Starting a venture capital fund requires navigating complex legal structures and regulatory requirements. The National Venture Capital Association forms and guidelines provide the framework that most successful funds follow.

At Primum Law Group, we’ve helped founders understand these requirements and avoid costly mistakes during fund formation. This guide walks you through the essential documents, compliance steps, and structural decisions you’ll face.

What the NVCA Actually Does for Fund Founders

The National Venture Capital Association represents over 600 member firms that manage more than $4 trillion in assets across the United States. Founded in 1973, the organization shaped how modern venture capital operates by establishing standardized legal templates and governance practices that reduced formation costs and accelerated deal closures. The NVCA’s influence extends far beyond its membership-even funds that don’t formally join the association rely on NVCA-drafted documents as their baseline for fund agreements. This widespread adoption happened because the NVCA solved a real problem: before standardized templates existed, each fund spent months negotiating identical provisions with limited partners, wasting time and legal fees on repetitive work.

Why the NVCA Model Documents Matter to Your Fund

The NVCA publishes model legal documents that serve as starting points for fund formation, including limited partnership agreements, subscription agreements, and side letters. These templates don’t lock you into rigid structures-they’re intentionally flexible frameworks that accommodate different investment strategies, fee arrangements, and governance preferences. A 2023 survey by the American Investment Council found that 78% of newly formed funds used NVCA model documents or derivatives of them as their foundation. Using an NVCA-based template typically reduces initial legal drafting costs by 40-50% compared to building documents from scratch, and it signals to institutional investors that your fund follows industry-standard governance practices.

Limited partners recognize these documents because they’ve reviewed them dozens of times, which accelerates their due diligence process.

Industry Standards That Shape Deal Terms

The NVCA maintains guidelines on standard fund economics, investor rights, and management company structures that have become market expectations rather than optional suggestions. For example, the association’s guidance on management fees typically ranges between 1.5% and 2.5% of committed capital for early-stage funds, with performance fees capped at 20% of profits. Institutional investors question deviations from these ranges because departures signal either inexperience or unfavorable economics. The NVCA also publishes annual reports on fund formation trends-their 2024 data showed that the median fund size for early-stage investors reached $185 million, up from $142 million in 2019. These numbers help you calibrate realistic fundraising targets and understand whether your proposed fund structure aligns with what limited partners expect at your stage and strategy level.

How These Standards Affect Your Fund Formation Strategy

Understanding NVCA benchmarks before you structure your fund prevents costly revisions later. Limited partners compare your fund’s terms against NVCA standards during due diligence, and significant deviations require explanation and justification. The association’s model documents also establish precedent for how disputes get resolved, how investor information flows, and what happens if fund performance underperforms. Funds that adopt NVCA frameworks signal institutional competence to potential investors, which matters when you’re competing for capital against established managers.

The specific legal documents and compliance requirements tied to these NVCA standards form the foundation of your fund’s legal structure. Understanding what paperwork you actually need and when you need it determines whether your formation timeline stays on track or gets derailed by missing filings and regulatory oversights.

Legal Documents and Formation Requirements

Starting your fund requires filing specific documents with the SEC and your state, and the paperwork timeline matters more than most founders realize. The SEC requires funds managing over $100 million to register as investment advisers under the Investment Advisers Act of 1940, which triggers Form ADV filing and ongoing compliance obligations. Funds below this threshold can operate under the exemption for private fund advisers, but you still need to file Form D with the SEC within 15 days of your first capital raise to report your offering. Many founders skip this step thinking it’s optional, then face penalties when the SEC discovers the violation during routine audits.

Essential Paperwork for Fund Formation

Your state requires a formation document-typically a limited partnership agreement or LLC operating agreement-filed with the Secretary of State where you’re organizing. The NVCA model limited partnership agreement handles most of this structure, but you cannot simply download it and file without customization. Your agreement needs to specify your fund’s exact fee structure, investor classes if you’re raising from different categories, and dispute resolution mechanisms that comply with your state’s partnership laws.

Delaware and California remain the most common choices for fund domicile because their courts have extensive venture capital case law and predictable interpretations of partnership agreements. Filing your formation documents costs between $500 and $2,000 depending on your state, but the real expense comes from legal review of customized terms-typically $15,000 to $40,000 with a qualified firm.

You’ll also need a subscription agreement that investors sign when they commit capital, which outlines their rights, restrictions on transfers, and information they’ll receive quarterly. The SEC doesn’t mandate specific language here, but institutional investors expect certain protections around liquidity rights and governance participation that the NVCA subscription template covers.

Managing Side Letters and Investor Customization

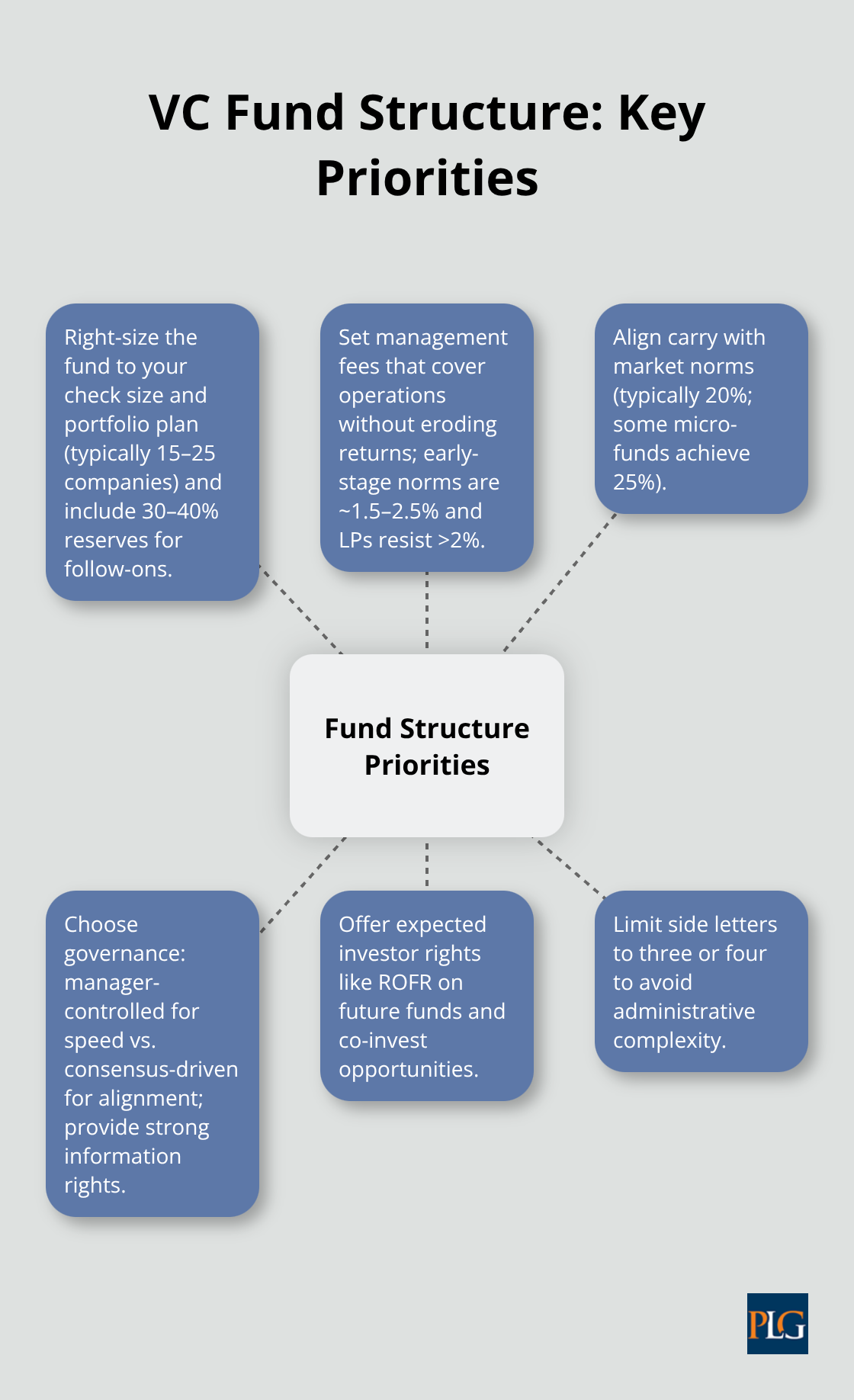

Side letters-individual agreements between your fund and specific investors for customized terms-add another layer of complexity that slows your timeline significantly. Each side letter creates exceptions to your main partnership agreement, and managing 20 side letters with different terms across your investor base becomes a compliance nightmare. Limit side letters to three or four maximum, and only for truly substantial investors who justify the administrative burden.

Compliance and Regulatory Considerations

Your compliance obligations depend partly on your fund size and investor base. If you’re raising exclusively from accredited investors and keeping your investor count under 100, you avoid certain SEC reporting requirements that larger funds face. However, you must still maintain accurate records of who qualifies as accredited-the SEC shifted to a look-through approach in 2020, meaning you need to verify accreditation status for entities and trusts, not just individuals.

This verification process takes 30 to 60 days if you’re raising from institutional investors who provide documentation, but it stretches much longer if you’re raising from high-net-worth individuals unfamiliar with the accreditation process. Your fund also needs a compliance calendar that tracks when various filings and notifications are due-Form ADV amendments when your fund crosses $150 million in assets under management, annual audited financial statements if you exceed $750 million, and quarterly reports to your investors.

Missing these deadlines creates liability for you personally as the fund manager and can trigger SEC enforcement actions.

Timeline and Process Overview

The timeline from fund formation to your first capital close typically spans four to six months if you have your documentation prepared before you start fundraising. This means you should complete your formation documents and SEC filings at least 60 days before you begin investor outreach. Funds that rush this process trying to close capital faster end up revising agreements mid-fundraise when investors raise documentation concerns, which extends your timeline significantly and signals disorganization to prospective limited partners.

Once your legal foundation is solid, your actual fund structure-the size you’re targeting, your fee model, and your governance framework-determines whether limited partners view your fund as a serious contender or a risky bet.

Best Practices for Venture Capital Fund Structure

Your fund size determines everything that follows-your fee revenue, your ability to write meaningful checks, and whether limited partners view you as serious or undercapitalized. The 2024 NVCA data showed median early-stage fund sizes at $185 million, but this number obscures a critical reality: funds under $100 million struggle to justify operational costs while funds over $500 million face pressure to deploy capital quickly into larger rounds. Most founders pick a target size based on how much they think they can raise rather than what makes economic sense for their strategy.

This backwards approach creates problems immediately. If you invest $500,000 to $2 million per company in early-stage rounds, a $50 million fund forces you to write 25 to 100 checks across your portfolio-a portfolio size that becomes unmanageable without a large team. Conversely, a $300 million fund targeting the same check sizes means you cannot deploy capital without either writing smaller checks that don’t move the needle or abandoning your strategy entirely.

Calculate Fund Size From Your Investment Model

Start with your target check size, your intended portfolio size (typically 15 to 25 companies for early-stage), and your reserve allocation for follow-on investments. Most early-stage funds reserve 30 to 40 percent of committed capital for follow-ons, which means a $200 million fund with $2 million initial checks and 20 portfolio companies actually depletes capital faster than the math initially suggests. Work backwards from these numbers to land on a fund size that makes operational sense rather than picking an arbitrary target.

Management Fees That Cover Operations Without Killing Returns

Management fees for early-stage funds typically range between 1.5 and 2.5 percent of committed capital annually, but this range masks important variations based on fund size and strategy. A $100 million fund charging 2 percent generates $2 million annually in management fees, which covers a two-person team barely. A $200 million fund at the same rate generates $4 million, which supports meaningful operational capacity.

The problem intensifies for smaller funds: a $50 million fund at 2 percent produces $1 million in annual fees, which forces you to choose between hiring experienced operators or running lean. Limited partners increasingly push back on management fees exceeding 2 percent for early-stage funds, viewing higher rates as compensation for inexperience rather than value delivery.

Performance fees (carried interest) typically cap at 20 percent of profits for early-stage funds, though some micro-funds negotiate 25 percent because their smaller fund sizes require higher carry to make the economics work for the general partners. Your fee structure must sustain your team while remaining competitive with market expectations. If you cannot operate your fund effectively at market-rate fees, your fund size is too small.

Attempting to charge above-market fees signals either inexperience or unfavorable economics, both of which limit your fundraising success. Calculate your annual operational costs first-salaries, office space, compliance, insurance, and back-office support-then work backwards to determine what fund size supports these costs at market-rate fees. This prevents the common mistake of raising a fund size that cannot support the team you actually need.

Investor Rights and Governance That Prevent Conflicts Later

Your governance framework determines how you make decisions when limited partners disagree with your investment choices or fund direction. Most NVCA model agreements give general partners broad discretion over investment decisions while limiting limited partner involvement to information rights and voting on extraordinary matters like fund dissolution or GP removal. This structure works until your fund underperforms, at which point limited partners scrutinize every decision and second-guess your judgment.

The governance question to resolve early is whether you build a manager-controlled fund or a consensus-driven fund. Manager-controlled funds move faster and avoid endless negotiation with limited partners, but they create resentment if performance disappoints. Consensus-driven funds move slowly but build investor alignment that matters during downturns.

Most successful early-stage funds lean toward manager control with strong information rights for limited partners-quarterly reports showing portfolio company performance, capital deployment, and fund economics.

Investor rights around information access cost you almost nothing to provide but create significant goodwill. Limited partners also expect rights of first refusal if you raise a follow-on fund and co-investment rights if you deploy meaningful capital into secondary opportunities outside your main fund. Negotiate these terms during fundraising rather than discovering conflicts later when limited partners feel excluded.

Governance Terms That Shape Long-Term Relationships

Your partnership agreement should specify what happens if a general partner leaves or the fund underperforms materially-terms that NVCA documents address but that require customization based on your specific situation. The governance framework you establish now becomes the template for your entire relationship with limited partners and shapes their willingness to commit to follow-on funds.

Final Thoughts

Forming a venture capital fund requires you to integrate three interconnected decisions: understanding how National Venture Capital Association forms and standards shape investor expectations, completing your legal documentation and SEC filings on schedule, and structuring your fund around realistic economics rather than aspirational targets. Most founders treat these as separate problems when they actually form one integrated challenge. Your fund size determines your fee revenue, which determines your team capacity, which determines your ability to execute your investment strategy effectively.

The most common mistakes we see at Primum Law Group involve founders who rush their legal documentation to start fundraising faster, then face investor pushback on governance terms they didn’t anticipate. Others select fund sizes that sound impressive but cannot support the operational infrastructure required to manage a portfolio effectively. Still others ignore NVCA benchmarks thinking they can negotiate custom terms with limited partners, only to discover that institutional investors simply walk away rather than negotiate against market standards.

You should build your formation timeline backwards from your target fundraising launch date-you need 60 to 90 days minimum to complete legal documentation, SEC filings, and compliance setup before you approach your first investor. This means starting your formation process now if you plan to fundraise within the next quarter. Contact us at https://primumlaw.com to discuss your fund formation timeline and avoid the delays that derail most first-time fund managers.