Expanding your business across borders brings real opportunities-and real legal complexity. International corporate law governs everything from entity setup to contract enforcement, and getting it wrong costs time and money.

At Primum Law Group, we’ve seen companies stumble because they underestimated local requirements or missed tax implications. This guide walks you through the legal structures, contracts, and pitfalls you need to navigate for successful cross-border ventures.

Setting Up Your Legal Structure Across Borders

When you establish operations in multiple countries, you face a fundamental choice: operate through a single parent entity or create separate legal entities in each jurisdiction. The wrong decision locks you into inefficient tax structures or leaves you exposed to liability in ways you didn’t anticipate. A Delaware C-corporation works well for attracting U.S. venture capital, but it becomes a liability if your core operations sit in Singapore or London. Start with a tax map before you incorporate anywhere. This means identifying where your revenue originates, where your employees live, where your intellectual property should sit, and which jurisdictions impose minimum capital requirements or mandatory local ownership stakes.

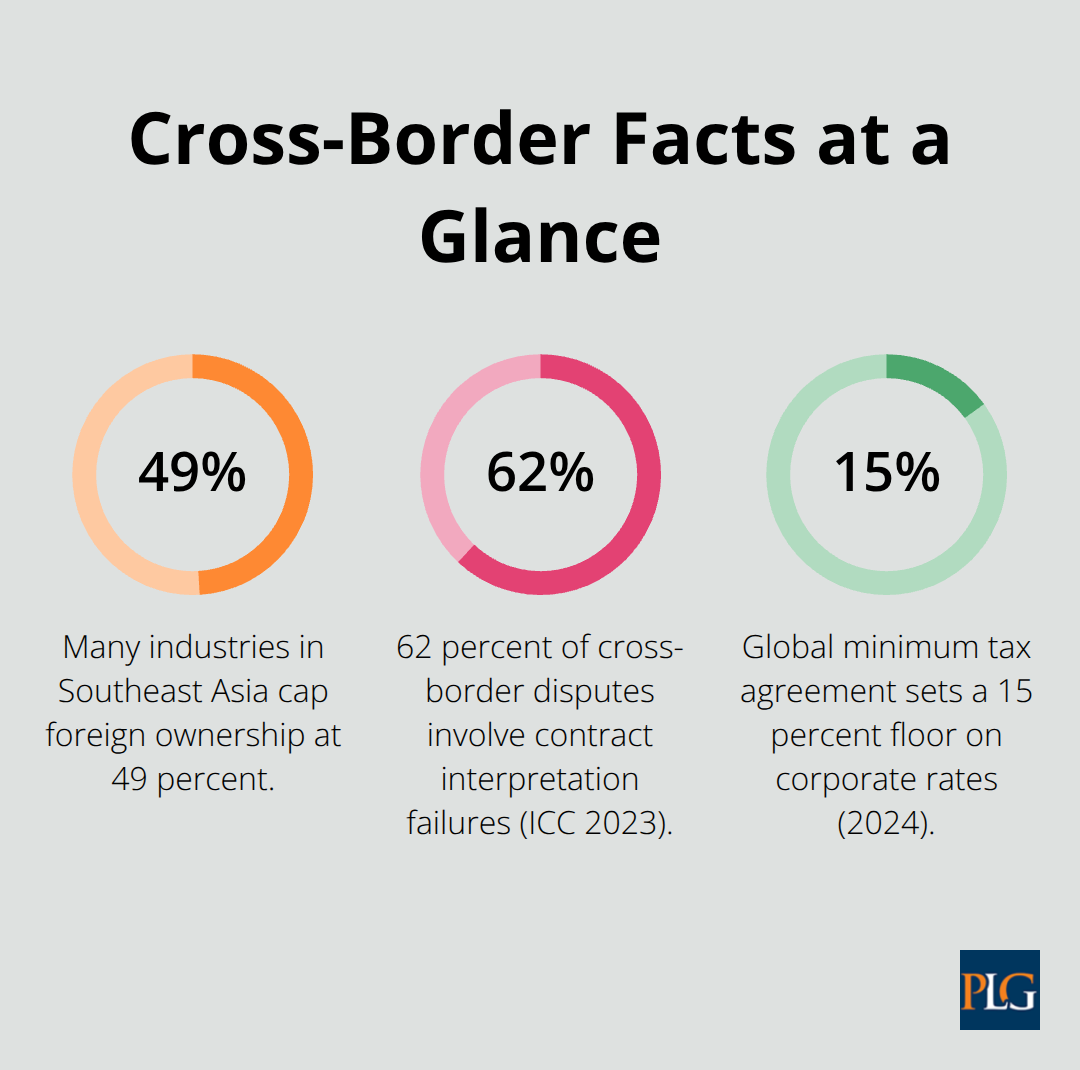

Foreign ownership limits vary dramatically across sectors and countries. In Southeast Asia, many industries cap foreign ownership at 49 percent, while others prohibit it entirely. The EU generally welcomes foreign investment but imposes strict data residency requirements that force you to store customer information within EU borders.

Japan and South Korea require local board representation in many cases. These aren’t bureaucratic nuances you can ignore during year two-they shape your entire corporate architecture from day one.

Where to Incorporate Your Parent Company

Your parent entity should live in a jurisdiction with strong contract enforcement, favorable tax treaties, and predictable courts. Delaware dominates for U.S.-focused ventures because it offers well-developed case law, no state income tax on corporate profits, and rapid corporate filings. If you’re targeting European markets or have substantial EU operations, the Netherlands or Ireland provide favorable tax treatment and extensive treaty networks. The choice matters for transfer pricing, withholding taxes, and dispute resolution.

A Delaware parent with subsidiaries in Ireland and Singapore gives you flexibility to route IP licensing, financing, and service agreements through tax-efficient jurisdictions while remaining compliant with arm’s length rules. The OECD’s transfer pricing guidelines, adopted by over 140 countries, require that intercompany transactions reflect what unrelated parties would charge. Violating this invites aggressive audits and double taxation. Document every transaction between your entities with contemporaneous pricing studies.

Managing Tax Obligations Across Multiple Countries

International operations trigger multiple tax regimes simultaneously. The U.S. taxes its citizens and residents on worldwide income, plus it taxes foreign corporations on U.S.-source income. The EU applies VAT on digital services and physical goods differently depending on where the customer sits. China taxes foreign entities on China-source income and increasingly requires local staff to contribute to social insurance. Most countries have tax treaties with the U.S. and each other, but these only work if you claim them correctly. Many companies leave money on the table by failing to file for foreign tax credits or treaty benefits.

If you have U.S. shareholders and foreign subsidiaries, the Global Intangible Low-Taxed Income rules and Base Erosion and Profit Shifting initiatives constrain how much profit you can shift to low-tax jurisdictions. A 2024 global minimum tax agreement sets a 15 percent floor on corporate rates, reducing opportunities for aggressive tax planning. Transfer pricing documentation now requires detailed economic analysis, comparable company studies, and contemporaneous records. If you skip this, tax authorities can impose penalties of 20 to 40 percent on adjustments, plus interest.

Building Your Cross-Border Tax Strategy

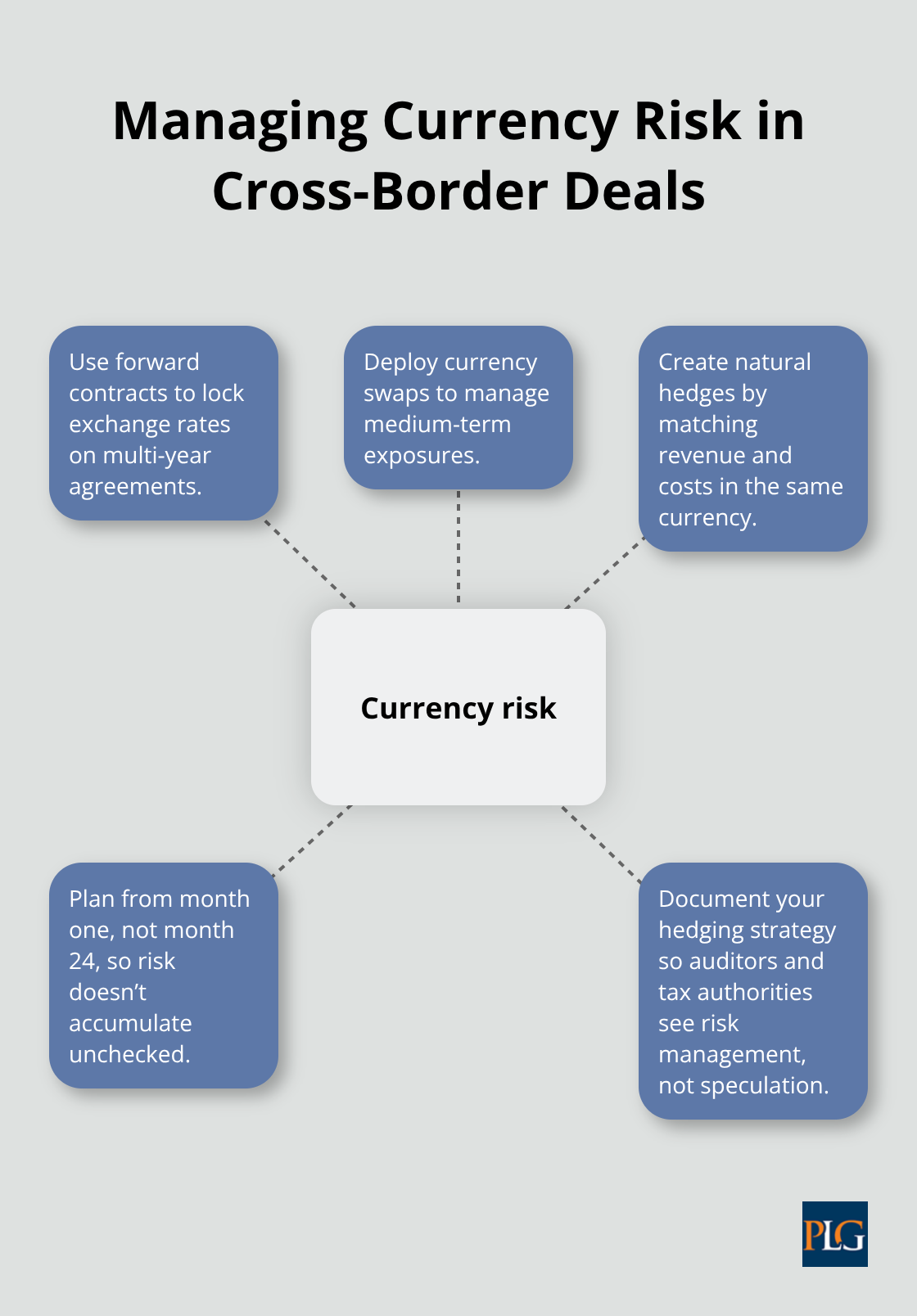

Engage a cross-border tax advisor early-the cost of planning beats the cost of remediation by orders of magnitude. Your tax strategy should account for withholding taxes on dividends, interest, and royalties flowing between entities. Currency fluctuations can trigger unexpected gains or losses on intercompany loans, so structure financing with forward contracts or natural hedges. Many companies operating across the U.S., EU, and Asia-Pacific regions face conflicting requirements around profit allocation and substance requirements. A jurisdiction might demand that you maintain local staff, office space, and decision-making authority to justify keeping profits there. Substance without strategy leaves you vulnerable to transfer pricing challenges, but strategy without substance invites reputational and legal risk. The next section covers how to draft contracts that actually hold up when disputes cross borders.

Contracts That Hold Up Across Borders

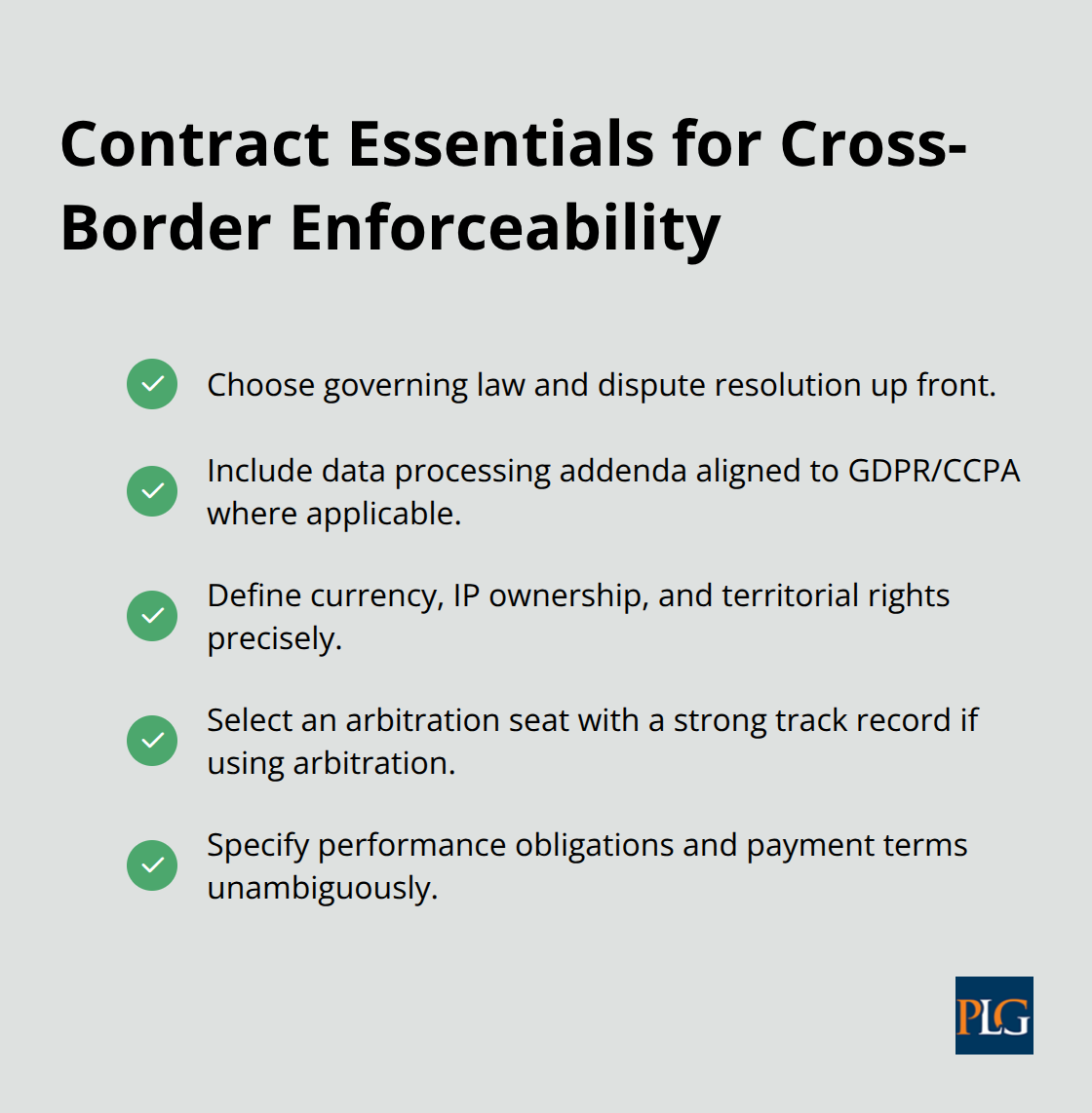

International contracts fail not because of poor drafting but because companies ignore governing law and dispute resolution from the start. You must choose which country’s laws control your agreement before you need a court to enforce it. Most U.S. companies default to New York or Delaware law out of habit, but this choice locks you into expensive litigation in U.S. courts even when the dispute involves European or Asian parties. International arbitration under the New York Convention on the Recognition and Enforcement of Foreign Arbitral Awards gives you a faster, more neutral path. Over 170 countries enforce arbitration awards under this convention, meaning a Singapore arbitrator’s decision carries weight in London, São Paulo, and Tokyo without requiring you to fight through local courts. Arbitration typically resolves disputes in 18 to 24 months versus three to five years for litigation, and confidentiality keeps your business disputes out of public records. Choose your arbitration seat carefully-London, Singapore, and Geneva have strong track records and developed case law. Avoid seats in countries where one party has political influence or where courts routinely overturn arbitration awards.

Governing Law and Dispute Resolution

Contracts crossing borders must address currency, data transfers, and intellectual property ownership with surgical precision because local laws override your agreement if you get it wrong. If you license software to a German customer, GDPR applies regardless of what your contract says-you must process personal data only for specified purposes, keep it secure, and honor deletion requests. A 2023 International Chamber of Commerce survey found that 62 percent of cross-border disputes involved contract interpretation failures, often because parties used vague language around performance obligations or payment terms in different currencies.

Specify exactly which version of GDPR, CCPA, or local privacy law applies, and build data processing addenda into every contract that touches customer information.

Allocating Intellectual Property Rights

Intellectual property ownership requires explicit allocation: state which party owns background IP brought into the deal, which owns IP developed during performance, and what happens to jointly developed IP on exit. Many companies assume they own what they create, but German law presumes employees own inventions unless the employment contract explicitly assigns them. If you’re expanding to Southeast Asia, Thailand and Vietnam impose strict local ownership requirements on technology and manufacturing-your contract structure must reflect these limits or face unenforceability.

Managing Currency and Financial Risk

Currency risk deserves its own clause: specify whether payments occur in USD, EUR, or the local currency, and decide whether exchange fluctuations above a threshold trigger adjustment mechanisms. A 15 percent swing in EUR/USD can wipe out margin on a three-year contract, so forward contracts or natural hedges belong in your financial planning alongside your legal agreements.

Protecting IP Across Jurisdictions

Intellectual property protection varies wildly across jurisdictions, and your U.S. patent or trademark registration means nothing in China, India, or Brazil without separate filings. The World Intellectual Property Organization’s Patent Cooperation Treaty lets you file a single international application that covers over 150 countries, but you must file within 12 months of your first U.S. filing or lose priority rights. Trademarks require country-by-country registration under the Madrid Protocol, which covers 130 countries and costs far less than filing separately-a single Madrid filing covers multiple countries for under $1,000 versus $2,000 to $5,000 per country filing individually. Trade secrets, however, travel differently: the U.S. Defend Trade Secrets Act lets you sue for misappropriation in federal court even across state lines, but the EU has no equivalent statute. Instead, EU member states rely on unfair competition laws and employment contracts with restrictive covenants. Non-disclosure agreements must comply with local law-Germany limits non-competes to two years and requires compensation, while California voids them entirely. If you’re transferring technology to a joint venture partner in India or Southeast Asia, require auditable controls over access, segregate confidential information from standard operations, and document every transfer with contemporaneous agreements.

Licensing Agreements and Territorial Restrictions

Many companies lose IP not through theft but through careless licensing: a perpetual, non-exclusive license in one contract plus a territory-limited exclusive license in another creates conflicts that courts resolve against the drafter. State clearly whether licenses are exclusive or non-exclusive, whether they cover improvements and derivative works, and what happens if either party is acquired. Territorial restrictions matter because European competition law scrutinizes exclusive licensing arrangements, while U.S. antitrust law applies different standards to the same restriction. When drafting and negotiating contracts for multinational operations, these details determine whether your agreements survive enforcement across borders or collapse when disputes arise-which brings us to the common pitfalls that derail even well-intentioned cross-border ventures.

Where Cross-Border Ventures Stumble

Compliance gaps destroy cross-border ventures faster than bad contracts or weak tax planning. Companies operating in Southeast Asia often assume that complying with regulations in their home country is sufficient, then face surprise licensing denials or operational shutdowns when local authorities demand certifications, local staff, or minimum capital thresholds that weren’t on anyone’s radar. Thailand requires foreign companies in certain sectors to maintain Thai nationals in management roles and restricts land ownership entirely. Vietnam imposes strict local content requirements on manufacturing and technology transfers. These aren’t minor inconveniences-they reshape your operational model, staffing, and ownership structure.

Map Regulations Before You Invest

The solution is a regulatory audit before you invest a dollar: map every jurisdiction where you operate or plan to operate, identify which licenses, permits, and registrations you need, and assign one person ownership of compliance for each market. Build a regulatory calendar that tracks filing deadlines, renewal dates, and audit cycles across jurisdictions. A single missed filing in one country can invalidate your right to operate there, trigger penalties, and expose you to personal liability for officers and directors.

Manage Currency Risk From Day One

Currency risk compounds compliance failures. A company with revenue in EUR and costs in USD faces real margin pressure if exchange rates move 10 to 15 percent-which happens multiple times per year. Many ventures ignore this because they assume currency fluctuations wash out over time, but a three-year contract locked at today’s exchange rates can evaporate profitability within months if the rate swings against you. Forward contracts, currency swaps, and natural hedges (matching revenue and cost currency) belong in your financial planning from month one, not month 24. Document your hedging strategy in writing so that auditors and tax authorities understand you’re managing business risk, not speculating.

Local Rules Override Your Contracts

Cultural and business practice differences create silent failures that documents cannot fix. Negotiation styles, decision-making timelines, and trust-building processes vary dramatically across regions. In Japan and South Korea, relationship-building precedes negotiations; rushing into contract terms before establishing trust signals disrespect and kills deals. In the Middle East, personal relationships matter more than formal governance structures. In Germany and Scandinavia, detailed written agreements and upfront legal clarity are expected and respected. A U.S. company accustomed to rapid deal cycles and loose handshake agreements will frustrate partners in civil-law jurisdictions where everything must be documented and codified.

Hire local counsel not just for legal compliance but for cultural guidance-they identify which business practices will alienate partners or trigger regulatory scrutiny. Many joint venture failures trace back to misaligned expectations around decision-making authority, profit distribution, and exit timelines that were never articulated because both parties assumed their home-country norms applied. Specify these explicitly: define how many board votes are required for major decisions, set clear timelines for capital calls, and agree on valuation methodologies for exit scenarios before disputes force the issue.

Validate Your Structure Across Jurisdictions

Tax authorities in different jurisdictions interpret transfer pricing, substance requirements, and profit allocation through their own cultural and legal lenses. A structure that satisfies the IRS might trigger aggressive audits in Germany or Singapore because local officials expect different economic substance or documentation. Work with local tax counsel in each major jurisdiction to validate your structure before implementation, not after audits begin.

Final Thoughts

Cross-border ventures succeed when you treat international corporate law as a foundation, not an afterthought. The companies that stumble typically made one of three mistakes: they underestimated local compliance requirements, they ignored currency and tax implications until audits arrived, or they assumed their home-country business practices would translate across borders. None of these failures stem from bad luck-they stem from skipping the planning phase.

Map your regulatory obligations before you incorporate, choose your parent entity jurisdiction based on tax treaties and contract enforcement, and build transfer pricing documentation from day one. Draft contracts that specify governing law, dispute resolution, currency terms, and intellectual property ownership with precision, then validate your structure with local counsel in each major jurisdiction. Hire advisors who understand both the legal requirements and the cultural norms of your target markets, because these steps cost money upfront but save multiples of that cost when disputes or audits arrive.

At Primum Law Group in San Francisco, we work with startups and growing companies to structure international corporate law arrangements that survive regulatory scrutiny and scale efficiently. We handle international corporate structuring, tax planning, and cross-border transactions so you can focus on building your business. A sustainable global strategy requires ongoing oversight-assign one person accountability for compliance in each jurisdiction, maintain a regulatory calendar, and review your transfer pricing documentation annually.