Finding the right venture capital partner can make or break your startup’s trajectory. At Primum Law Group, we’ve seen countless founders struggle to identify a venture capital example that actually matches their business stage and goals.

The difference between approaching the wrong VC firm and the right one often determines whether you get funded or face rejection. This guide walks you through exactly what investors look for, where to find them in San Francisco, and how to evaluate whether they’re truly the right fit for your company.

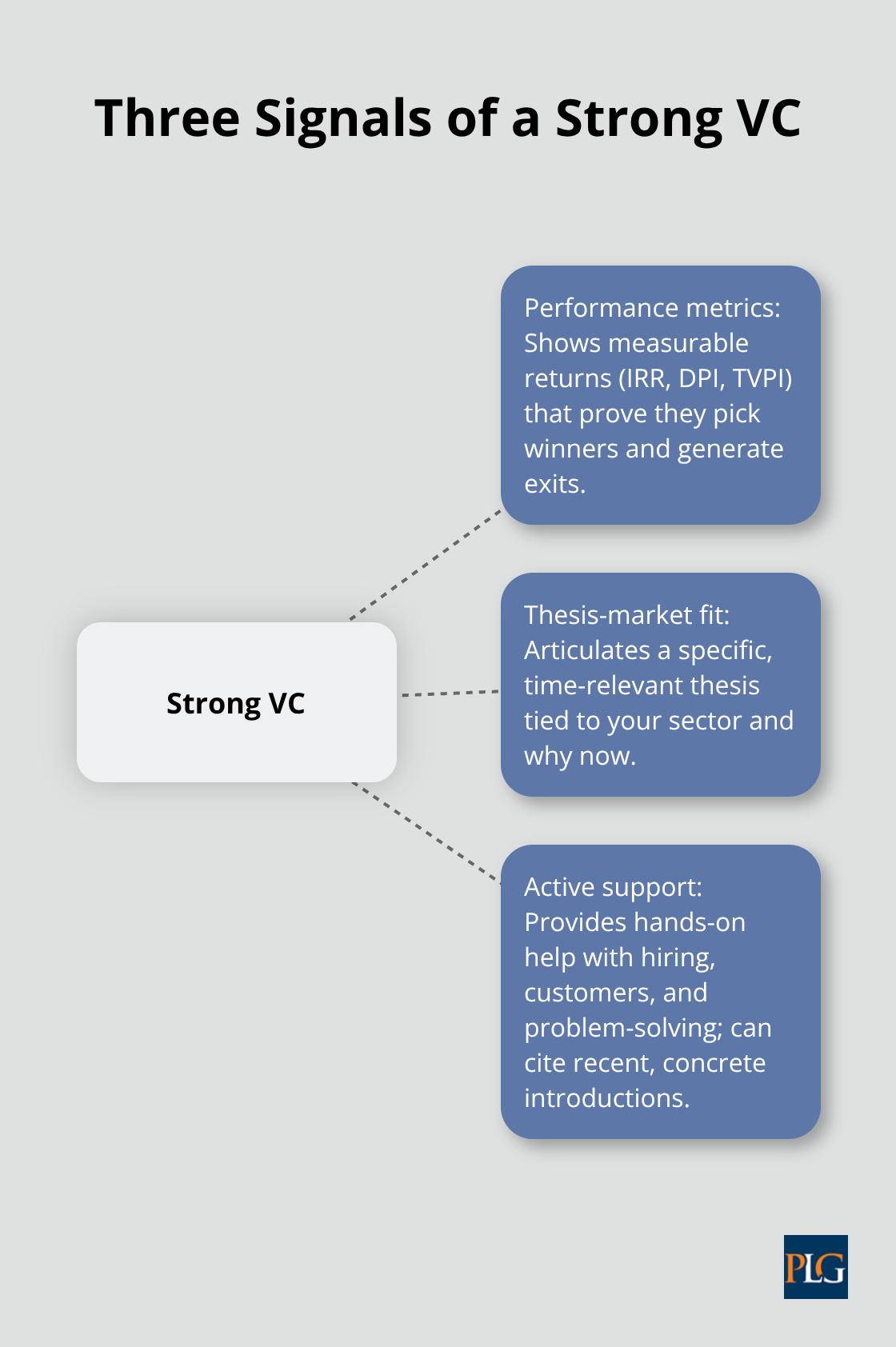

What Separates Strong VCs From the Rest

Performance Metrics Reveal True Track Records

VCs are not all equal, and the metrics they brag about often hide critical weaknesses. Most founders fixate on brand names and fund size, then wonder why their chosen investor adds little value beyond a check. Strong venture investors demonstrate three concrete signals: measurable returns on past investments, a clear thesis for why they back companies in your sector, and a track record of rolling up their sleeves to support portfolio companies through real challenges.

Start by examining actual performance data rather than marketing language. Look at IRR (Internal Rate of Return), which measures the speed of returns from a fund’s investments. Top-quartile funds typically achieve IRRs above 20%, while 15–20% is solid and anything below 10% raises serious questions about fund quality. Beyond IRR, check DPI (Distributions to Paid-In), which tracks realized cash returns. A DPI above 1.5x indicates the fund has actually returned cash to its investors, not just held paper gains. TVPI (Total Value to Paid-In) combines realized and unrealized value, and funds above 2.0x perform well. These metrics matter because they reveal whether the fund’s leaders can actually pick winners and navigate exits. A VC claiming success but showing a 0.8x DPI is still fishing for their next job with your capital.

When evaluating funds, cross-reference their portfolio against public exits. If a firm claims fintech focus but their exits are primarily in consumer apps, their stated thesis doesn’t match their results. Sequoia’s track record with PayPal and Square illustrates what real fintech conviction looks like. Accel’s $17.06 billion in assets and consistent follow-on funding patterns show a firm with staying power to support companies through multiple rounds. NEA’s $9.25 billion fund size enables them to lead substantial rounds and allocate capital to future funding. Look beyond press releases to see whether the fund actually invested in companies solving problems similar to yours, and whether those companies achieved meaningful traction or exits.

Investment Thesis Must Connect to Market Reality

The second signal is a genuine investment thesis tied to market realities, not generic sector language. A VC saying they focus on AI is worthless; a VC explaining why they believe autonomous supply-chain optimization will capture $50 billion in value over the next decade is specific and credible. Their thesis should explain the market problem, why it’s solvable now (not five years ago or five years from now), and how they plan to identify winning companies before competitors do.

When you speak with potential investors, ask them to articulate their thesis in concrete terms. If they struggle or resort to buzzwords, move on. A fund that invests across all stages but shows no clear pattern in how they support early-stage companies is likely spreading capital too thin to help you meaningfully.

Active Support Beyond the Check Matters Most

The third signal is evidence that they actively support portfolio companies beyond writing checks. Greylock’s investments in Workday and Wealthfront reflect a pattern of companies that scaled significantly after funding, suggesting operational help and network access were real. Ask potential investors for specific examples of how they’ve helped companies in your space reach product-market fit, hire key executives, or land first customers. A VC who can name three concrete introductions they made this month is more valuable than one who vaguely promises to help.

Ask for references from their portfolio founders, not the cherry-picked success stories. Call the founders of companies that didn’t exit and ask whether the VC was helpful during tough periods. That conversation reveals whether the partner genuinely cares about your success or just wants to appear on your cap table. Once you’ve identified firms that pass these three tests, you’re ready to research where they operate and how to approach them strategically.

Finding VC Firms in San Francisco

San Francisco hosts the densest concentration of venture capital in North America, with firms like Accel, NEA, Sequoia, and Andreessen Horowitz controlling over $33 billion in combined assets. This density creates both opportunity and noise. Most founders waste months chasing the wrong funds because they rely on outdated lists or generic databases. The reality is that VCs rarely fund cold outreach. Warm introductions close deals; cold emails get deleted.

Map Funds That Invested in Your Space

Start with a specific strategy: identify funds that have invested in companies solving your exact problem. If you’re building fintech infrastructure, pull the portfolios of funds that backed companies like PayPal or Square and track who led those rounds. Crunchbase and PitchBook let you filter by sector, stage, and geography, but these tools only work if you know what to search for.

Spend a week building a target list of 15 to 20 funds that deployed capital in your space within the last two years. This eliminates funds that claim focus but haven’t invested recently and saves you from pitching to firms that don’t fund your stage. Once you have the list, dig into each fund’s recent announcements and identify the partners who led deals. Those partners are your actual targets, not the fund brand.

Leverage Networks and Strategic Events

Networks and events accelerate introductions far faster than cold outreach. Y Combinator companies report that roughly 40 percent of their seed funding comes from investors they met through the program or its alumni network, not from general fundraising outreach. If you’re not in a formal program, attend sector-specific events where investors actively scout.

VentureBeat events, TechCrunch Disrupt, and industry conferences attract fund managers actively looking to deploy capital. Skip generic networking events; attend ones tied to your vertical. A fintech founder belongs at FinTech Summit, not at a general startup mixer. Leverage LinkedIn to identify connections at target funds. If someone in your network knows a partner at Greylock or Redpoint, ask for a warm introduction immediately. That introduction, even from a tangential connection, converts to meetings at rates 5 to 10 times higher than cold email.

Use Portfolio Companies as Bridges

If no direct connection exists, find someone who works at a portfolio company of your target fund and ask them to facilitate an introduction. Portfolio company employees often maintain stronger relationships with their investors than founders do. This path opens doors that cold outreach cannot.

Attend demo days and pitch competitions where funds send scouts. These events let you pitch in front of multiple investors simultaneously, and the competitive format often triggers faster decision-making than traditional one-on-one meetings. The partners you meet at these events have already signaled they’re actively looking to deploy capital, which means your pitch lands at the right moment.

Identify the Right Partner Within Each Fund

Once you secure a meeting, confirm you’re speaking with the actual decision-maker. Large funds like Accel and NEA have multiple partners with different sector focuses and stage preferences. A partner who leads Series A rounds in enterprise software won’t move fast on your seed-stage consumer app. Ask the person who schedules your meeting which partner leads investments in your sector and stage. This simple question prevents wasted pitches to the wrong person inside the right fund.

The firms that have actually invested in your space recently have already proven they understand your market. They’ve made bets, learned from those bets, and built relationships with founders and operators in your sector. These are the only funds worth pursuing. Once you’ve identified your target partners and secured initial meetings, the next step is evaluating whether they’re truly aligned with your company’s needs and stage.

How to Evaluate and Approach the Right VC Firm in San Francisco

Match Fund Stage to Your Company Stage

Fund size and stage preference are not marketing details. They determine whether a partner can actually write you a check and whether they have bandwidth to support your company. A seed fund with $50 million in assets operates under completely different constraints than a $5 billion growth fund. Seed funds typically deploy $500,000 to $2 million per company, while Series A funds deploy $3 million to $15 million, and growth funds deploy $25 million or more. If you’re raising $1 million and pitch a growth fund that writes minimum checks of $25 million, you waste their time and yours. The partner will either pass immediately or try to force you into a larger round before you’re ready, which weakens your negotiating position and burns capital inefficiently.

Start by confirming the fund’s typical check size and the stage they actually fund. Don’t rely on their website; ask the person scheduling your meeting directly. A partner who leads Series A rounds at NEA’s $9.25 billion fund moves at a different pace than a partner at a $300 million seed fund like 500 Startups. The larger fund often takes longer to decide because they have more capital to deploy and less urgency to close individual deals. Smaller funds move faster because they need to deploy capital within specific timelines. If you need funding within 60 days, a seed-stage fund with capital ready to deploy beats a mega-fund that operates on 90-day diligence cycles.

Equally important is confirming whether the fund has actually invested at your current stage recently. Pull their last five investments and check the funding rounds they led. If a fund claims to do seed investing but their last five deals were all Series B or later, they’ve shifted strategy and won’t move fast on early-stage companies regardless of what their website says. Funds that have invested in companies at your exact stage within the past 12 months have already built processes, relationships, and conviction in that stage. They move quickly and understand your metrics and challenges.

Assess Values and Operations for Real Partnership Potential

Cultural fit sounds vague, but it’s concrete and measurable. It means: Does this fund invest for the long term or push for quick exits? Do they support founders during downturns or disappear when times get tough? Do they add value through introductions and operational guidance or just take board seats? The best way to assess this is to call three founders in their portfolio and ask specific questions. Don’t ask if they like their investor; ask whether the investor made introductions that generated revenue, whether they helped recruit key hires, and whether they remained engaged during difficult periods. A founder who hesitates or gives vague answers is telling you something important.

Red flags include funds that charge monitoring fees beyond standard carry, funds that push for participating preferred stock beyond 1x unless justified by extreme dilution, and funds that rush you through due diligence without asking tough questions. A VC that doesn’t challenge your assumptions is either not serious or not competent. The best investors ask hard questions and push back on weak logic. They want to find fatal flaws before they invest, not after.

Ask potential investors about their reserve strategy. Many funds allocate roughly half their capital to follow-on rounds for existing portfolio companies. If a fund invested in you but allocated minimal reserves, they can’t support you through subsequent rounds, which means you’ll face dilution from other investors or fail to raise at all. Confirm they have capital committed to follow-on funding before signing term sheets. Also assess decision-making speed and transparency. Some funds make decisions in two weeks; others take three months. If a fund is slow to decide on diligence questions or vague about their process, they’ll be slow to help when you need fast decisions during business challenges. A fund that moves decisively and communicates clearly about timelines and next steps operates with founders, not against them.

Prepare Pitch Materials That Prove Traction

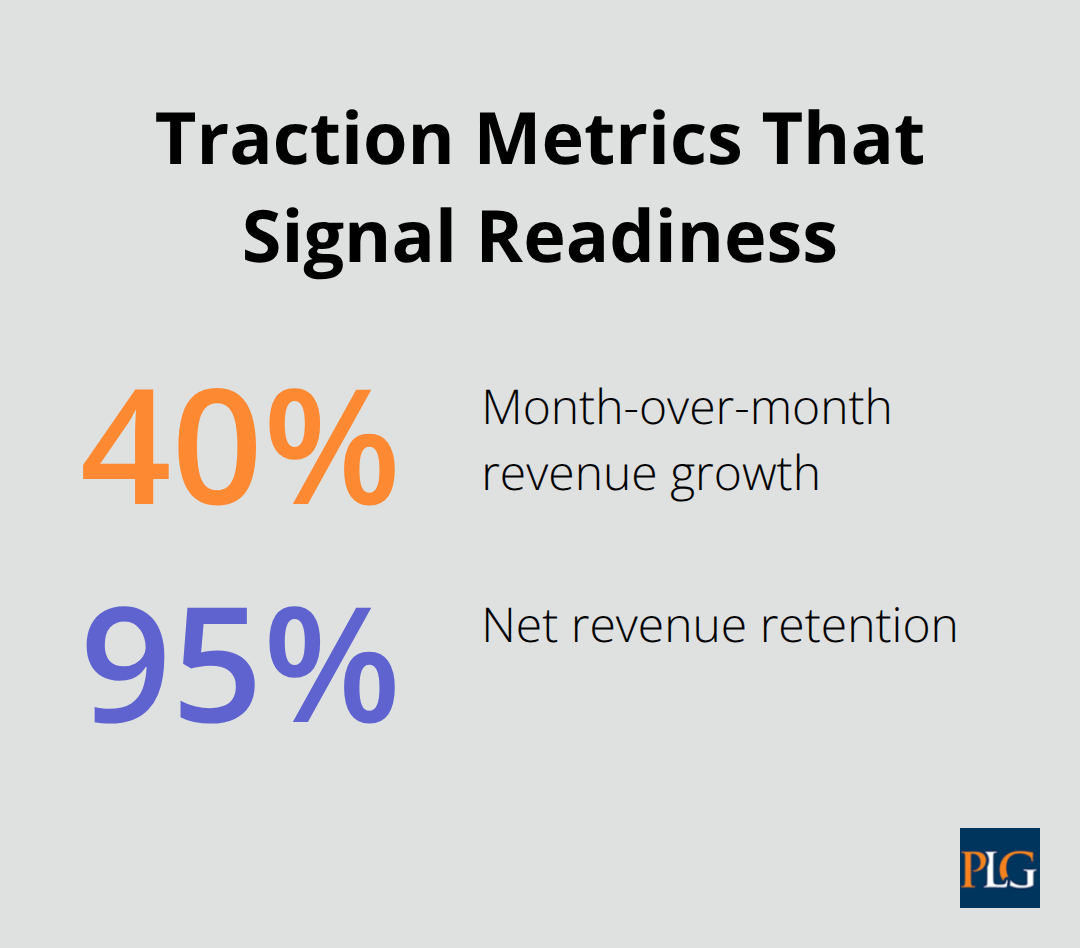

Your pitch deck and supporting materials should demonstrate traction, not potential. VCs have heard thousands of pitches about massive markets and visionary founders. They fund companies with evidence of traction: customers paying for your product, retention metrics showing people value what you built, or growth rates that prove market demand exists. If you don’t have revenue, show user engagement metrics that correlate to revenue potential. If you’re pre-product, show evidence that customers will pay through letters of intent or pilot agreements. A deck full of market size estimates and competitive positioning without traction signals you’re early and risky. A deck showing 40 percent month-over-month revenue growth, 95 percent net revenue retention, and three enterprise customers ready to expand signals you’ve found something real.

Include specific metrics: your monthly recurring revenue or annual recurring revenue, customer acquisition cost, lifetime value, churn rate, and gross margin. Vague statements like strong growth or impressive metrics irritate investors because they suggest you don’t deeply understand your business. Prepare a one-page summary of your financial model that shows unit economics and a path to profitability or sustainable growth. Most founders avoid this because their numbers look weak initially. That’s fine. A realistic financial model showing you understand your path forward beats an inflated model that makes investors question your credibility.

When you meet with investors, bring documents that prove claims: customer contracts, testimonials, usage data dashboards, or pilot results. A screenshot showing your product’s daily active users or revenue curve beats any verbal claim. Prepare specific examples of how you’ll use the capital. Not generic categories like product development and marketing, but concrete plans: hiring a VP of Sales to expand into enterprise, running a $500,000 paid acquisition campaign to test new geographies, or building a specific product feature that removes a customer bottleneck. Investors fund specificity because it shows you’ve thought through execution, not just vision.

Final Thoughts

Selecting the right venture capital example requires matching three concrete criteria: fund stage and check size aligned with your current raise, a track record of actual support for portfolio companies in your sector, and decision-making speed that fits your timeline. Most founders chase brand names and miss funds that move faster and add more value. The venture capital firm that works for your startup is the one that invested recently in companies solving your exact problem, not the one with the biggest name or largest fund size.

Your next step involves building a target list of 15 to 20 funds that deployed capital in your space within the last two years, then calling three founders in each fund’s portfolio to ask whether the investor made introductions that generated revenue and remained engaged during difficult periods. Prepare your pitch materials with specific metrics: monthly recurring revenue, customer acquisition cost, lifetime value, and churn rate. Concrete numbers prove you understand your business far better than vague claims about strong growth.

Once you identify target funds and secure initial meetings, confirm you speak with the actual decision-maker for your stage and sector, and ask potential investors about their reserve strategy and whether they have capital committed to follow-on rounds. We at Primum Law Group provide venture capital transaction services to startups and investors throughout San Francisco and Silicon Valley, helping founders negotiate favorable terms and structure deals that align with long-term goals. Our team handles everything from term sheet review to cap table management, ensuring you understand every commitment before signing.