Venture capital contracts are the backbone of startup funding, yet many founders and investors approach them without a clear roadmap. A poorly drafted venture capital contract sample can cost you thousands in legal fees or worse-leave your interests unprotected when disputes arise.

At Primum Law Group, we’ve seen firsthand how the right contract structure makes the difference between smooth funding rounds and costly complications. This guide walks you through the essential components, legal requirements, and common mistakes that could derail your VC deal.

What Should a Venture Capital Contract Actually Include

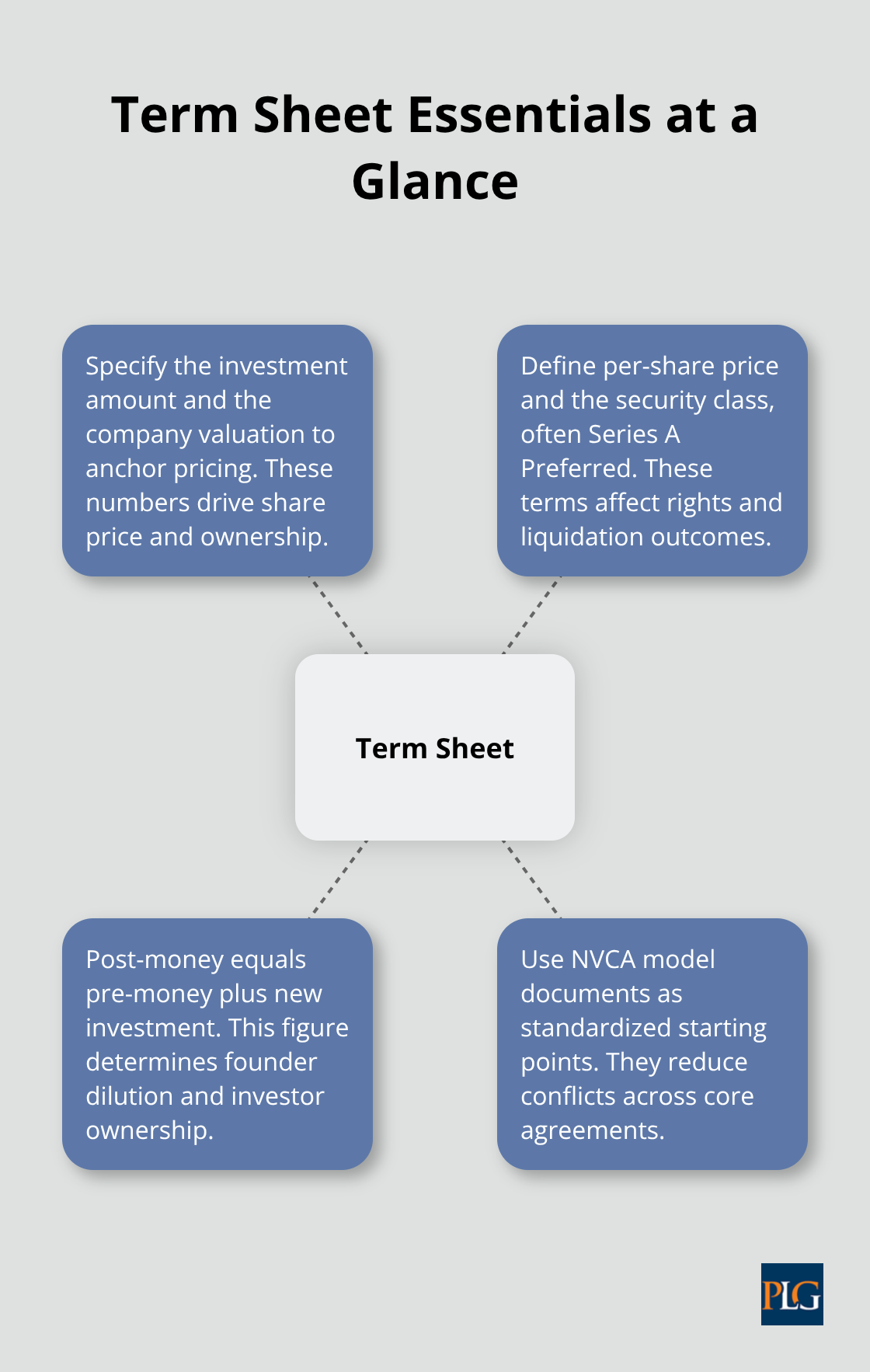

The Term Sheet Foundation

A venture capital contract starts with the term sheet, a non-binding document that outlines the basic framework before lawyers draft binding agreements. Most term sheets run under 10 pages and establish the foundation for everything that follows. The term sheet specifies the investment amount, company valuation, share price, and share class, typically Series A Preferred stock. Post-money valuation is the critical number here-it equals pre-money valuation plus the new investment. If an investor puts $8 million into a company with a $19 million pre-money valuation, the post-money is $27 million, and the investor owns roughly 30 percent.

This math directly determines founder dilution, so getting the valuation right matters enormously.

The NVCA model documents, updated in October 2025, provide standard starting templates that most investors expect founders to use. These templates include the Certificate of Incorporation, Stock Purchase Agreement, Investors’ Rights Agreement, and Voting Agreement, all designed to work together without internal conflicts.

Liquidation Preferences and Anti-Dilution Protection

Liquidation preference is the clause that actually dominates investor returns in an exit. A 1x non-participating preference means investors get their money back first, then common shareholders split what remains-this is standard and reasonable. A full ratchet anti-dilution provision punishes founders harshly in down rounds by resetting the investor’s share price downward, while a weighted-average approach is fairer and more common in 2026 deals.

Anti-dilution protection kicks in if a future round values the company lower. Pay-to-play provisions can strip anti-dilution rights from investors who skip subsequent rounds. These terms protect investors but can handcuff founders, so negotiate hard on the scope and conditions.

Board Composition and Investor Rights

Board composition matters just as much as economics. Try for an odd number of directors, typically three or five, with at least one independent member who isn’t affiliated with the founder or investor. Investors will demand information rights, including quarterly financials and annual audited statements, plus the right to participate in future funding rounds to maintain ownership.

Pro rata rights let investors buy shares in the next round proportional to their current stake. These provisions shape how much control investors retain and how much flexibility founders preserve for future capital raises. The balance you strike here determines whether your cap table remains manageable or becomes locked down by protective provisions that require investor approval for major business decisions.

What You Must Know About VC Contract Compliance in San Francisco

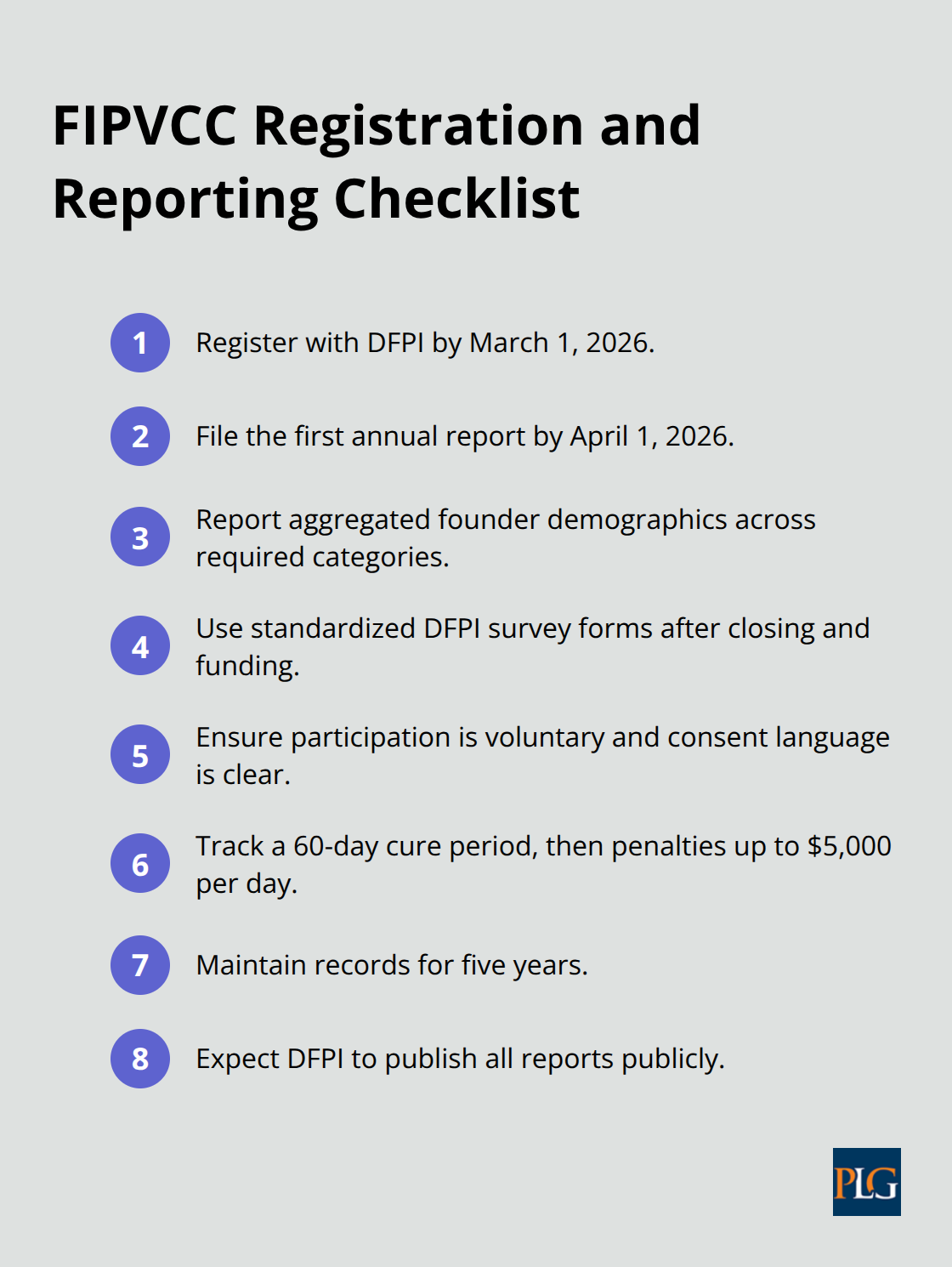

California’s New Registration Requirements

California’s Financial Innovation and Privacy Venture Capital Company Registration Act fundamentally changes how you structure VC contracts starting March 1, 2026. The law requires any venture capital firm with a California nexus to register with the California Department of Financial Protection and Innovation and file annual reports disclosing founder demographic data. This applies broadly-if you invest in California-based startups or solicit money from California residents, you fall under FIPVCC rules even if your fund operates elsewhere. The definition of venture capital investment is expansive: it includes any securities purchase where you gain management rights to influence operations or business objectives, capturing growth equity funds, corporate venture arms, and some family offices that traditionally avoided VC classifications.

Registration and Reporting Deadlines

Registration itself is straightforward and costs at least $175, but the annual reporting requirement is where complexity emerges. You must register by March 1, 2026, and file your first annual report by April 1, 2026. Beginning April 1, 2026, you must report demographic data for founding teams across your portfolio, including gender identity, race and ethnicity, disability status, LGBTQ+ identification, veteran status, and California residency. The data must be aggregated and anonymized-you collect it after the investment agreement closes and funds transfer, using standardized DFPI survey forms, and participation is voluntary for founders.

Failure to file by April 1 triggers a 60-day cure period, then civil penalties up to $5,000 per day, with higher penalties for knowing violations. You must maintain all records for five years, and the DFPI publishes all reports publicly.

Building Compliance Into Your Workflows

This regulatory shift forces you to build demographic data collection into your closing workflows now. Design your investment agreements to include clear consent language explaining that founder surveys are voluntary and responses will be aggregated and anonymized. Implement a secure data-handling process that separates demographic responses from founder identities and stores them separately. Many founders worry about privacy, so transparency about how you use the data builds trust. The broad California nexus standard means most active VC firms will register regardless of headquarters location-the DFPI hasn’t issued detailed guidance on terms like significant presence or operational office, so assume you’re covered if you have any meaningful California activity.

Practical Steps for Compliance

Assign a compliance point person to manage DFPI reporting and regulatory inquiries, keep your cap table updated in real time to track portfolio companies and investment amounts by calendar year, and establish a compliance calendar with reminders for March 1 registration and April 1 annual reports. Public disclosure of your founder diversity metrics will influence how limited partners and entrepreneurs perceive your fund, making data accuracy and timely filing non-negotiable. These compliance obligations directly shape how you draft your investment agreements and structure your post-closing processes, which means your VC contracts must now account for regulatory requirements that didn’t exist before 2026.

What Kills VC Deals Before They Close

Vague Language Creates Expensive Disputes

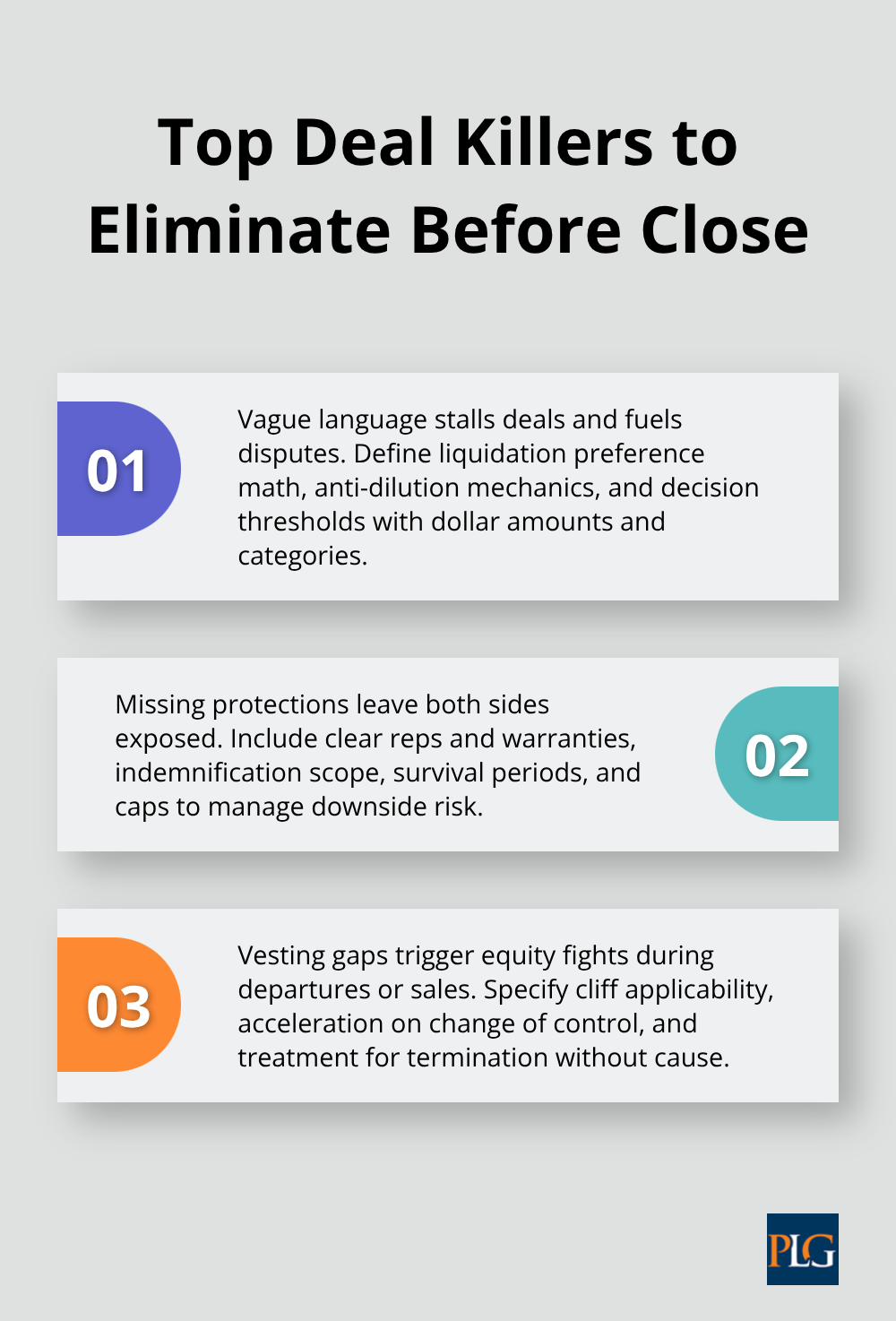

Vague language in venture capital contracts creates disputes that neither founders nor investors want to fight. Deals stall for months when liquidation preference calculations lack precise definitions, anti-dilution mechanics leave room for interpretation, or board approval thresholds remain ambiguous. A term sheet that states investors need board approval for major decisions sounds protective until you realize the contract never defines what counts as major. Does hiring a VP of Sales require approval? Changing accounting firms? Buying new office equipment? Without specific thresholds tied to dollar amounts or strategic categories, arguments erupt when speed matters most.

The model documents include detailed definitions for exactly this reason, but many founders skip the commentary sections that explain why precision matters. If your contract fails to specify that board approval applies only to decisions exceeding $500,000 in annual expense impact or equity issuances above 5 percent of outstanding shares, you’ve left a landmine in your cap table. One founder spent $15,000 in legal fees resolving a dispute over whether a Series B financing required investor consent under a protective provision that never actually named Series B financing specifically.

Missing Protections Leave Both Parties Exposed

Inadequate downside protection appears when either party assumes the other won’t exercise their rights. Investors often skip detailed reps and warranties in early-stage deals, telling themselves the company is too young to harbor hidden liabilities, then discover undisclosed IP disputes or regulatory violations during due diligence. Founders frequently accept vague indemnification language that exposes them personally to investor losses, not realizing they remain on the hook for claims years after they’ve left the company.

Missing contingency clauses create real problems when circumstances shift. A term sheet signed in January that doesn’t address what happens if a key engineer leaves before closing, or if revenue drops 40 percent before fund transfer, gives both parties ammunition for renegotiation or walkaway claims. Build in specific conditions precedent tied to measurable metrics: if monthly recurring revenue falls below X, if more than one C-level executive departs, or if a material customer contract terminates, either party can renegotiate terms or exit cleanly.

Vesting Schedules That Lack Critical Details

Sloppy vesting schedules create problems that hit hardest when someone leaves early or a sale happens unexpectedly. A four-year vest with a one-year cliff is standard, but contracts often fail to specify whether the cliff applies to options only or restricted stock, whether acceleration occurs on change of control, or how much vests if a founder faces termination without cause. These gaps leave founders vulnerable to disputes over equity ownership when transitions occur.

California’s new FIPVCC registration requirements add another layer-your contracts must now document founder demographic data collection and consent clearly, or you’ll face compliance gaps when April 2026 reporting arrives. The difference between a well-drafted vesting schedule and a careless one determines whether founders retain fair equity treatment or lose thousands in unvested shares during unexpected departures.

Compliance Gaps in Modern VC Contracts

Contracts that ignore California’s FIPVCC requirements create serious problems for venture capital firms operating with any California nexus. Your investment agreements must include clear consent language explaining that founder surveys are voluntary and responses will be aggregated and anonymized. Without this documentation, you’ll struggle to collect the demographic data required for April 2026 reporting, and your compliance record will show gaps that regulators notice.

The broad California nexus standard means most active VC firms must register regardless of headquarters location. If you invest in California-based startups or solicit money from California residents, FIPVCC rules apply to you. Your contracts must account for these regulatory requirements now, not after registration deadlines pass and penalties accumulate.

Final Thoughts

A strong venture capital contract sample protects both founders and investors by establishing clear expectations before disputes arise. The essential elements we’ve covered-precise term sheet language, defined liquidation preferences, transparent board composition, and compliant demographic data collection-form the foundation of deals that close smoothly and scale successfully. Vague definitions, missing contingencies, and overlooked regulatory requirements create friction that costs time and money when you can least afford it. California’s FIPVCC registration requirements, evolving anti-dilution standards, and the need to balance founder flexibility with investor protection mean that template documents alone won’t suffice for most deals.

You need counsel who understands both the economics driving your negotiation and the regulatory landscape shaping your obligations. We at Primum Law Group work with founders and investors throughout San Francisco and Silicon Valley to translate term sheets into binding agreements that actually work. Our team handles venture capital and private equity transactions, startup counseling, and corporate governance matters that keep your cap table clean and your compliance record solid.

Your next step is straightforward: gather your term sheet, review it against the NVCA model documents, and identify the specific terms that matter most to your deal. Then reach out to experienced legal counsel who can tailor a venture capital contract to your facts and jurisdiction. The investment in proper documentation now pays dividends when you’re raising your next round or navigating an exit.