track AR aging, accrual accuracy, and bank reconciliation timing. Even early-stage startups should implement a structured close process that takes two weeks maximum from month end to final statements. This discipline prevents the scramble that derails investor confidence and creates compliance risk. Your investors expect consistency and accuracy in financial reporting, and meeting these expectations builds trust for future funding rounds.

Final Thoughts

Venture financing agreements determine whether your startup thrives or gets constrained by investor control. The founders who succeed navigate term sheets by focusing on the provisions that genuinely matter: liquidation preferences, anti-dilution mechanics, board composition, and vesting acceleration. Everything else wastes your energy and damages your credibility with investors.

The 2025 San Francisco fundraising environment shows that investor power has concentrated among a small set of Bay Area firms, which means you won’t negotiate away standard protective provisions like information rights or drag-along rights. Instead, spend your negotiation capital on board control, operational freedom through defined dollar thresholds on protective provisions, and founder protection through vesting acceleration. A lower valuation from a strong investor beats a higher valuation from a weaker one because follow-on capacity and investor reputation matter more than the initial number.

After closing, compliance becomes your immediate priority, and venture financing agreements require you to meet Delaware franchise tax deadlines, obtain Section 409A valuations, document your cap table precisely, and deliver quarterly investor reporting on schedule. Missing these deadlines costs you good standing status, triggers penalties, and damages investor confidence before your next fundraising round. We at Primum Law Group help startups navigate venture financing agreements from term sheet negotiation through post-investment compliance, turning complex agreements into clear strategy.