Selling a business is one of the biggest financial decisions you’ll make. Without proper exit strategy planning, you risk leaving money on the table or facing unexpected complications when the time comes.

At Primum Law Group, we’ve seen countless business owners scramble because they waited too long to prepare. The owners who succeed are those who map out their exit years in advance, align their finances, and understand their options.

Why Exit Planning Can’t Wait

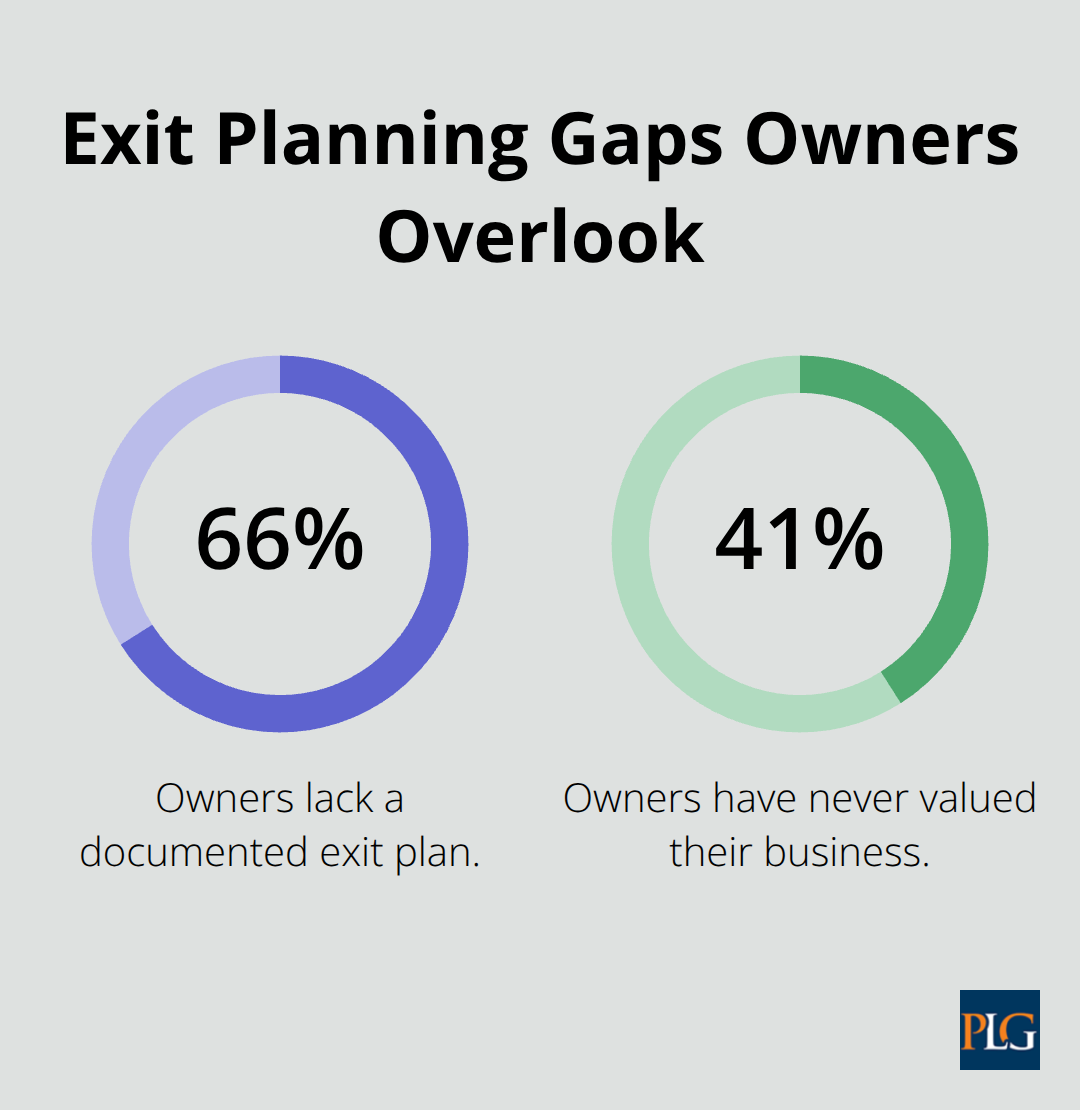

Most business owners treat exit planning like retirement planning-something to handle eventually. The reality is far harsher. According to the Exit Planning Institute, 66% of owners lack a documented exit plan, and 41% have never valued their business. This negligence costs real money.

A business without clear exit preparation typically sells for 20-30% less than one with proper groundwork, simply because buyers perceive higher risk and integration challenges. The gap between a rushed sale and a strategic one often amounts to hundreds of thousands of dollars that owners leave behind.

Building Value Takes Years, Not Months

The most actionable insight we can offer is this: start exit planning three to five years before your target exit date. This timeline matters because buyers evaluate specific metrics, and improving them requires sustained effort. They examine EBITDA multiples-mid-market businesses typically command 4-6x multiples, while high-growth tech companies reach 10-15x. To hit those multiples, you need audited financial statements, documented operational procedures, and demonstrated independence from yourself as the owner.

A business that relies entirely on you is worth less because the buyer inherits transition risk. Normalizing your financials by removing discretionary expenses and above-market owner compensation reveals the true earning power. If you’ve been running personal expenses through the business or taking inflated salary, buyers will adjust your valuation downward. Starting early gives you time to clean these items without raising red flags.

Timing Compounds Your Negotiating Power

Strategic buyers and private equity firms dominate 85% of recent exits. Strategic buyers pay premiums for synergies-they can integrate your operations, eliminate redundancy, and cross-sell to their existing customers. Private equity typically operates on a 3-7 year horizon and often expects the owner to stay involved during transition. Neither group will accept a business with messy records, concentrated customer bases, or unclear contracts.

If you have just one customer representing 40% of revenue, that’s a valuation killer. Diversifying your customer base across multiple segments and geographies takes time. Building recurring revenue through contracts or subscriptions requires product development and sales cycles. Assembling a capable management team with documented processes reduces owner dependence-a critical value driver. These improvements compound when you start early.

Waiting until you need the exit forces you to sell on the buyer’s timeline, in their market conditions, at their valuation. Starting years ahead lets you control the narrative and present a business that’s genuinely attractive, not desperate. The next section explores the specific components that separate a strong exit strategy from one that leaves value on the table.

Building the Foundation for a Smooth Exit

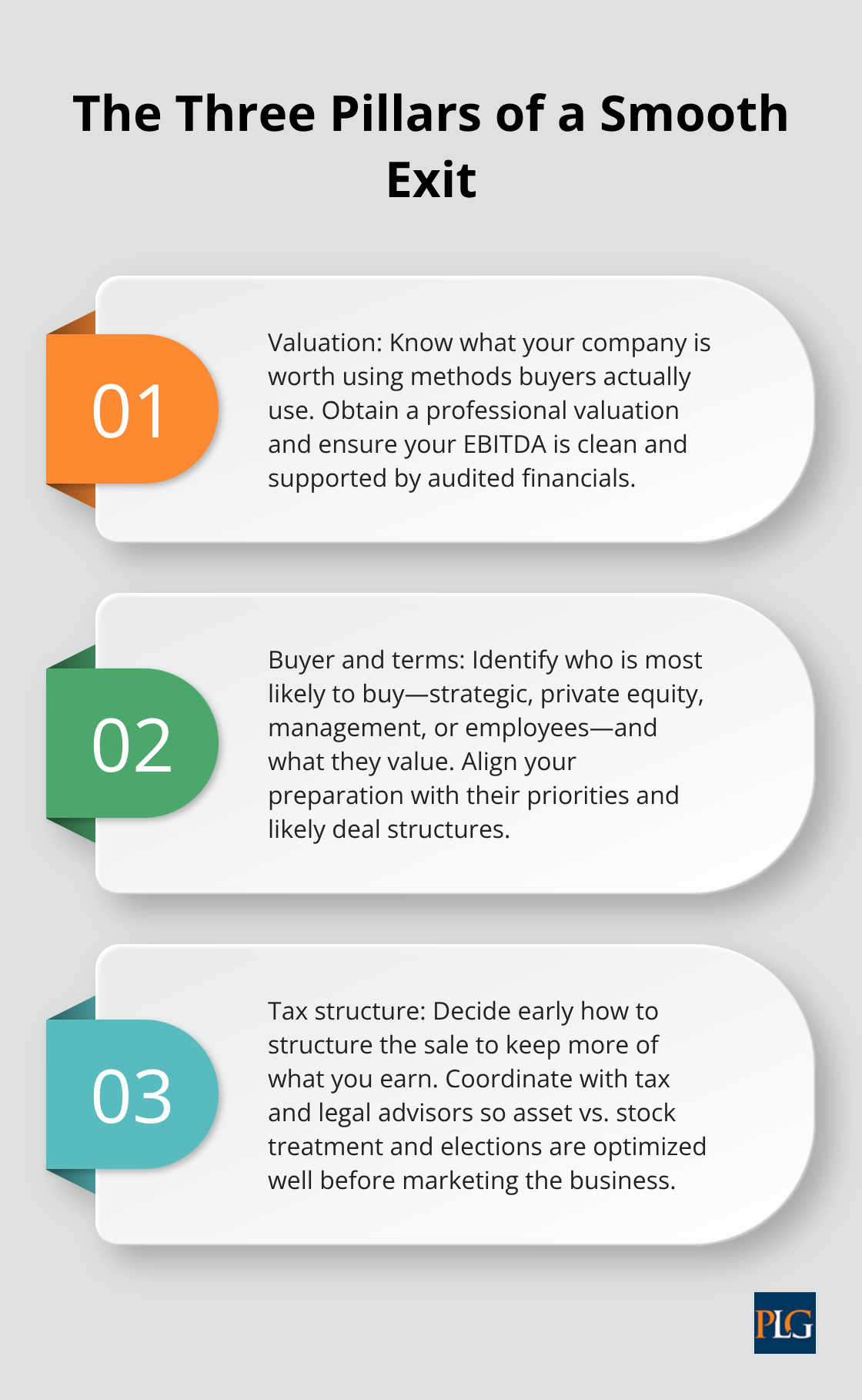

A solid exit strategy rests on three interconnected pillars: knowing what your business is actually worth, understanding who will buy it and on what terms, and structuring the deal so taxes don’t consume half your proceeds. Most owners treat these as separate tasks when they should be integrated from the start. Your financial preparation directly influences buyer interest, which shapes deal structure options, which determines your tax bill.

Skipping any step creates friction that costs money and extends timelines.

What Your Financials Must Show

Buyers spend 30-90 days verifying every revenue line, contract, and expense claim during due diligence. If your records are incomplete or inconsistent, they’ll either walk away or demand a price reduction to cover the risk of hidden liabilities. Obtain a professional valuation using methods that buyers actually use: EBITDA multiples, discounted cash flow analysis, or asset-based approaches depending on your industry. Mid-market businesses typically trade at 4-6x EBITDA, but that multiple only applies if your numbers are clean and audited. Many owners discover their valuations drop 15-25% when they normalize EBITDA by removing discretionary expenses and owner compensation that a buyer won’t inherit.

Get audited financial statements prepared now, not three months before you market the business. Prepare a virtual data room with organized contracts, customer agreements, vendor relationships, insurance policies, and tax returns. Buyers expect this level of organization, and having it ready signals professional management. Document your standard operating procedures for every critical function-if the business depends entirely on your knowledge, buyers treat it as a single-person risk and discount accordingly.

Identifying the Right Buyer Changes Everything

Strategic buyers and private equity firms account for over 85% of business exits. Strategic buyers look for synergies-they’ll pay premiums if your business fills a gap in their product line, expands their geographic footprint, or gives them access to your customer base. Private equity buyers focus on growth potential and cash flow, typically planning a 3-7 year hold before their own exit. Management buyouts work when key employees have both the capability and financing access to take ownership. ESOPs provide a tax-efficient path if you want to exit gradually while keeping the business employee-owned.

Each buyer type values different things. A strategic buyer cares about revenue concentration risk; if 40% of your revenue comes from one customer, they’ll demand a steep discount. A private equity firm cares about growth trajectory and management depth. Start relationship-building with potential acquirers two to three years before your target exit, even informally. Industry conferences, trade associations, and your professional network reveal who’s actively acquiring in your space. When the time comes to formally market the business, you’ll have multiple interested parties rather than desperately hoping someone appears.

Tax Structure Determines What You Actually Keep

The difference between an asset sale and a stock sale can amount to hundreds of thousands of dollars in tax liability. Asset sales allow buyers to depreciate acquired assets and often produce favorable tax outcomes for them, but they’re typically less favorable for you as the seller because different asset categories receive different tax treatment. Stock sales let you potentially qualify for capital gains rates, but buyers prefer asset sales and will discount their offer accordingly.

If you operate as an S corporation, a 338(h)(10) election may allow you to be taxed as an asset sale while still selling stock, but this requires coordination between buyer and seller and detailed tax planning. Installment sales spread your gain across multiple years, potentially lowering your tax bracket and managing capital gains. Consult a tax professional and your legal team at least eighteen months before exit to prevent surprises. Structure decisions interact with your business form, the purchase price allocation, and whether you’ll stay involved post-closing. These choices compound in importance; a poorly structured deal can cost more in taxes than you saved in negotiating the purchase price.

The mechanics of your exit-who buys, how they buy, and what structure you choose-all hinge on preparation work that starts well before you market the business. The next section examines the specific exit paths available and when each one makes sense for your situation.

Which Exit Path Fits Your Timeline and Goals

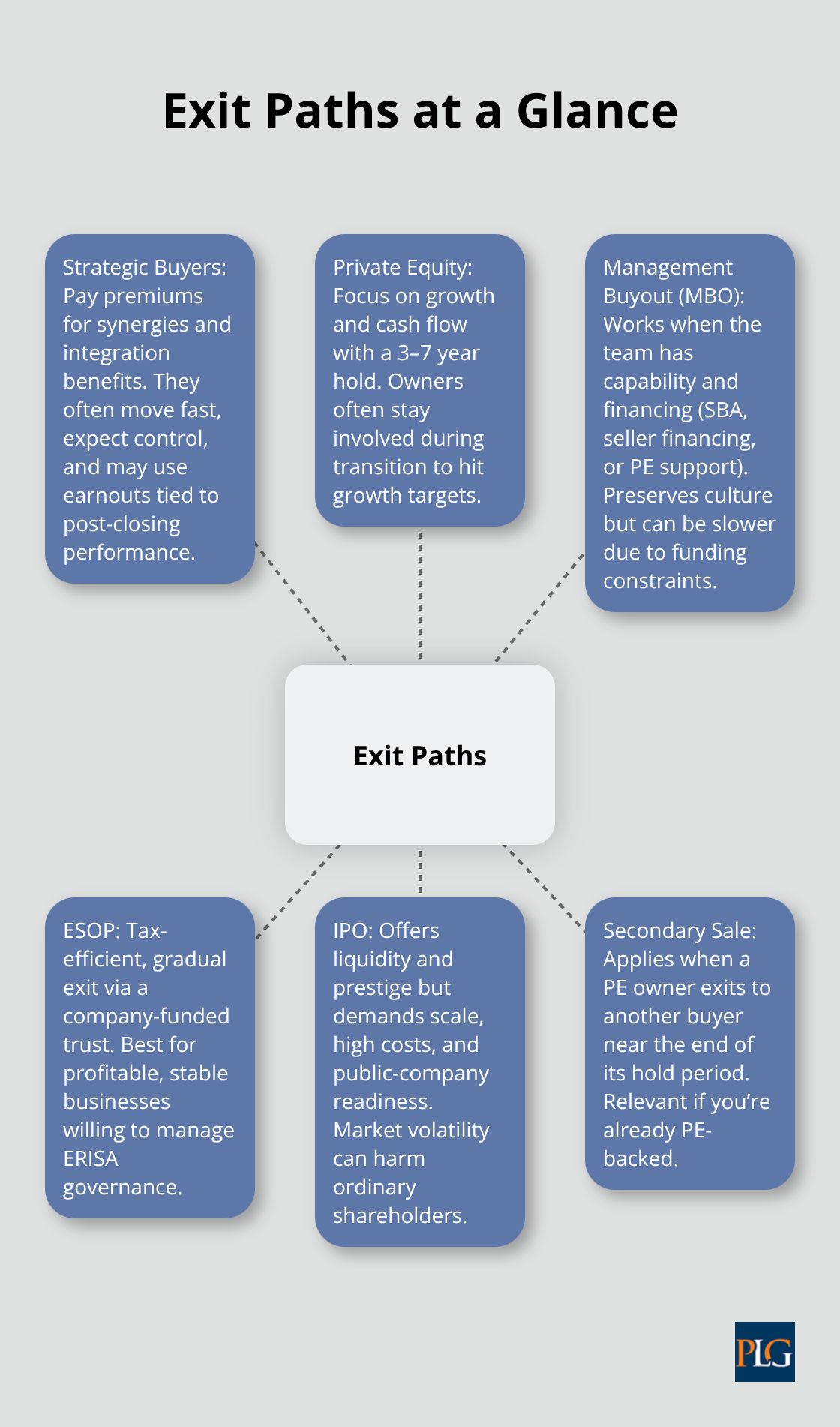

Strategic acquisitions, management buyouts, and public offerings represent fundamentally different paths forward, each with distinct timelines, financial outcomes, and control implications. Your choice depends less on what sounds appealing and more on what your business can actually support and what you need from the exit. Strategic buyers move fastest but demand control. Private equity operates on longer timelines with growth expectations. Management buyouts preserve culture but create financing constraints. ESOPs offer gradual exits with tax advantages. IPOs deliver prestige and liquidity but require scale most private companies lack, and the volatility can devastate ordinary shareholders during downturns. The Exit Planning Institute research shows that strategic acquisitions and private equity transactions account for over 85% of actual exits, which tells you where the real liquidity lives.

Strategic Buyers Pay for What They Can Integrate

A strategic buyer writes the largest check when they see operational synergies, customer access, or geographic expansion. They’ll pay 4-6x EBITDA for a mid-market business, sometimes higher if you fill a critical gap in their product line or customer base. The catch is speed and control. They move quickly because integration timelines matter to their stakeholders, and they’ll demand earnouts tied to post-closing performance to protect against revenue loss during transition. If your largest customer represents 40% of revenue, they’ll discount aggressively because customer concentration creates integration risk. They’ll also want you involved during transition, typically 6-18 months, with clawback provisions if revenue drops. This path works best if you have clean financials, documented processes, and a diversified customer base. Strategic buyers evaluate fit constantly; when conditions align, they move from conversation to letter of intent in weeks. Start those conversations 18-24 months before your target exit date if you’ve spent years building relationships with industry peers or larger competitors.

Management Buyouts and ESOPs Require Different Financing

A management buyout happens when your key employees have both the capability and access to capital to acquire the business. This typically requires an SBA loan, seller financing, or private equity backing, which means your management team must qualify for debt. If your business generates $2 million in annual EBITDA and your COO wants to buy it at a 5x multiple, that’s a $10 million acquisition. Your COO needs to cover 20-30% down payment from personal capital, then service $7-8 million in debt. Most don’t have that capacity unless private equity co-invests. ESOPs work differently. You sell shares to an ESOP trust funded by company debt, which creates a tax-deductible contribution and lets you defer capital gains if you reinvest proceeds in qualifying securities. The business repays the ESOP debt from cash flow while employees gradually accumulate ownership. ESOPs work best for profitable, cash-generative businesses with stable revenue and a committed employee base. They preserve company culture and employee continuity, but they require sophisticated governance and ERISA compliance. Both paths take longer than strategic sales-typically 12-24 months for structuring, financing, and execution. They make sense if you want to preserve the company’s independence or reward loyal employees, but they won’t deliver the speed or valuation multiples that strategic buyers offer.

IPOs and Secondary Sales Demand Scale Most Owners Lack

An initial public offering requires revenue typically exceeding $100 million, predictable growth, and a management team that can operate under public company scrutiny. The underwriting process takes 6-12 months, regulatory costs run $5-10 million, and ongoing compliance creates permanent overhead. Most private businesses don’t meet these thresholds, and those that do often find the IPO market volatile. Investopedia research shows that IPOs can be attractive for prestige and liquidity but create volatility that ordinary investors find painful. Secondary sales-where a private equity firm exits to another buyer-happen when the first investor’s hold period ends, typically 3-7 years. This path only applies if your business already has private equity ownership and you’re a minority shareholder or employee. For owner-operators planning a first exit, IPO and secondary sale are rarely realistic options. Focus instead on the paths where your business actually qualifies: a strategic acquisition if you have clean financials and market fit, a management buyout if your team can finance the transaction, or an ESOP if you want a gradual exit with tax efficiency.

Final Thoughts

Exit strategy planning isn’t something you finish and file away. It evolves as your business grows, market conditions shift, and your personal goals change. The owners who walk away with the largest checks aren’t the ones who stumble into a buyer at the last minute-they’re the ones who spent years building financial credibility, diversifying their customer base, and assembling a management team that functions without them. These improvements compound, and a business that generates clean audited financials, operates with documented procedures, and demonstrates recurring revenue commands higher valuations across every buyer type.

The timeline matters more than you think. Starting your exit strategy planning three to five years before your target exit date gives you time to normalize your financials, address operational weaknesses, and build relationships with potential buyers. Waiting until you need the exit forces you to accept whatever terms appear in whatever market conditions exist at that moment, and you lose negotiating power when buyers sense desperation.

Your legal and financial advisors should be involved from the beginning, not brought in when you’re ready to sign documents. A tax professional can structure your deal to minimize capital gains exposure, a business attorney can review contracts and identify liability risks, and a financial advisor can align your exit proceeds with retirement planning. We at Primum Law Group work with business owners on the legal and structural aspects of exits, from deal documentation to corporate governance and compliance preparation, and you can reach out to learn how we support business transitions.