Corporate accounting crimes cost U.S. businesses an estimated $5.3 billion annually, according to the Association of Certified Fraud Examiners. Laws like the Sarbanes-Oxley Act were enacted to prevent corporate accounting-related crimes, yet violations continue to occur.

At Primum Law Group, we help San Francisco businesses understand these legal requirements and build defenses against fraud. This guide covers the laws that matter, the risks your company faces, and the practical steps to protect yourself.

What Accounting Crimes Actually Look Like

Three Forms of Misconduct

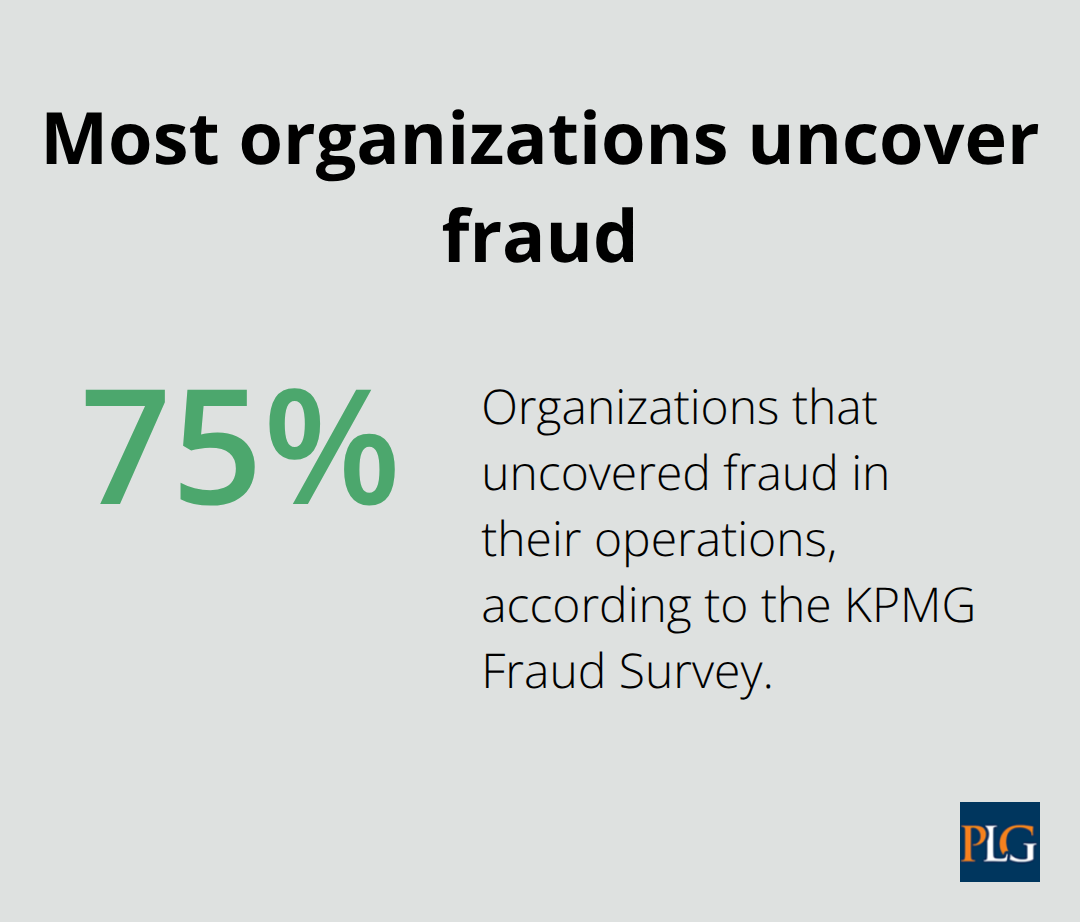

Accounting crimes in San Francisco and across the country take three primary forms, and understanding each one helps you spot warning signs before damage occurs. Financial statement manipulation happens when executives or finance teams intentionally misrepresent revenues, expenses, or assets to make a company appear more profitable or stable than it actually is. The KPMG Fraud Survey found that about 75% of organizations uncovered fraud in their operations, meaning most companies encounter some form of misconduct.

Embezzlement and misappropriation of funds occur when employees or managers steal company assets, often through fictitious vendor schemes, unauthorized cash withdrawals, or falsified expense reports.

How the SF Parks Alliance Case Reveals Control Failures

The SF Parks Alliance case illustrates how dangerous weak controls become. The organization reported roughly $1.2 million in cash but failed to prevent alleged misuse of restricted donor funds, with partner organizations like Friends of Franklin Square left with about $148,000 in unreimbursed expenses. Vendor reimbursements slowed to a crawl, with some partner groups receiving payments of only $100 at a time, yet leadership’s financial misconduct allegations only surfaced after the organization’s sudden closure. This pattern shows how embezzlement often goes undetected for months or years because it happens gradually and involves lower-level transactions that seem routine.

Detection Difficulty and Financial Impact

The critical difference between these crimes lies in detection difficulty and financial impact. Statement manipulation typically requires collusion among multiple people and affects how investors, lenders, and regulators view your company, potentially triggering SEC enforcement actions or criminal prosecution under federal law. San Francisco businesses operating in regulated industries face additional exposure because auditors and regulators expect higher standards.

Why Most Accounting Crimes Succeed

The reality is that most accounting crimes succeed not because perpetrators are sophisticated, but because organizations lack proper segregation of duties, independent reconciliations, and transparent vendor payment processes. A single person controlling cash receipts, bank deposits, and account reconciliation creates the perfect environment for fraud. Implementing controls that separate these functions-so one person receives checks, another deposits them, and a third person reconciles the bank statement-eliminates most embezzlement opportunities. Regular bank reconciliations completed by someone independent of transaction processing catch discrepancies quickly, while monitoring of vendor creation and payment approvals prevents fictitious vendor schemes before they drain significant funds.

These control failures expose companies to massive financial and legal risk, which is why federal law imposes strict requirements on how businesses must operate and report their finances.

Federal Laws That Stop Accounting Crimes

San Francisco businesses operate under a web of federal laws designed specifically to prevent the fraud patterns we just discussed. The Sarbanes-Oxley Act, passed in 2002 after the Enron and WorldCom scandals, requires public companies to maintain robust internal controls and have auditors attest to their effectiveness. Section 404 of SOX demands that management assess internal control effectiveness annually, and auditors must verify these assessments-this is not optional paperwork but a legal obligation with teeth.

Sarbanes-Oxley Compliance and SEC Enforcement

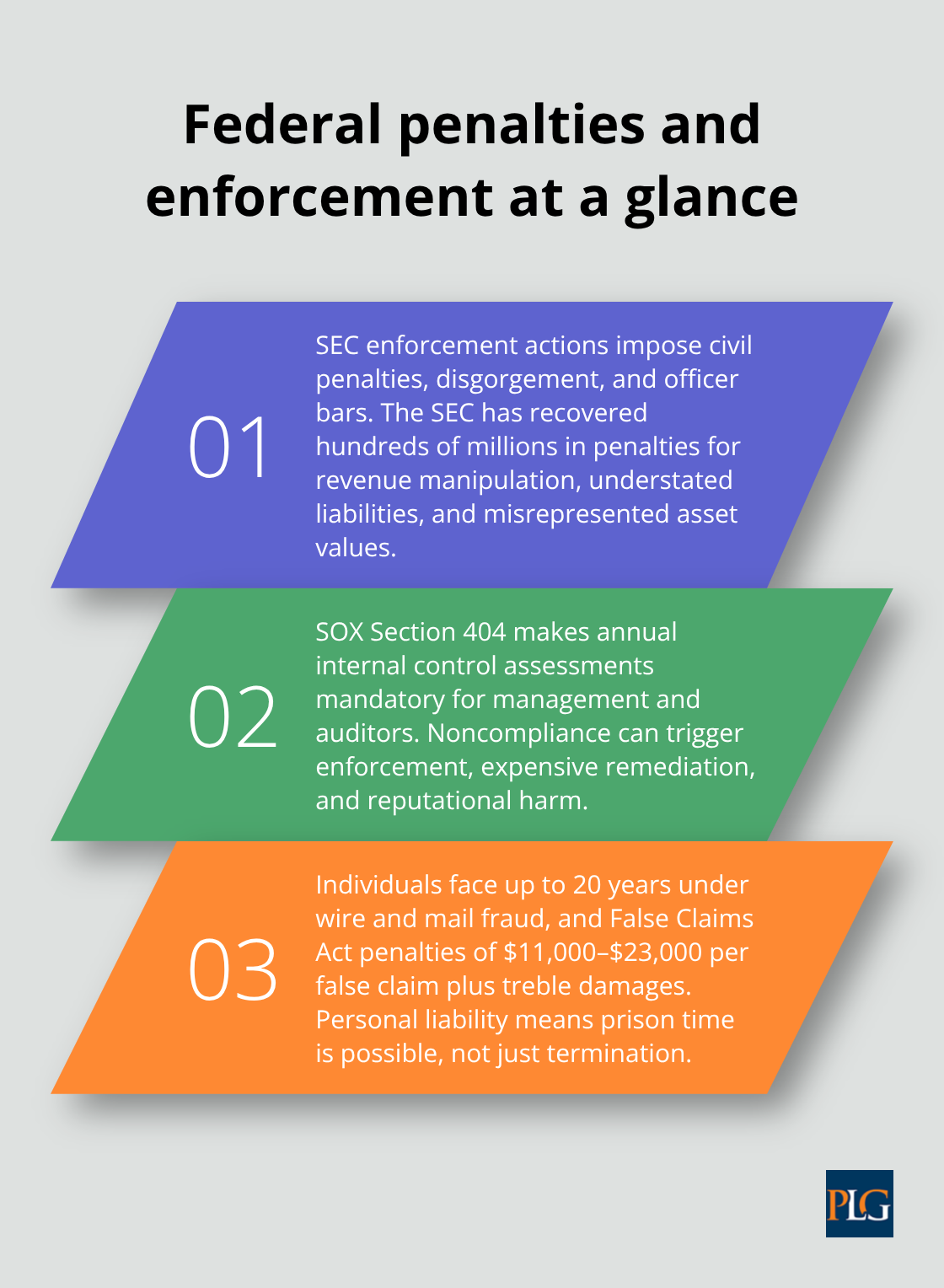

Companies that fail SOX compliance face SEC enforcement actions, which result in civil penalties, disgorgement of ill-gotten gains, and officer bars that prevent executives from serving in leadership roles. The Securities Exchange Commission actively pursues financial statement fraud cases; in recent years, the SEC has recovered hundreds of millions in penalties from companies that manipulated revenue recognition, understated liabilities, or misrepresented asset values. For San Francisco tech companies and growth-stage businesses, understanding that SOX principles apply to your internal controls even before you go public matters-building these controls now prevents the expensive remediation later.

Criminal Liability for Individuals

Federal criminal law adds another enforcement layer that makes accounting crimes genuinely risky for perpetrators. The wire fraud statute, mail fraud statute, and conspiracy charges carry sentences up to 20 years in prison, while the False Claims Act allows the government to pursue civil penalties of $11,000 to $23,000 per false claim plus treble damages.

Individual employees and executives face personal criminal liability, not just the company-embezzlement or statement manipulation can result in prison time, not merely termination.

Building a Culture That Deters Fraud

This reality means that building a compliance culture where employees understand the personal consequences of misconduct proves far more effective than assuming people will follow rules out of goodwill. Companies that implement transparent vendor approval processes, require dual signatures on checks, and conduct unannounced cash counts demonstrate to employees and prosecutors alike that fraud will be detected. The SF Parks Alliance case showed what happens when organizations fail to implement these federal-standard controls-once investigators uncovered the alleged misconduct, the organization collapsed and leadership faced potential criminal referrals.

These federal laws create real consequences, but they only protect your company if you translate them into actual operational practices. The next section covers the specific internal controls and audit procedures that transform legal requirements into working defenses against fraud.

Building Controls That Actually Stop Fraud

The gap between having compliance policies and actually preventing fraud comes down to one thing: whether your San Francisco business makes stealing harder than working. Most companies understand they need internal controls, but they treat them as compliance checkbox items rather than operational necessities. This mindset fails because controls only work when daily processes embed them and monitoring happens consistently.

Segregation of Duties: Your First Line of Defense

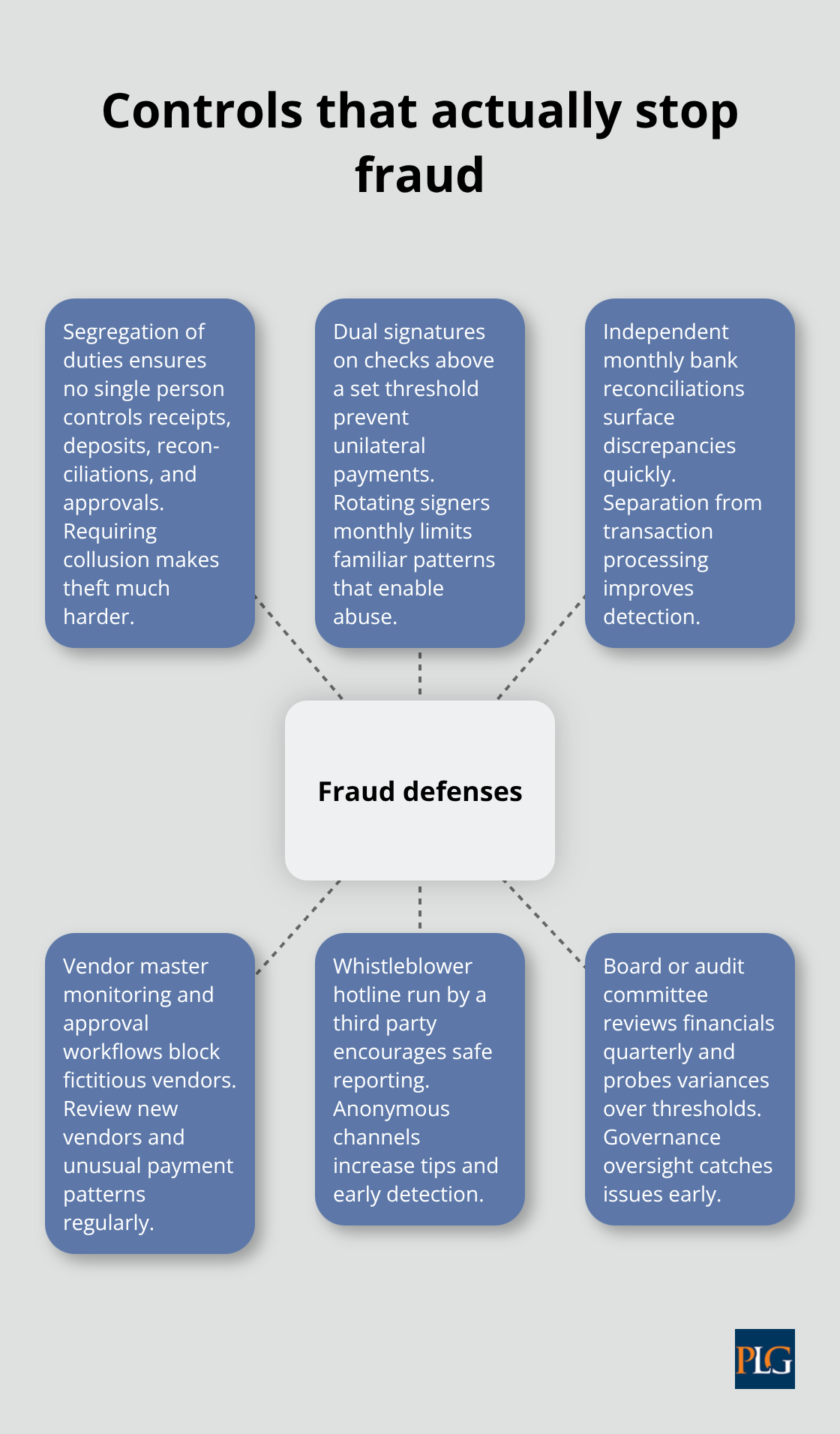

Segregation of duties stands as the single most effective control, and it works because it requires collusion to commit fraud. When one person receives checks, another deposits them, a third reconciles the bank statement, and a fourth approves vendor payments, no individual can steal without involving multiple people. The SF Parks Alliance lacked this separation, which allowed alleged misconduct to continue undetected for months. Your San Francisco business should implement this control immediately: no single employee should handle receipts, deposits, reconciliations, and approvals.

Preventive Controls That Eliminate Embezzlement

Require dual signatures on checks above a certain threshold-say $5,000-and rotate check-signing authority monthly so the same person never signs consecutively. Monthly bank reconciliations completed by someone independent of transaction processing catch discrepancies within 30 days rather than waiting for year-end audits. Unannounced cash counts performed quarterly by someone outside the finance department deter embezzlement because employees cannot predict when verification will occur. These controls cost almost nothing to implement but eliminate the vast majority of embezzlement schemes.

Detective Controls That Catch What Prevention Misses

Detective controls catch what preventive controls miss, and they matter because no prevention system is perfect. Require itemized receipts for all expenses over $100 and review them monthly against budget forecasts to spot unusual patterns. Examine vendor master files quarterly to identify fictitious vendors-watch for vendors with no phone number, vendors that only appear once, or vendors paid entirely in cash. Review journal entries created outside normal processes, as this is where executives manipulate financial statements. Conduct surprise audits of petty cash and credit card charges monthly rather than annually.

Whistleblower Programs and Risk Assessment

Implement a formal whistleblower hotline staffed by an independent third party, not your HR department, because employees will not report misconduct to people they see daily. The AICPA Fraud Risk Management Guide recommends that organizations document their fraud risk assessment and update it annually, identifying which fraud scenarios pose the highest risk to your business.

For San Francisco startups and growth companies, this means assessing whether your biggest risk is fictitious vendors, payroll fraud, revenue manipulation, or asset theft, then designing controls specifically for those scenarios. Detective controls should also include quarterly financial statement reviews by your board or audit committee, comparing actual results to budget and requiring management to explain variances above 10%. This catches both intentional manipulation and operational problems before they become disasters.

Final Thoughts

Accounting crimes threaten San Francisco businesses of all sizes, but they remain preventable through consistent operational discipline. The Sarbanes-Oxley Act was enacted to prevent corporate accounting-related crimes after major corporate failures exposed how weak controls enable fraud, yet SOX compliance alone does not stop embezzlement or statement manipulation. Your company must translate legal requirements into daily practices that make stealing genuinely difficult, and the controls we discussed-segregation of duties, dual check signatures, monthly bank reconciliations, and quarterly vendor audits-cost minimal money while eliminating most fraud opportunities.

Detective controls like whistleblower hotlines and surprise cash counts catch what prevention misses, and federal criminal penalties of up to 20 years in prison create real consequences for perpetrators. Your board should review financial statements monthly, your finance team should understand that controls protect them personally, and your employees should know that misconduct will be detected. The SF Parks Alliance case demonstrated what happens when organizations fail to implement these basics-alleged misconduct went undetected for months, partner organizations lost hundreds of thousands of dollars, and leadership faced potential criminal referral.

Start now by conducting a fraud risk assessment specific to your business, identifying which scenarios pose the highest risk, then implementing controls that target those risks. Assign responsibility for monthly reconciliations and quarterly audits to people independent of transaction processing, and document your control procedures in writing so new employees understand expectations and auditors can verify compliance. We at Primum Law Group help San Francisco businesses build compliance frameworks that prevent fraud while supporting growth-contact us to discuss how we can strengthen your internal controls and protect your company from accounting crimes.